28 Aug 2013 AMC

Market Summary

Before Market Opens

Markets

across Asia were mostly lower as worries of a conflict in Syria caused crude

oil to spike above $112 per barrel in overnight trade, pressuring equities.

Majors like Japan's Nikkei (-1.5%) and Hong Kong's Hang Seng (-1.6%) saw heavy

selling, but it was the Philippines PSEi (-3.0%) that was saddled with the

biggest decline as action posted its lowest close of 2013. All was not bad in

peripheral Asia as Indonesia's Jakarta Composite (+1.5%) rebounded after days of

heavy selling. Elsewhere, India's Sensex (+0.2%) eked out a gain despite the

rupee tumbling roughly 4.0% to a low of 68.93 per dollar. Data out of the

region was light as Thailand's industrial production sank 4.5% year-over-year

(-1.8% expected) and South Korea's business confidence ticked up to 73 from 72.

·

In

Japan, the Nikkei closed

lower by 1.5% as trade closed at a two-month low. Heavyweights Fast Retailing

and Softbank were pressured, giving up 1.3% and 1.9%, respectively. On the

upside, shares of oil explorer Inpex outperformed, posting a 0.9%

advance.

·

Hong

Kong's Hang Seng lost 1.6% as

trade ended at a five-week low. Energy stocks were under pressure with

PetroChina tumbling 4.4% after executives from one of its subsidiaries were

said to be under investigation.

·

In

China, the Shanghai Composite

shed 0.1% amid a choppy trade. Financials lagged as Ping An Bank fell 2.3%.

Elsewhere, gold miners Shandong Gold-Mining and Zhongjin Gold Corp. moved limit

up, 10%.

The

major European indices have spent the first half of the session in negative

territory with Germany's DAX (-1.4%) leading to the downside. Investors

received a fair share of economic data. Eurozone M3 Money Supply rose 2.2%

year-over-year (2.1% expected, 2.4% prior) while private loans decreased 1.9%

year-over-year (-1.6% forecast, -1.6% previous). Germany's GfK Consumer Climate

slipped to 6.9 from 7.0 (7.1 expected). Separately, the Import Price Index

ticked up 0.3% month-over-month (0.2% expected, -0.8% prior). Great Britain's

CBI Distributive Trades Survey rose to 27 from 17 (19 forecast). Italy's retail

sales slipped 0.2% month-over-month (0.1% expected, 0.1% prior) while the

year-over-year reading indicated a decrease of 3.0% (1.2% previous). Also of

note, speaking at a campaign rally in Rendsburg, German Chancellor Angela

Merkel said "Greece shouldn't have been allowed into the euro" and

that "Chancellor [Gerhard] Schroeder accepted Greece and weakened the

Stability Pact."

·

In

France, the CAC holds a loss

of 0.3%. Hotel operator Accor trades lower by 4.3% after the company introduced

a new chairman and chief executive officer. Exporter Renault is also among the

laggards, trading lower by 3.5%.

·

Great

Britain's FTSE is lower by 0.5% as

airlines lead the decliners. EasyJet and International Consolidated Airlines

Group sport respective losses of 3.5% and 5.2%. Oil companies are among the

leaders with BG Group, Royal Dutch Shell, and Tullow Oil up between 1.8% and 3.1%.

·

In

Germany, the DAX trades down

1.4% as Lufthansa leads to the downside with a loss of 4.2%. Exporters BMW,

Daimler, and Volkswagen also lag with losses between 1.4% and 1.9%.

Market Internals

Market Internals -Technical-

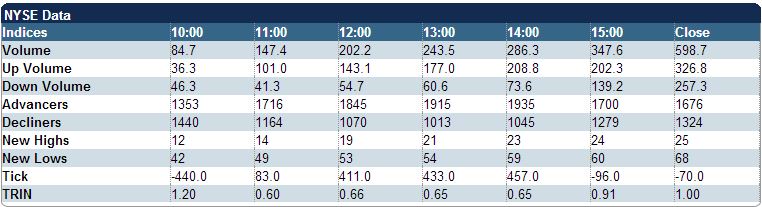

The Nasdaq closed up 15 (+0.41%) at 3593, the Dow closed up 48 (+0.33%) at 14825, and the S&P 500 closed up 4 (+0.27%) at 1635. Action came on below average volume (NYSE 598 mln vs. avg. of 735; NASDAQ 1333 mln vs. avg. of 1584), with advancers outpacing decliners (NYSE 1698/1362, NASDAQ 1453/1051) and new lows outpacing new highs (NYSE 26/70, NASDAQ 33/26).

Relative Strength:

Indonesia-IDX +2.29%, Lithium-LIT +2.23%, Cocoa-NIB +2.07%, Energy-XLE +1.66%, Energy-IYE +1.65%, Oil Services-OIH +1.53%, Columbia Index-GXG +1.49%, South Korea-EWY +1.47%, Italy-EWI +1.3%, Brazilian Real-BZF +1.11%.

Relative Weakness:

Gold Miners-GDX -2.75%, Silver Miners-SIL -1.9%, Mexico-EWW -1.73%, Poland-EPOL -1.42%, Switzerland-EWL -1.39%, Germany-EWG -1.25%, Corn-CORN -1.12%, South Africa-EZA -0.98%, Base Metals-DBB -0.87%, 20+ Year Treasuries-TLT -0.81%

Leaders and Laggards

Technical Updates

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Briefing's Commentaries

Closing Market Summary: S&P 500 Unable to Clear 100-Day Moving Average

The S&P 500 settled higher by 0.3% to follow yesterday's 1.6% slide. Although the benchmark index advanced, it was unable to retake its 100-day moving average.

Eight of ten sectors finished in positive territory with energy leading the way. The sector displayed significant strength, climbing 1.8%, after outperforming during yesterday's session. Thanks to today's jump, energy is the only sector trading in positive territory this month.

On a related note, crude oil rose 0.4% to $109.40 per barrel, and has gained almost 12.0% so far this quarter amid increased tensions in the Middle East. Oil prices bear watching over the coming days as the continued strength has the potential to pose as a headwind to economic growth.

The Dow Jones Transportation Average is one of the groups with increased sensitivity to energy prices. The bellwether complex underperformed with a loss of 0.1% after falling 2.6% during yesterday's session. The weakness in transports weighed on the industrial sector, which added less than 0.1%.

Overall, today's rebound was not very robust. Yesterday, six sectors lost more than 1.0%, and today, none of those six advanced more than 0.4%. Outside of energy, only health care and discretionary shares finished ahead of the S&P.

The health care space advanced 0.4% as biotechnology rallied. The iShares Nasdaq Biotechnology ETF (IBB 193.32, +2.05) rose 1.1%, which helped the Nasdaq outperform the broader market.

Elsewhere, the discretionary space gained 0.4% as retailers displayed strength. Express (EXPR 21.10, +1.30) jumped 6.6% following its in-line report while the SPDR S&P Retail ETF (XRT 77.79, +0.43) finished higher by 0.6%. While most discretionary components advanced, home builders lagged as the iShares Dow Jones US Home Construction ETF (ITB 20.56, -0.10) slipped 0.5%.

Countercyclical sectors ended in mixed fashion as utilities (+0.3%) settled in-line while consumer staples (-0.7%) and telecom services (-0.5%) lagged.

Treasuries finished on their lows with the benchmark 10-yr yield tacking on six basis points to 2.78%.

Today's session saw below-average trading volume as less than 600 million shares changed hands on the floor of the New York Stock Exchange.

The weekly MBA Mortgage Index remained in a downtrend with today's 2.5% fall marking the fourteenth decline out of the past sixteen readings including last week's 4.6% slide.

Separately, July pending home sales fell 1.3%, which was worse than the 0.2% increase forecast by the Briefing.com consensus. Today's reading follows last month's decrease of 0.4%.

Tomorrow, weekly initial claims and the second estimate of second quarter GDP will be reported at 8:30 ET.

The U.S. Treasury will auction $29 billion in 7-yr notes.

Commodities

Closing Commodities: Crude Oil Rises

1%, Closes Just Above $110/Barrel

·

Oct crude oil rose for a

fifth consecutive session on continued concerns over unrest in the Middle East.

The energy component chopped around near the $110.00 per barrel level after

pulling back from a high of $112.24 per barrel set in overnight action, its

highest level since May 2011. It eventually settled at $110.07 per barrel, or

1.0% higher

·

Sep natural gas erased

earlier losses after trading as low as $3.51 per MMBtu in morning pit trade. It

broke into positive territory in last half hour of the floor session and closed

0.3% higher at $3.58 per MMBtu

·

Precious metals

retreated into negative territory as the dollar index gained strength

·

Dec gold pulled back

from its session high of $1431.00 per ounce and eventually settled with a 0.1%

loss at $1418.70 per ounce

·

Sep silver brushed a

session low of $24.22 per ounce after trading as high as $25.00 per ounce

earlier in the session. It closed 1.1% lower at $24.38 per ounce

NYMEX Energy Closing Prices

·

Oct

crude oil rose $1.07 to

$110.07/barrel

o Crude oil rose for a fifth consecutive session

on continued concerns over tension in Syria. The energy component chopped

around near the $110.00 level for most of today's pit trade after trading as

high as $112.24 in overnight action, its highest level since May 2011. It

eventually settled with a 1.0% gain.

·

Sep

natural gas rose 1 cent to

$3.58/MMBtu

o Natural gas lifted from its session low of $3.51

and trended higher as the session progressed. It broke into positive territory

in the last half hour of pit trade and settled 0.3% higher.

·

Oct

heating oil rose 4 cents to

$3.21/gallon

·

Oct

RBOB gasoline rose 4 cents to

$2.96/gallon

CBOT Agriculture and Ethanol/ICE

Sugar Closing Prices

·

Dec

corn fell 6 cents to

$4.80/bushel

·

Sep

wheat fell 4 cents to

$6.47/bushel

·

Nov

soybeans rose 1 cent to

$13.74/bushel

·

Sep

ethanol rose 2 cents to

$2.49/gallon

·

Nov

sugar (#16 (U.S.)) rose

0.33 of a penny to 20.95 cents/lbs

COMEX Metals Closing Prices

·

Dec

gold fell $1.50 to

$1418.70/ounce

o Gold touched a session high of $1431.00 moments

after floor trade opened but slipped into negative territory as the dollar

index gained strength. It spent the remainder of its session chopping around

just below the break-even line and eventually settled with a 0.1% loss.

·

Sep

silver fell $0.28 to

$24.38/ounce

o Silver also retreated into the red after trading

as high as $25.00 in early morning pit action. It brushed a session low of

$24.22 and settled with a 1.1% loss.

·

Sep

copper fell 3 cents to

$3.30/lbs

{kind=link}

Treasuries

Treasuries slip to session lows

2-yr unch @ 99 30/32

3-yr -04/32 @ 99 17/32

5-yr -11/32 @ 98 29/32

7-yr -16/32 @ 98 19/32

10-yr -22/32 @ 97 14/32

30-yr -1 06/32 @ 97 15/32

{kind=link}

Next Day In View

Economic Commentary

On other news....

Summary of Weekly Petroleum Data for the Week Ending Aug 23, 2013

Production: U.S. crude oil refinery inputs averaged about 15.8 mln barrels per day (bpd) during the week ending August 23, 2013, 71 thousand bpd below the previous week's average. Refineries operated at 91.3% of their operable capacity last week. Gasoline production decreased last week, averaging 9.4 mln bpd. Distillate fuel production decreased last week, averaging about 4.9 mln bpd.

Imports: U.S. crude oil imports averaged about 8.4 mln bpd last week, up by 423 thousand bpd from the previous week. Over the last four weeks, crude oil imports averaged over 8.0 mln bpd, 723 thousand bpd below the same four-week period last year. Total motor gasoline imports (including both finished gasoline and gasoline blending components) last week averaged 670 thousand bpd. Distillate fuel imports averaged 165 thousand bpd last week.

Inventory: U.S. commercial crude oil inventories (excluding those in the Strategic Petroleum Reserve) increased by 3.0 mln barrels from the previous week. At 362.0 mln barrels, U.S. crude oil inventories are near the upper limit of the average range for this time of year. Total motor gasoline inventories decreased by 0.6 mln barrels last week and are in the upper half of the average range. Finished gasoline inventories increased while blending components inventories decreased last week. Distillate fuel inventories decreased by 0.3 mln barrels last week and are near the lower limit of the average range for this time of year.

Demand: Total products supplied over the last four-week period averaged 19.4 mln bpd, up by 0.9% from the same period last year. Over the last four weeks, motor gasoline product supplied averaged about 9.2 mln bpd, up by 1.0% from the same period last year. Distillate fuel product supplied averaged over 3.7 mln bpd over the last four weeks, up by 3.1% from the same period last year.

Currencies

Euro Fails at 1.3400: 10-yr:

-19/32..2.785%..USD/JPY: 97.73..EUR/USD: 1.3331

The Dollar Index drifts near session highs amid a rather uneventful trade. The Index saw a steady climb to 81.50 over the course of the morning, but action has spent most of U.S. trade confined to a tight 10 cent range. Bulls remain steadfast in their efforts to retake the 200-day moving average (81.70).

The Dollar Index drifts near session highs amid a rather uneventful trade. The Index saw a steady climb to 81.50 over the course of the morning, but action has spent most of U.S. trade confined to a tight 10 cent range. Bulls remain steadfast in their efforts to retake the 200-day moving average (81.70).

·

EURUSD is -60 pips at 1.3330 after an early effort to

retake the 1.3400 level was once again thwarted. The single currency is now

testing minor support in the area, with a breakdown setting up a move towards

1.3250. However, the more important level is 1.3200, which will be helped by

the 50-day moving average. Trade saw little reaction to headlines out

this afternoon indicating Italy has canceled property tax plans on first homes,

removing some near-term headline risk as Silvio Berlusconi's LDP threatened to

leave the coalition if measures were passed. German preliminary CPI

and unemployment change will cross the wires tomorrow. Click here to see a daily EURUSD

chart.

·

GBPUSD is -25 pips at 1.5520 after seeing a sharp

reversal following comments from Bank of England Governor Carney. Mr.

Carney suggested the central bank could embark on more easing if the recovery

falters, causing a face-ripping rally off session lows (1.5430) as the

comments provided nothing new. Current action is probing support aided by the

200-day moving average.

·

USDCHF is +45 pips at .9220 as action withstood yet

another test of key .9200 support. The ability to hold key support despite

several tests over the past couple of weeks has bulls look ahead to the .9350

level that is aided by both the 50- and 200-day moving averages.

·

USDJPY is +70 pips at 97.75 as trade holds just off the

best levels of the session. The pair briefly probed the 97.00 level, but it was

able to hold and action now climbs back towards the upper end of the range.

However, the 99.00 area will prove difficult to conquer as both the 50- and

100-day moving averages aid trendline resistance. Japanese data is limited to

retail sales.

·

AUDUSD is -35 pips at .8940 as trade ticks lower for a

second session. Early weakness dropped the pair below the important

.8900 area, but the hard currency looks as though it will avoid a fresh

three-year low. Australian data includes HIA New Home Sales and private

capital expenditure.

·

USDCAD is +5 pips at 1.0480 as action holds just off

the day's lows. A breakdown of current levels will likely lead to a test of

1.0425 support that is helped by the 50-day moving average. Canada's current

account is scheduled for release tomorrow morning.

Jason's Commentaries

Market is getting into the 'one day up one day down' syndrome already... it's gonna be a sideways consolidation phase for a while before breaking out. Market started with a bullish bias in the market as there are many traders covering their position after the market had a blood bath on Tuesday. And it seemed that the market actually continued the trend all the way till closing bell. But towards the end of the session, the market had some minor profit taking. Volumes were rather thin, with approx 600m shares traded on the NYSE. Internals were showing mixed signals in session last night. Consumer staples lagged while the Energy sector gained the most in the market last night. Energy sector is likely to hold up the indices as Syria's issue worsen. While on the technical standpoint, we can see that the indices are likely to hit the support level. However, I believe it's likely to hold up for another day. And we're having the prelim GDP results coming out tonight which is likely to gyrate the market if GDP contracts. As for the commodities, Crude oil hit a high of $112.24 last night, on Syria fears. Petrol price is going up soon...

Market Call: Flat to upside

Date: 29 Aug 2013

It's the mismanagement of the economy by the selfish blundering of our ruling class.

ReplyDeletecomposiet

keramiek

terrazzo

graniet