27 June 2014 AMC - Market held flat, however Nasdaq advances

Market Summary

European

Markets Closing Prices

European

markets are now closed; stock markets across Europe performed as follows:

·

UK's FTSE: + 0.3%

·

Germany's DAX: + 0.1%

·

France's CAC: -0.1%

·

Spain's IBEX: -0.3%

·

Portugal's PSI: -1.7%

·

Italy's MIB Index: -0.3%

·

Irish Ovrl Index: + 0.1%

·

Greece ATHEX Composite: -1.3%

Before Market Opens

S&P futures vs fair value:

-5.10. Nasdaq futures vs fair value: -6.50.

The S&P 500 futures trade five points below fair value.

Asian markets ended the session on a lower note.

The S&P 500 futures trade five points below fair value.

Asian markets ended the session on a lower note.

·

In economic data: o

Japan's National CPI rose 3.7% year-over-year (prior 3.4%), while National Core

CPI increased 3.4% year-over-year (consensus 3.4%, previous 3.2%). Separately,

Tokyo CPI rose 3.0% year-over-year (prior 3.1%), while Tokyo Core CPI increased

2.8%, as expected (previous 2.8%). Also of note, Household Spending plunged

8.0% year-over-year (expected -2.0%, previous -4.6%), Retail Sales slipped 0.4%

year-over-year (expected -1.8%, prior -4.4%), and the Unemployment Rate ticked

down to 3.5% from 3.6% (expected 3.6%)

------

·

Japan's Nikkei lost 1.4%, pressing to a one-week low. A

stronger yen weighed on exporters as Canon fell 1.6% and Nissan Motor lost

0.9%.

·

Hong

Kong's Hang Seng added 0.1%,

remaining near its best levels of 2014. Insurers lagged as Ping An Insurance

and China Life Insurer fell 0.8% and 0.5%, respectively.

·

China's Shanghai Composite shed 0.1% as trade was unable

to reclaim the 50-day moving average. Shanxi Coal sank 3.2% following reports

the company filed a suit against customers for not paying their bills.

Major European indices hover near

their flat lines amid light volumes. Of note were comments from Bank of England

Governor Mark Carney, who discussed policy once again, saying interest rate

hikes are possible in 2014 or 2015 and that the ‘new normal' rate would be near

2.50%.

·

Participants received

several data points:

o Eurozone Business and Consumer Survey slipped to

102.0 from 102.6 (expected 103.0) as Consumer Confidence fell to -8.0 from -7.1

(expected -7.0) and Business Climate inched down to 0.2 from 0.4 (expected

0.4)

o Germany's Import Price Index was unchanged

month-over-month (expected 0.2%, previous -0.3%), while CPI rose 0.3%

month-over-month (expected 0.2%, previous -0.1%)

o Great Britain's Q1 GDP was left unrevised at

0.8% quarter-over-quarter, while the year-over-year reading was revised down to

3.0% from 3.1%. Separately, the current account deficit narrowed to GBP18.50

billion from GBP23.50 billion (expected deficit of GBP17.50 billion) and

Business Investment rose 5.0% quarter-over-quarter (consensus 2.7%, prior

2.7%)

o French Q1 GDP was left unrevised at 0.0%, while

Consumer Spending rose 1.0% month-over-month (expected 0.4%, prior -0.2%).

Separately, PPI slipped 0.5% month-over-month (consensus -0.6%, previous

-0.2%)

o Spain's Retail Sales rose 0.5% year-over-year

(expected 1.8%, previous 0.7%)

o Italy's Business Confidence improved to 100.0

from 99.8 (expected 99.8)

o Swiss KOF Leading Indicators rose to 100.4 from

100.1 (expected 99.1)

------

·

In

France, the CAC is higher by

0.1%. Industrials outperform with Airbus Group and Legrand both up near 1.7%.

Countercyclical names are among the laggards. Orange is lower by 1.1% and

Veolia Environnement holds a loss of 1.8%.

·

Germany's DAX trades up 0.2%. Utilities display strength

with E.ON and RWE up 0.6% and 1.0%, respectively. Conglomerate Siemens lags,

trading lower by 1.1%.

·

Great

Britain's FTSE holds an advance of

0.2%. Homebuilders Barratt Developments and Persimmon lead with gains of 3.8%

and 1.8%, respectively.

·

Spain's IBEX is lower by 0.2% amid weakness in

financials. Banco Santander, Bankinter, and CaixaBank are down between 0.5% and

0.8%.

U.S. Equities

·

Futures point to a heavy

open after yesterday's late-day rally erased most of the early losses

·

The DJIA and S&P

linger near all-time highs while the Nasdaq holds near its best levels in more

than 14 years

·

The VIX (11.63) remains

near its lowest levels since February 2007

o S&P Futures -5 @ 1944

o Dow Futures -30 @ 16,732

o Nasdaq Futures -5 @ 3812

Asia

·

Markets ended mostly

lower across Asia

·

Japan saw a big drop in

household spending (-8.0% YoY actual v. -1.9% YoY expected) and an uptick in

inflation at the national level (3.4% YoY) while holding steady in Tokyo (2.8%

YoY). The small than expected decline in retail sales (-0.4% YoY actual v.

-1.9% YoY expected) was the lone bit of good news

·

Japan's Nikkei (-1.4%)

pressed to a one-week low

·

Hong Kong's Hang Seng

(+0.1%) remained near its best levels of 2014

·

China's Shanghai

Composite (-0.1%) as trade was unable to reclaim the 50 dma

·

India's Sensex (+0.2%)

saw a lackluster session

·

Australia's ASX (-0.4%)

was rejected by the 50 dma

Market Internals

Leaders and Laggards

Technical Updates

Commentaries

Commodities

Closing Commodities: Natural Gas

Falls 2.9% Over the Week

·

Aug gold traded slightly

above the breakeven level today, rising to a session high of $1321.90 per

ounce. It eventually settled 0.2% higher at $1320.00 per ounce, gaining 0.3%

over the week.

·

Sep silver traded near

the unchanged line in a range between 21.07 per ounce and $21.22 per ounce.

Unable to gain buying support, it settled 0.1% lower at $21.14 per ounce,

booking a 0.7% gain for the week.

·

Aug crude oil pulled

back from its session high of $106.17 per barrel shortly after equity markets

opened and spent the remainder of floor trade chopping around in negative

territory. It touched a session low of $105.33 per barrel and eventually

settled at $105.76 per barrel, or four cents lower, booking a 1.0% loss for the

week.

·

Aug natural gas spent

the tire pit session in the red, trading as low as $4.38 per MMBtu. It inched

slightly higher heading into the close and settled with a 0.5% loss at $4.42

per MMBtu. Today's weakness brought losses for the week to 2.9%.

CBOT

Agriculture and Ethanol/ICE Sugar Closing Prices

·

Sep

corn rose 3 cent to

$4.42/bushel

·

Sep

wheat rose 8 cents to

$5.93/bushel

·

Aug

soybeans fell 5 cents to

$13.77/bushel

·

Sep

ethanol rose cent to

$2.00/gallon

·

Sep

sugar (#16 (U.S.)) rose

0.05 of a penny to 26.13 cents/lbs

NYMEX

Energy Closing Prices

Aug crude oil fell $0.04 to $105.76/barrel

·

Crude oil pulled back

from a session high of $106.17 shortly after equity markets opened and spent

the remainder of floor trade chopping around in negative territory. It touched

a session low of $105.33 and eventually settled just four cents below the

unchanged line, booking a 1.0% loss for the week.

Aug natural gas fell 2 cents to $4.42/MMBtu

·

Natural gas spent the

entire pit session in the red, trading as low as $4.38. It inched slightly

higher heading into the close and cut losses to 0.5%. Today's weakness brought

losses for the week to 2.9%.

Aug heating oil fell 2 cents to $3.02/gallon

Aug

RBOB rose 1 cent to $3.07/gallonTreasuries

On other news....

Currencies

Dollar Fights to Hold 80.00: 10-yr:

-01/32..2.532%..USD/JPY: 101.36..EUR/USD: 1.3645

·

The Dollar Index presses

session lows as trade looks to avoid its first sub-80.00 close since May 12. Click here to see a daily Dollar

Index chart.

·

EURUSD is +30 pips @ 1.3640 as steady buying over the

course of the session has trade contending with its best close in three

weeks. Resistance in the 1.3650 area moves into focus as the 200 dma

also lurks in the vicinity. Eurozone data is heavy as M3 money supply, private

loans, and CPI Flash Estimate accompany German retail sales.

·

GBPUSD is -5 pips @ 1.7020 as trade holds just off the

lows. Sterling saw some light buying early on in the session, but has been in a

steady decline since the wider than anticipated trade deficit. The 1.7050 area

has provided resistance over the past two weeks, and the inability to push

through that level has caused some to turn their attention towards the 1.6900

level. British data is limited to net lending to individuals.

·

USDCHF is -25 pips @ .8910 as trade breaks down

to a one and a half-month low. Today's selling has the pair probing its 50

dma, and comes amid strength in the euro.

·

USDJPY is -30 pips @ 101.35 as action lingers

near one-month lows following the large drop in household

spending an in uptick in the national inflation reading. The 101.25 area

will be watched closely in the days ahead as support at the level dates back to

the beginning of February. Japan's preliminary industrial production is due out

Sunday evening.

·

AUDUSD is +5 pips @ .9415 amid a rather subdued trade.

Early buying threatened the .9450 level sellers were once again able to stand

their ground. Any close above .9420 would be the best since November.

·

USDCAD is -30 pips @ 1.0665 as trade looks

likely to book its lowest close since January 7. Today's selling comes

despite a larger than expected decline in Canada's Raw Materials Price Index

(-0.4% actual v. 1.3% expected), and has trade testing key support in the area.

Canada's GDP will be released on Monday.

Weekly Analysis

Week 1

Technical Updates

{kind=link}

Briefing's Commentaries

Next Week In View

Economic Commentaries

Economic summary: Michigan Sentiment

above expectations

Economic Data Summary:

Economic Data Summary:

·

June

Michigan Sentiment - Final 82.5 vs Briefing.com consensus of 81.7; May was 81.2

o The preliminary June report initially showed a

decline in confidence. That didn't jive with the big improvements in equity

prices and employment conditions. The final reading brings the Consumer

Sentiment Index in-line with the Conference Board's Consumer Confidence Index,

which increased to 85.2 in June from 82.2 in May. Unless there is a disruption

in stock trends or employment conditions, consumer sentiment will likely

continue on its upward trend in July. The Current Conditions Index was revised

up to 96.6 in June from a preliminary reading of 95.4. The Consumer

Expectations Index increased to 73.5 from 72.2. The expectations level remains

below the May reading of 73.7.

Upcoming Economic Data:

·

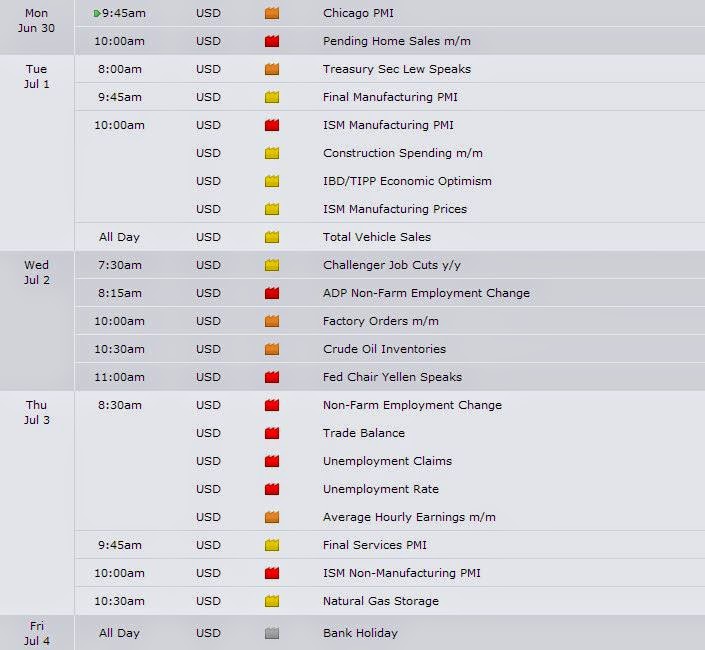

June Chicago PMI due out

Monday at 9:45 (May was 65.5)

·

May Pending Home Sales

due out Monday at 10:00 (April was 0.4%)

Upcoming Fed/Treasury Events:

·

San Francisco Fed

President John Williams (not a voting FOMC member, moderate) to speak tomorrow

at 13:10

Other International Events of

Interest

·

Japan saw a big drop in

household spending (-8.0% YoY actual v. -1.9% YoY expected) and an uptick in

inflation at the national level (3.4% YoY) while holding steady in Tokyo (2.8%

YoY). The small than expected decline in retail sales (-0.4% YoY actual v.

-1.9% YoY expected) was the lone bit of good news.

Jason's Commentaries

It came in pretty much a surprise the market actually held up on Friday. Due to the movements of Apple, IBM, Oracle and Apple, the entire market got dragged up. However, looking across the entire market, the market was actually more flat than ever. Volumes spiked to a new high, the bulls bearly outpaced the bears and there's a lot of divergence all around the place. The market started with a bearish sentiment all the way until after lunch as the market started reversing and covered all the losses made throughout the day. Looking at the technical side, the market is likely to consolidate for a short while, possibly making a retracement. This week, we're having a few major events happening. Yellen is speaking on Wednesday and we're having the employment report earlier this week as Friday is a public holidays. Seems that the market might be pricing once again.

Market Call: FLAT to upside

Date: 30 Jun 2014