22 Feb 2013 AMC

Market Summary

Market Internals

Leaders and Laggards

Technical Updates

Commentaries

|

Commodities

Treasuries

Weekly Analysis

Week 38

Technical Updates

Briefing's Commentaries

Week in Review: S&P 500 Snaps Seven Week Winning Streak

On Monday, equity and bond markets were closed in observance of Presidents Day.

Tuesday's session saw the S&P 500 settle higher by 0.7% after spending the duration of the day in a steady upward climb. Equities got off to an upbeat start supported in part by bullish European trade. In addition, merger speculation helped support the markets at the open. Health care stocks were in the news when the Centers for Medicare & Medicaid Services proposed lower 2014 Medicare co-payments. The news carried a negative impact for health care providers as Humana (HUM 70.61, -2.04) and UnitedHealth Group (UNH 54.47, -0.77) lost 6.4% and 1.2% respectively.

On Wednesday, the S&P 500 settled lower by 1.2% after spending the entire session in negative territory. Equities began the day on a lower note amid mixed housing data and hovered near their lows ahead of the Fed's minutes. Stocks then fell to fresh lows after the minutes indicated Committee members saw little change to the economic outlook. Homebuilders sold off in reaction to an earnings and revenue miss reported by Toll Brothers (TOL 34.59, +0.12). Peers PulteGroup (PHM 18.90, +0.15) and D.R. Horton(DHI 22.31, +0.14) were off 6.8% and 5.9% respectively.

Thursday proved to be an extension of Wednesday's weakness as the S&P 500 settled lower by 0.6%. Stocks began the day in the red and continued sliding into the afternoon when bargain hunters stepped in and lifted the major averages off their lows. The S&P 500 managed to hold the psychologically important 1500 level, avoiding its first close below that mark since February 4. Wal-Mart (WMT 70.40, +0.14) gained 1.5% after beating on earnings. However, the company issued first quarter guidance on the low end of analyst expectations. In addition, Wal-Mart said it expects its comparable store sales to be flat during the first quarter. This suggests the worries regarding consumer spending, expressed in an internal email last week, have some credence to them. ..NYSE Adv/Dec 2246/733. ..NASDAQ Adv/Dec 1770/688.

Next Week In View

Jason's Commentaries

Was right on the call for Friday, DJI went up almost a 120 points, and all 3 main indices posted some decent gains. The VIX lost a total of 6.9% on Friday when HP came in fantastic results and spiked a 12% gain. On the Dow, We have KO, GD, AXP,DD and IBM performing exceptionally well on Friday, each with a gain of more than 1.5% which allow DJI to lock in such huge gain. Although there was not much economic news coming out on Friday, earnings drove the day up. Looking at the internals, volumes was not very impressive, having a mere 680 Million shares traded on the NYSE, which is slightly lower than the average traded volume. Although, the bulls were outpacing the bears, it seems that the bears was able to stand their ground a little.The treasuries looked a little divergence on Friday. While the market is rallying on Friday, Treasuries did the same thing with the 5,10 and 30 year.

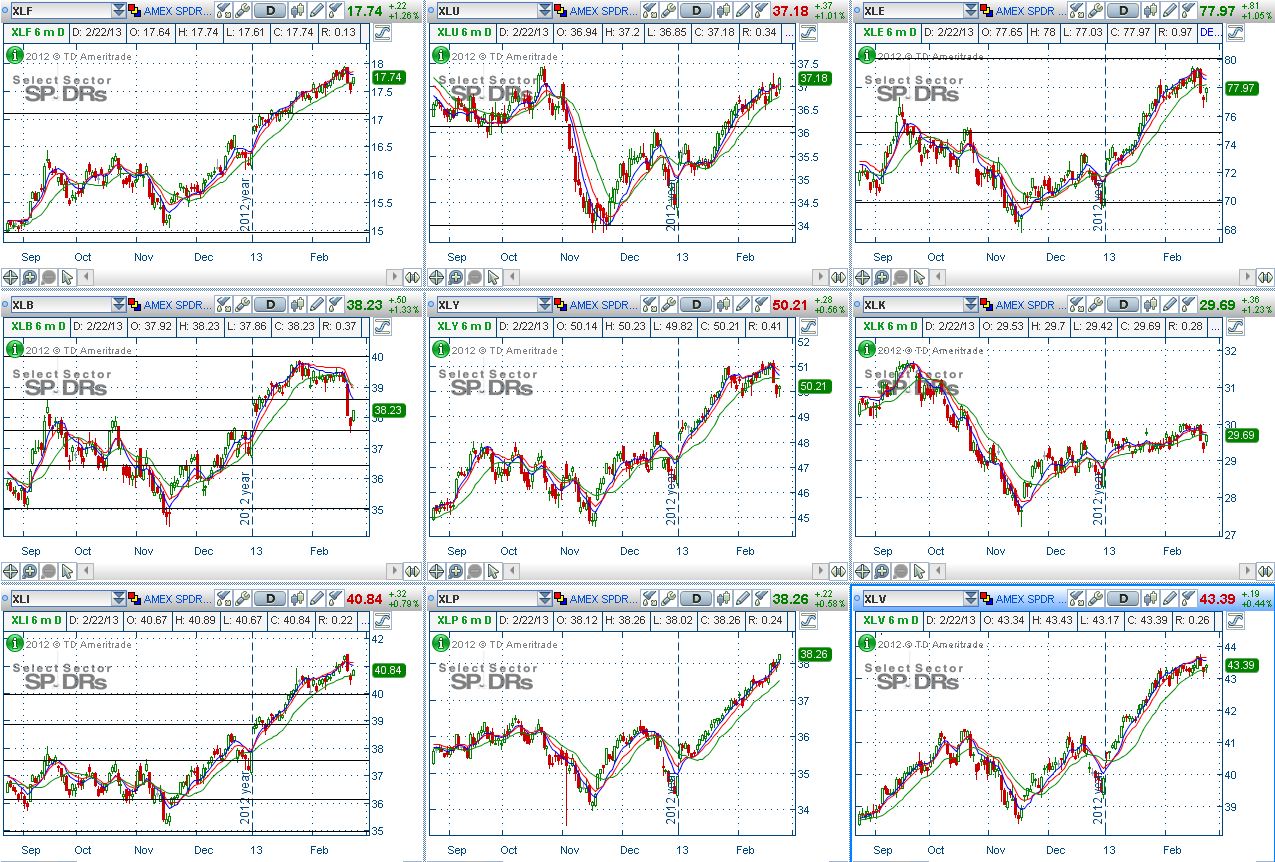

While on our 9 main sectors, the leaders were the financials, Tech, Utilities and Materials. Financials were being led by Morgan Stanley, AIG, Prudential, Goldman Sachs, Charles Schwab, Legg Mason and BlackRock. Each having a gain of more than 2% on the Friday. While on the Materials, It was companies like Du Pont, Dow Chemicals and Eastman Chemical which led the sector. Not to mention Mosaic, Aloca, CF Industries were down in materials. While on the Tech, HP, Texas instrument, Symantec led the sector up tremendously, having a gain of more than 2.5% each. And if we were to look at the weekly performance of the 9 sectors, the Industrials, Materials, Consumer Discretionary, Tech and Healthcare seems to be losing a little of their steam and might be correcting soon. The industrials were being bogged down by the Defense Industry, Healthcare being dragged by the HMOs, the Materials were lagged by the Agriculture Industry. And tech namely were weighed down by the giant Apple.

As we're entering the end of Feb, which is likely to mark the end of this flat and volatile month, we're also expecting the Congress to decide and act on the Fiscal Cliff and debt ceiling issues which has been postponed since Jan. This coming week also mark the first week of Mar, which the first trading day of Mar has been down 4 times out of 6, up 9 of 11 times. While we're looking at the chart, we're definitely still in a consolidation phase.My dear friend, Jason Tan, http://strongerhead.com, has noted something very interesting on the consolidation period of the market at its highs, which is worth spending a few minutes of your time reading it.

While we're coming to an end of the earnings season, here's the report card on the S&P 500 stocks.

Out of the 500 stocks,

86.5%, announced their earnings.

63.3% beat their earnings

11.4% just met their earnings

25.2% missed their estimate.

Having a 25% missing their Q4 results is not exactly a good thing for the market.

Market Call: DOWN

Date: 25 Feb 2013

No comments:

Post a Comment