28 Jun 2013 AMC

Market Summary

Market Internals

Leaders and Laggards

Technical Updates

Commentaries

|

Commodities

Treasuries

Weekly Analysis

Week 38

Technical Updates

Briefing's Commentaries

Week in Review: S&P 500 Tests 100-Day Moving Average

On Monday, the stock market began the week on a fitful note as rising interest rates at home and falling equity markets abroad conspired to keep the major averages in negative territory throughout the day. The S&P 500 registered its first close below its 100-day moving average this year. Overseas, the drop in China was attributed to a growing sense of angst that a liquidity crisis and credit crunch are brewing there. The growth concerns weighed heavily on the cyclical sectors throughout the day. Financials (-1.8%) led the losses and were joined by materials (-1.7%), industrials (-1.7%), energy (-1.5%), and technology (-1.4%) as the worst-performing areas.

Equities ended Tuesday's session near their highs, but were unable to erase their Monday losses. The S&P 500 climbed 1.0% as all ten sectors ended with gains. The bulk of the advance occurred in the first 90 minutes of the session amid a global rebound. Interestingly, two rate-sensitive sectors vaulted to the top of this month's leaderboard despite the continued climb in Treasury yields. The telecom services sector rose 2.0%, which turned its month-to-date loss to a gain of 1.0%.

Wednesday began on an upbeat note despite some disappointing economic news. The final first quarter GDP reading was revised down to 1.8% from 2.4%. Typically, revisions to GDP in the third estimate are very minor. The large decline in this report was very unusual and caught all economists by surprise. Most of the downward revision came from consumption in services. In the previous estimate, services spending increased 3.1%. That was revised down to 1.7% growth and contributed 0.6 percentage points less to GDP growth. Stocks received this news in stride as sluggish growth suggests the Federal Reserve is less likely to withdraw its support from the markets. To that end, the Treasury complex received an aggressive bid immediately after the GDP revision crossed the wires. The benchmark 10-yr yield ended lower by seven basis points at 2.542%.

On Thursday, the S&P 500 settled higher by 0.6% as nine sectors posted gains. Equities were off to the races at the sound of the opening bell, aided by the personal income report, which pointed to an increase of 0.5% in May. The Briefing.com consensus expected personal income to rise 0.2%. Stocks received a secondary boost from the pending home sales report as May sales rose 6.7% (1.5% consensus). The S&P notched its high of 1620 shortly after the market digested the latest housing data point. However, the index was unable to rise above that level as the 20- and 50-day moving averages served as resistance at the session high. ..NYSE Adv/Dec 1541/1488. ..NASDAQ Adv/Dec 1322/1180.

Next Week In View

Jason's Commentaries

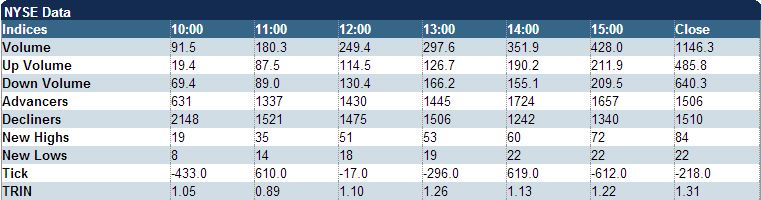

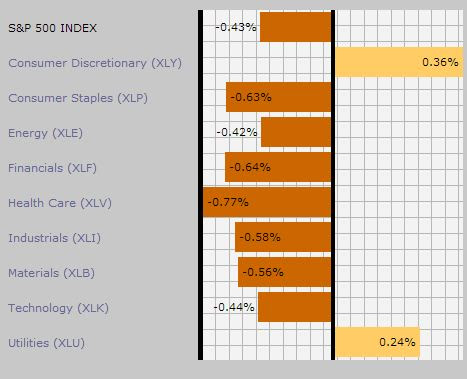

Was right for the call for Friday, Dow was being dragged down by IBM while Nasdaq lead by Apple.. While S&P500 is showing some mixed signs. Market started with a bearish bias and went through a volatile session through the day. Volumes was standing at 1100m shares on the NYSE. While the internals are showing mixed signs. VIX went lower as well. Most sectors were performing in the red except for Consumer discretionary and Utilities. Both S&P500 and Dow showed a reversal pattern facing the resistance at the 20MA. While on the weekly perspective, we have all 3 indices sitting on the support. It's gonna be a very volatile week as we're having the employment reports coming this weeks. So... prepare for the ride.

Market Call: Flat to upside

Date: 1 July 2013

No comments:

Post a Comment