12 Apr 2013 AMC

Market Summary

Market Internals

Leaders and Laggards

Technical Updates

Commentaries

|

Commodities

Treasuries

Weekly Analysis

Week 38

Technical Updates

Briefing's Commentaries

Stocks spent the bulk of Monday's session in negative territory before afternoon buying lifted the major averages out of the red. As a result, the S&P 500 settled higher by 0.6%. Although stocks finished with gains, leadership was mixed, suggesting a certain level of indecision was present among market participants. Both consumer sectors ended ahead of the broader market with the defensively-oriented staples in the lead. Coca-Cola (KO 41.08, -0.10) rose 2.0% and Philip Morris (PM 96.44, +0.84) advanced 1.9%.

On Tuesday, equities settled just off their best levels of the session with the S&P 500 gaining 0.4%. After opening on a higher note, stocks alternated between gains and losses until afternoon action sent the major indices to their highs. Steelmakers rallied across the board as the Market Vectors Steel ETF (SLX 42.25, -0.44) surged 3.4% to record its second largest one-day advance of the year.

Wednesday saw the S&P 500 rise 1.2% as technology, health care, and industrials outperformed the broader market. Notably, the Dow Jones Transportation Average stood out with a gain of 1.8%. On the downside, homebuilders sat out the broad market rally asTaylor Morrison Home Corporation (TMHC 24.30, +0.29) made its debut as a publically traded company.

On Thursday, the S&P 500 rose 0.4%, but technology stocks did not participate in the advance. The sector was under pressure after the International Data Corporation indicated first-quarter PC shipments plunged 14%. This marked the largest decline on record since IDC began tracking shipments in 1994, and pressured major tech names. Hewlett-Packard (HPQ 20.90, +0.02) fell 6.5% while Intel (INTC 21.68, -0.15) and Microsoft(MSFT 28.79, -0.14) settled with respective losses of 2.0% and 4.4%. ..NYSE Adv/Dec 1171/1787. ..NASDAQ Adv/Dec 1009/1474.

Next Week In View

Jason's Commentaries

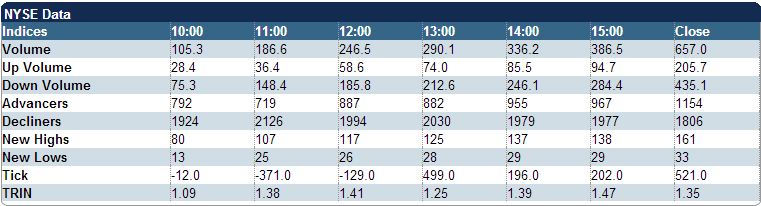

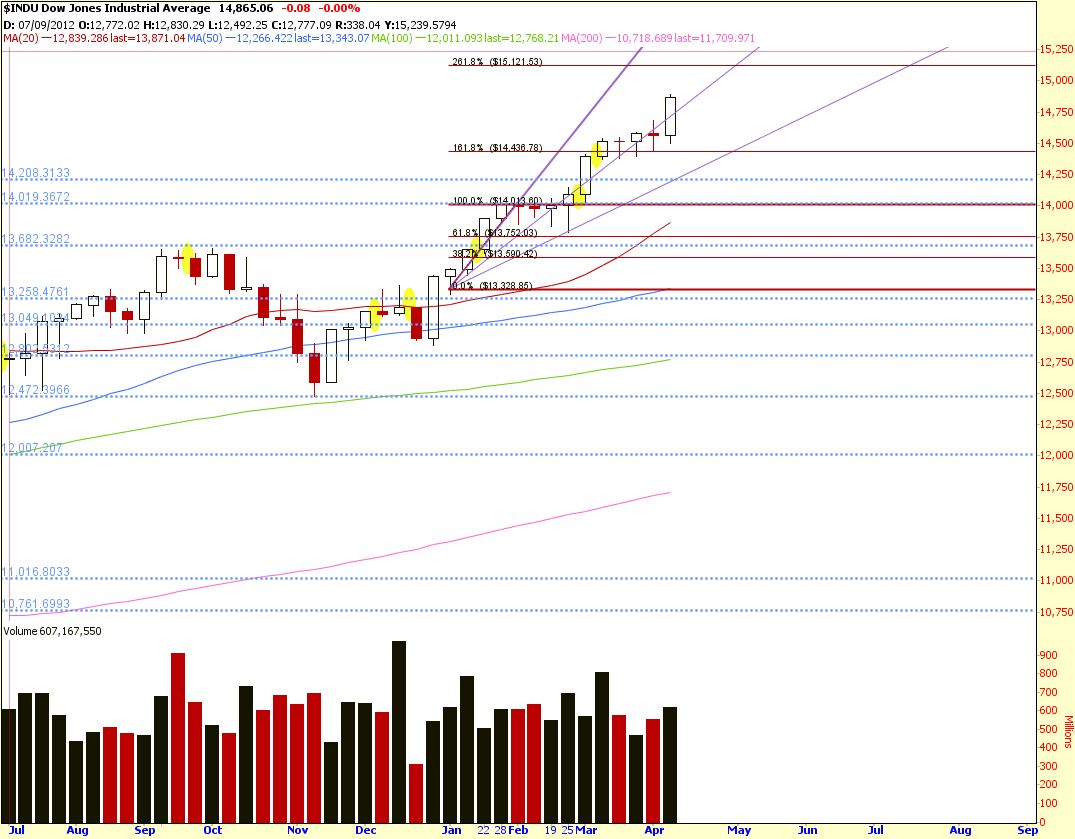

The market came under pressure at the start of the day with Wells Fargo and JP Morgan's earnings not quite up the expectation. As I expected.. It was really a volatile session and we ended flat for the trading day. Wells Fargo and JP Morgan managed to beat the bottom line expectation but the revenues fall. Due to much cost cutting in the financial sectors, I won't consider the results fantastic. While Monday we have Citi announcing their earnings before market open. I believe 3 of the major banks earnings will be able give a good snapshot on how the financial sector is going to perform already. While on the internals, we're able to have quite a bit of volumes at 657Mil shares traded on the NYSE and the DVOL managed to outpaced the UVOL by 2:1. While we're having the flat day, the main leader for the day was Consumer Discretionary while the Materials and Energy lagging each more than 1.3%. So it's more of a down day than a flat day. While on the technical side, the Dow is showing a hanging man which signifies the end of trend already, however, a little divergence from the weekly charts, where all 3 indices are showing bullish candlestick formation. That is definitely a sign that the market is going to go through a volatile period, especially through this earnings season. From the 9 main sectors movements, we can see that the defensive sectors are outweighing the important sectors like Financials and Tech. If anymore other Dow components are not performing well for their earnings, I'm expecting the Sell-in-May to come early. While on the commodities, Oil sunk below $90 per barrel at the start of trading session on Monday as other Asian markets are being hammered. On top of that, precious metals had a rough session on Friday as well. Seems that Precious metals are not exactly a 'safe haven' anymore right? Nonetheless, we're not going to have much data coming out on Monday, so the centre of gravity will lies on Citi's earnings.

Market Call:FLAT

Date: 15 Apr 2013

No comments:

Post a Comment