26 March 2014 AMC- Market dragged down by Financials, Industrials and Tech; Citi down 5% after Fed rejects capital plan

Market Summary

European

Markets Closing Prices

European

markets are now closed; stock markets across Europe performed as follows:

·

UK's FTSE: 0.0%

·

Germany's DAX: + 1.2%

·

France's CAC: + 0.9%

·

Spain's IBEX: + 1.5%

·

Portugal's PSI: + 0.9%

·

Italy's MIB Index: + 1.4%

·

Irish Ovrl Index: + 1.1%

·

Greece ATHEX Composite: + 0.2%

Before Market Opens

S&P futures vs fair value:

+8.10. Nasdaq futures vs fair value: +21.50.

The S&P 500 futures trade eight points above fair value.

It was a sea of green across Asia as all of the major bourses, aside from China's Shanghai Composite (-0.2%), saw gains. The latest Reserve Bank of Australia Financial Stability Review warned that low rates cannot last forever, and coincided with a speech from RBA Governor Stevens that warned of the dangers of a continued increase in home prices.

Elsewhere, Japan Prime Minister Shinzo Abe's economic advisor reiterated that the government is ready to announce additional policy easing measures in mid-May if the consumption tax hike, scheduled for April, begins to weigh on the economy.

In regional data, South Korea's final GDP improved to 3.7% year-over-year (expected 3.9%, prior 3.4%) and Singapore's industrial production jumped 12.8% year-over-year (consensus 12.9%).

The S&P 500 futures trade eight points above fair value.

It was a sea of green across Asia as all of the major bourses, aside from China's Shanghai Composite (-0.2%), saw gains. The latest Reserve Bank of Australia Financial Stability Review warned that low rates cannot last forever, and coincided with a speech from RBA Governor Stevens that warned of the dangers of a continued increase in home prices.

Elsewhere, Japan Prime Minister Shinzo Abe's economic advisor reiterated that the government is ready to announce additional policy easing measures in mid-May if the consumption tax hike, scheduled for April, begins to weigh on the economy.

In regional data, South Korea's final GDP improved to 3.7% year-over-year (expected 3.9%, prior 3.4%) and Singapore's industrial production jumped 12.8% year-over-year (consensus 12.9%).

·

Japan's Nikkei ticked up 0.4% amid a quiet trade.

Exporters outperformed as Toyota added 1.1% and Sony tacked on 1.9%.

·

Hong

Kong's Hang Seng rose 0.7%, but

surrendered the bulk of its early gains. Financials led as Bank of

Communications and Bank of China climbed 3.3% and 2.5%, respectively.

·

China's Shanghai Composite slipped 0.2%, holding near

three-week highs. Property developers were among the laggards with China Vanke

and Gree Real Estate both losing close to 1.5%.

Major European indices hold gains

across the board with Spain's IBEX (+1.7%) setting the pace. Among news of

note, Bank of England Monetary Policy Committee Member Martin Weale said that

the British economy is getting better with visible improvement in wages. Mr.

Weale also said that interest rates will not remain at current record-low

levels forever.

Economic data was limited. Germany's GfK Consumer Climate held steady at 8.5, as expected. Italian Retail Sales were unchanged month-over-month (consensus 0.4%, prior -0.3%) while the year-over-year reading fell 0.9% (expected -1.6%, previous -2.6%). Separately, Consumer Confidence improved to 101.7 from 97.7 (consensus 98.4). Elsewhere, Swiss Consumption Indicator increased to 1.57 from 1.49.

Economic data was limited. Germany's GfK Consumer Climate held steady at 8.5, as expected. Italian Retail Sales were unchanged month-over-month (consensus 0.4%, prior -0.3%) while the year-over-year reading fell 0.9% (expected -1.6%, previous -2.6%). Separately, Consumer Confidence improved to 101.7 from 97.7 (consensus 98.4). Elsewhere, Swiss Consumption Indicator increased to 1.57 from 1.49.

·

Great

Britain's FTSE is higher by 0.5%

with financials trading in mixed fashion. Standard Life and Hargreaves Lansdown

hold respective gains of 5.3% and 3.6% while Lloyds Banking Group holds a loss

of 4.4% after the British government sold a 7.9% stake in the bank.

·

In

France, the CAC trades up

1.1%. Industrials outperform with Alstom, Lafarge, and Schneider Electric up

between 1.8% and 2.0%. On the downside, GDF Suez is the lone decliner, trading

lower by 0.7%.

·

Germany's DAX holds an advance of 1.5% with all 30 components

trading higher. Producers of basic materials lead with BASF, K+S, and

ThyssenKrupp showing gains between 1.7% and 3.0%.

·

Spain's IBEX leads the region with a gain of 1.7%.

Bankia and CaixaBank trade higher by 3.2% and 4.1%, respectively.

U.S. Equities

·

Equity futures suggest

solid gains at the open

·

Yesterday's bid ran the

S&P 500 to within 0.6% of its record-high close

·

Durable orders (2.2%

actual v. 1.0% expected)

·

Durable orders -ex transportation

(0.2% actual v. 0.3% expected)

o S&P Futures +7 @ 1866

o Dow Futures +70 @ 16,368

o Nasdaq Futures +18 @ 3642

Asia

·

It was a sea of green

across Asia as all of the major bourses, aside from China's Shanghai Composite

(-0.2%), saw gains

·

The latest Reserve Bank

of Australia Financial Stability Review warned that low rates cannot last

forever, and coincided with a speech from RBA Governor Stevens that warned of

the dangers of a continued increase in home prices

·

South Korea's Final GDP

improved to 3.7% YoY (3.4% YoY previous, 3.9% YoY expected)

·

Singapore's industrial

production jumped 12.8% YoY (12.9% YoY expected)

·

Thailand's trade deficit

swung to a $1.77 bln surplus (-$2.5 bln previous)

·

Japan's Nikkei (+0.4%)

ticked higher amid a quiet trade

·

Hong Kong's Hang Seng

(+0.7%) surrendered the bulk of its early gains

·

China's Shanghai

Composite (-0.2%) held near three-week highs

·

India's Sensex (+0.2%)

closed at all-time highs

·

Australia's ASX (+0.8%)

climbed to its best level in almost two weeks

Market Internals

Market Internals -Technical-

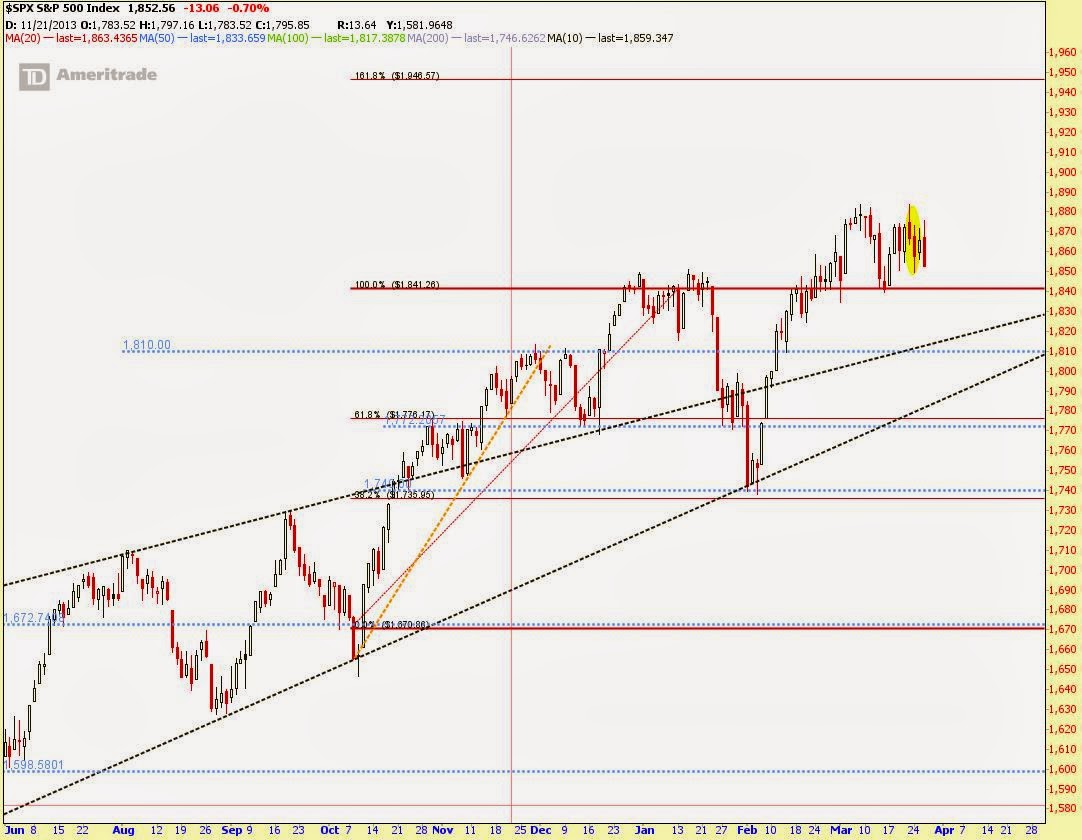

The Nasdaq closed down 31 (-1.43%) at 4174, the S&P 500 closed down 13 (-0.7%) at 1853, and the Dow closed down 99 (-0.6%) at 16269. Action came on slightly above average volume (NYSE 738 mln vs. avg. of 731; NASDAQ 2292 mln vs. avg. of 2042), with decliners outpacing advancers (NYSE 1057/2081, NASDAQ 558/2118) and new highs outpacing new lows (NYSE 92/29, NASDAQ 55/35).

Relative Strength:

Turkey-TUR +4.18%, Sugar-SGG +3.17%, Volatility-VXX +1.83%, Livestock-COW +1.57%, Eastern Europe-ESR +1.54%, South Korea-EWY +1.33%, Chile-ECH +0.93%, Oil-USO +0.89%, 20+ Year Treasuries-TLT +0.78%, Columbia Index-GXG +0.78%.

Relative Weakness:

Junior Gold Miners-GDXJ -5.64%, Clean Energy-PBW -4.92%, Gold Miners-GDX -4.04%, Cotton-BAL -3.62%, Silver Miners-SIL -3.24%, Vietnam-VNM -2.85%, Greece-GREK -2.6%, Sweden-EWD -1.45%, Israel-EIS -1.28%, Middle East and Africa-GAF -1.06%.

Leaders and Laggards

Technical Updates

{kind=link}

{kind=link}

Briefing's Commentaries

Closing Market Summary: Momentum

Names Lead Stocks Lower

The major averages finished the Wednesday session on a cautious note with the S&P 500 falling 0.7%. The Dow Jones Industrial Average (-0.6%) outperformed while small caps bore the brunt of the pressure. The Russell 2000 declined 1.9% while the Nasdaq Composite fell 1.4%.

Equity indices began the day on an upbeat note, but the financial sector (-0.9%) served up an early warning by not taking part in the opening rally. One industry group that briefly participated in the early advance was the biotech space. The iShares Nasdaq Biotechnology ETF (IBB 235.09, -4.35) was up as much as 1.1% during the first hour of action, but faded from the early high, taking the market lower. Interestingly, the broader health care sector (+0.1%) finished the day ahead of the remaining nine groups.

Outside of the relative weakness in biotechnology, the lack of upward momentum in the likes of Amazon.com (AMZN 343.41, -11.30), Facebook (FB 60.38, -4.51), Priceline.com (PCLN 1188.77, -34.93), and Tesla (TSLA 212.96, -7.48) kept the tech-heavy Nasdaq behind the other indices. Facebook was the weakest performer out of the bunch, falling 6.9% after announcing the acquisition of Oculus VR for roughly $2 billion in cash and stock.

Staying on the technology theme, the maker of the "Candy Crush" game, King Digital Entertainment (KING 19.00, -3.50), had a forgettable market debut, falling 15.6% in its first session. Although the stock itself holds no sway over the broader market, the disappointing debut likely contributed to the defensive sentiment.

Elsewhere, another influential sector—industrials (-0.9%)—ended among the laggards as transports displayed broad weakness. The Dow Jones Transportation Average lost 1.6% after being unable to take out its 2014 closing high of 7592.36. All 20 index components posted losses with shipper Kirby (KEX 98.78, -3.71) leading the slide with a 3.6% loss.

Equities notwithstanding, the foreign exchange market also reflected a defensive posture as the Japanese yen strengthened, sending the dollar/yen pair below the 102.00 level.

Similarly, Treasuries rallied throughout the session while receiving a boost from a strong $35 billion 5-year note auction. The benchmark 10-yr yield fell five basis points to 2.69%.

With stocks ending on their lows, participants displayed demand for volatility protection, sending the CBOE Volatility Index (VIX 15.20, +1.18) higher by 8.4%.

Trading volume was a bit above average with nearly 738 million shares changing hands at the NYSE.

Today's economic data was limited to just two reports:

The major averages finished the Wednesday session on a cautious note with the S&P 500 falling 0.7%. The Dow Jones Industrial Average (-0.6%) outperformed while small caps bore the brunt of the pressure. The Russell 2000 declined 1.9% while the Nasdaq Composite fell 1.4%.

Equity indices began the day on an upbeat note, but the financial sector (-0.9%) served up an early warning by not taking part in the opening rally. One industry group that briefly participated in the early advance was the biotech space. The iShares Nasdaq Biotechnology ETF (IBB 235.09, -4.35) was up as much as 1.1% during the first hour of action, but faded from the early high, taking the market lower. Interestingly, the broader health care sector (+0.1%) finished the day ahead of the remaining nine groups.

Outside of the relative weakness in biotechnology, the lack of upward momentum in the likes of Amazon.com (AMZN 343.41, -11.30), Facebook (FB 60.38, -4.51), Priceline.com (PCLN 1188.77, -34.93), and Tesla (TSLA 212.96, -7.48) kept the tech-heavy Nasdaq behind the other indices. Facebook was the weakest performer out of the bunch, falling 6.9% after announcing the acquisition of Oculus VR for roughly $2 billion in cash and stock.

Staying on the technology theme, the maker of the "Candy Crush" game, King Digital Entertainment (KING 19.00, -3.50), had a forgettable market debut, falling 15.6% in its first session. Although the stock itself holds no sway over the broader market, the disappointing debut likely contributed to the defensive sentiment.

Elsewhere, another influential sector—industrials (-0.9%)—ended among the laggards as transports displayed broad weakness. The Dow Jones Transportation Average lost 1.6% after being unable to take out its 2014 closing high of 7592.36. All 20 index components posted losses with shipper Kirby (KEX 98.78, -3.71) leading the slide with a 3.6% loss.

Equities notwithstanding, the foreign exchange market also reflected a defensive posture as the Japanese yen strengthened, sending the dollar/yen pair below the 102.00 level.

Similarly, Treasuries rallied throughout the session while receiving a boost from a strong $35 billion 5-year note auction. The benchmark 10-yr yield fell five basis points to 2.69%.

With stocks ending on their lows, participants displayed demand for volatility protection, sending the CBOE Volatility Index (VIX 15.20, +1.18) higher by 8.4%.

Trading volume was a bit above average with nearly 738 million shares changing hands at the NYSE.

Today's economic data was limited to just two reports:

·

Durable goods orders

increased 2.2% in February after falling a downwardly revised 1.3% (from -1.0%)

in January. The Briefing.com consensus expected durable goods orders to

increase 1.0%. The upward headline surprise does not represent a strengthening

in demand from the manufacturing sector. A 6.9% increase in transportation

goods provided most of the increase in February demand. Much of that was

already known, as Boeing (BA 123.53, -0.49) reported 74

aircraft orders in February, up from 38 in January. Altogether, defense and

nondefense aircraft orders increased 15.2%. Excluding transportation, durable

goods orders increased a minor 0.2% in January. That was down from a downwardly

revised 0.9% (from 1.1%) increase in January. The consensus expected these

orders to increase 0.3%.

·

The weekly MBA Mortgage

Applications Index fell 3.5% to follow last week's uptick of 0.2%.

Tomorrow, weekly initial claims

(Briefing.com consensus 330K) and the third estimate of Q4 GDP (consensus 2.6%)

will be released at 8:30 ET while the Pending Home Sales report for February

(expected -0.2%) will cross the wires at 10:00 ET.

·

S&P 500 +0.2%

YTD

·

Nasdaq Composite -0.1%

YTD

·

Russell 2000 -0.6% YTD

·

Dow Jones Industrial

Average -1.9% YTD

Commodities

Closing Commodities: Gold Declines,

But Manages To Stay Above $1300

Commodities ended mostly lower today.

Commodities ended mostly lower today.

·

Metals all posted

losses, excluding iron ore futures, which rose six cents to $111.61/ton

·

Copper futures pulled

back from a 2-week high as concerns in China remain. May copper closed 4 cents

lower at $2.97/lb today

·

Gold and silver sold off

today. Apr gold managed to not break below $1300/oz and closed $7.80 lower at

$1303.40/oz. May silver fell 21 cents to $19.77/oz.

·

Crude oil climbed higher

today to post another session of gains. In the last 12 minutes of pit trading,

crude found more buyers, which pushed it back above $100/barrel and floor

trading came to a close. May crude ended 67 cents higher at

$100.24/barrel.

·

Meanwhile, May natural

gas lost 2 cents to finish at $4.39/MMBtu

COMEX

Metals Closing Prices

·

Apr gold fell $7.80 to

$1303.40/oz

·

May silver fell $0.21 to

$19.77/oz

·

May copper fell 4 cents

to $2.97/lbs

CBOT

Agriculture and Ethanol/ICE Sugar Closing Prices

·

May corn fell 2 cents to

$4.85/bushel

·

May wheat fell 12 cents

to $6.97/bushel

·

May soybeans rose 13

cents to $14.40/bushel

·

Apr ethanol fell 3 cents

to $2.95/gallon

·

May sugar (#16 (U.S.))

rose 0.19 of a penny to 22.08 cents/lbs

NYMEX

Energy Closing Prices; crude oil rallied in the last 12 min of trade and pushed

crude back above $100/barrel by the close

·

May crude oil rose $0.67

to $100.24/barrel

·

Apr natural gas fell 2

cents to $4.39/MMBtu (Nat gas was moved to May contract)

·

May heating oil settled

unchanged at $2.91/gallon

·

May RBOB rose 1 cent to

$2.90/gallon

{kind=link}

Treasuries

Strong 5y Auction Lifts Treasuries:

10-yr: +11/32..2.704%..USD/JPY: 102.04..EUR/USD: 1.3794

·

Treasuries closed on

their highs, buoyed by today's strong $35 bln 5y note auction. Click here to see an intraday 5y

chart.

·

The complex drifted

little changed into this morning's durable orders (2.2% actual v. 1.0%

expected) data, and caught a bid despite the headline beat as aircraft orders

were responsible the bulk of the gains.

·

A steady bid continued

into the lunchtime hour with action forming a floor into this afternoon's $35

bln 5y note auction.

·

The auction drew 1.715%

and a solid 2.99x bid/cover. Indirect (50.9%) and direct (23.1%) bidders saw

takedowns well above their 12-auction averages, leaving primary dealers

with just 26% of the supply and their lowest takedown on record.

·

Post-data buying dropped

yields to session lows, where they would hold for the remainder of the

afternoon.

·

The 5y shed -4.4bps to

finish the day @ 1.677%, a one-week low. The yield has spent much of the past

week hovering near key trendline resistance off the September highs that lurks

in the 1.725% area.

·

The 10y settled -3.4bps

@ 2.701%. Today's bid dropped the benchmark yield below its 50 dma with action

settling on the 200 dma. The 2.600% level will be under close watch in the days

ahead.

·

At the long end, the

30y slipped -2.8bps to 3.551%, its lowest in almost two months. This area

remains critical as a breakdown sets up the potential for a move into

3.150%.

·

A

flatter curve took hold as the 2-10-yr spread narrowed to 226bps.

·

Precious metals ended on

their lows with gold -$11 @ $1300 and silver -$0.28 @ $19.70.

·

Data: Initial and continuing claims, GDP - Third

Estimate (8:30), and pending home sales (10).

·

Auction: $29 bln 7y notes.

·

Fed

Speak: STL's Bullard remains

in Hong Kong to discuss "What are the Prospects for U.S. Monetary

Policy" (20:20). Chicago's Evans will be in Hong Kong, discussing the

economy and monetary policy (21:30).

{kind=link}

Next Day In View

Economic Commentary

Economic Summary: Durable Goods

orders top expectations; Q4-GDP Third Estimate due out tomorrow at 8:30

Economic Data Summary:

Economic Data Summary:

·

Weekly MBA Mortgage

Applications -3.5% vs Briefing.com consensus of ; Last Week was -1.2%

·

February

Durable Orders 2.2% vs Briefing.com consensus of 1.0%; January was -1.0%

·

February Durable Goods

Ex-Transpiration 0.2% vs Briefing.com consensus of 0.3%; January was -1.1%

o The upward headline surprise does not represent

a strengthening in demand from the manufacturing sector. A 6.9% increase in

transportation goods provided most of the increase in February demand. Much of

that was already known, as Boeing (BA) reported 74 aircraft orders in February,

up from 38 in January. Altogether, defense and nondefense aircraft orders

increased 15.2%. Excluding transportation, durable goods orders increased a

minor 0.2% in February.

Upcoming Economic Data:

·

Weekly Initial Claims

due out Weekly at 8:30 (Briefing.com consensus of 330K; Last Week was 320K)

·

Weekly Continuing Claims

due out Weekly at 8:30 (Briefing.com consensus of 2.9 M ; Last Week was 2.889 M

)

·

Fourth

Quarter GDP- Third Estimate due out Fourth Quarter at 8:30 (Briefing.com

consensus of 2.6%; Third Quarter was 2.4%)

·

Fourth

Quarter GDP Deflator- Third Estimate due out Fourth Quarter at 8:30

(Briefing.com consensus of 1.6%; Third Quarter was 1.6%)

·

February Pending Home

Sales due out February at 10:00 (Briefing.com consensus of -0.2%; January was

0.1%)

Upcoming Fed/Treasury Events:

·

Cleveland Sandra

Pianalto (voting FOMC member, typically dovish) to speak tomorrow at 8:30

·

Saint Louis Fed

President James Bullard (not a voting FOMC member, dovish) to speak tomorrow at

20;20

·

Chicago Fed President

Charlie Evans (not a voting FOMC member, dovish) to speak tomorrow at 21:30

Other International Events of

Interest

·

The latest Reserve Bank

of Australia Financial Stability Review warned that low rates cannot last

forever, and coincided with a speech from RBA Governor Stevens that warned of

the dangers of a continued increase in home prices

On other news....

Fed announces second round of CCAR

results

·

The Federal Reserve on

Wednesday announced it has approved the capital plans of 25 bank holding

companies participating in the Comprehensive Capital Analysis and Review

(CCAR). The Federal Reserve objected to the plans of the other five

participating firms--four based on qualitative concerns and one because it did

not meet a minimum post-stress capital requirement.

·

Strong capital levels

help ensure that banking organizations have the ability to lend to households

and businesses and to continue to meet their financial obligations, even in

times of economic difficulty. Now in its fourth year, the Federal Reserve in

CCAR evaluates the capital planning processes and capital adequacy of the

largest bank holding companies, including the firms' proposed capital actions

such as dividend payments and share buybacks and issuances.When considering an

institution's capital plan, the Federal Reserve considers both qualitative and

quantitative factors. These include a firm's capital ratios under severe

economic and financial market stress and the strength of the firm's capital

planning process. After the Federal Reserve objects to a capital plan, the

institution may only make capital distributions with prior written approval

from the Federal Reserve.

·

"The Federal

Reserve's annual capital plan assessment provides a structured and comparative

way to promote and assess the capacity of large bank holding companies to understand

and manage their capital positions," Federal Reserve Gov. Daniel Tarullo

said. "With each year we have seen broad improvement in the industry's

ability to assess its capital needs under stress and continuing improvements to

the risk-measurement and -management practices that support good capital

planning. However, both the firms and supervisors have more work to do as we

continue to raise expectations for the quality of risk management in the

nation's largest banks."The Federal Reserve can object to a capital plan

based on qualitative or quantitative concerns, or both. The Federal Reserve can

require a new capital plan from an institution outside of the annual review at

any time if there is a material change in the condition of an individual

institution or in the economy or financial markets that could potentially lead

to a change in a firm's capital position.

·

The

Federal Reserve did not object to the capital plans for Ally Financial Inc.; American Express

Company; Bank of America Corporation; The Bank of New York Mellon Corporation;

BB&T Corporation; BBVA Compass Bancshares, Inc.; BMO Financial Corp.;

Capital One Financial Corporation; Comerica Incorporated; Discover Financial

Services; Fifth Third Bancorp; The Goldman Sachs Group, Inc.; Huntington Bancshares

Incorporated; JP Morgan Chase & Co.; Keycorp; M&T Bank Corporation;

Morgan Stanley; Northern Trust Corporation; The PNC Financial Services Group,

Inc.; Regions Financial Corporation; State Street Corporation; SunTrust Banks,

Inc.; U.S. Bancorp; UnionBanCal Corporation; and Wells Fargo &

Company.

·

Bank

of America Corporation and The Goldman Sachs Group, Inc., met minimum capital

requirements after submitting adjusted capital actions.

·

Based on qualitative

concerns, the Federal Reserve objected to the capital plans of

Citigroup Inc.; HSBC North America Holdings Inc.; RBS Citizens Financial Group,

Inc.; and Santander Holdings USA, Inc.

o The Federal Reserve objected to the capital plan

of Zions Bancorporation because the firm did not meet the minimum, post-stress

tier-1 common ratio of 5 percent.U.S. firms have substantially increased their

capital since the first set of government stress tests in 2009.

·

The aggregate tier 1

common equity ratio, which compares high-quality capital to risk-weighted

assets, of the 30 bank holding companies in the 2014 CCAR has more than doubled

from 5.5 percent in the first quarter of 2009 to 11.6 percent in the fourth

quarter of 2013, reflecting an increase in tier 1 common equity of more than

$511 billion to $971 billion during the same period.That trend is expected to

continue.

o All but two of the 30 participants in this

year's CCAR are expected to build capital from the second quarter of 2014

through the first quarter of 2015. In the aggregate, the firms are expected to

distribute 40 percent less than their projected net income during the same

period. The 30 institutions in CCAR this year have a combined $13.5 trillion in

assets, or approximately 80 percent of all U.S. bank holding company assets.

Currencies

Dollar Hovers Little Changed: 10-yr:

+11/32..2.700%..USD/JPY: 101.95..EUR/USD: 1.3788

·

The Dollar Index trades

little changed as action hovers near the 80.00 level. Click here to see a daily Dollar

Index chart.

·

The Index has been bid

throughout the session, aside from a quick dip into the red in recent

trade.

·

EURUSD is -40 pips @ 1.3785 as sellers remain in

control for a second session. Today's weakness has the single currency looking

at another test of 1.3750 support, which has held up since the middle of

February. Eurozone data due out tomorrow includes M3 money supply and private

loans.

·

GBPUSD is +35 pips @ 1.6565 as steady buying persists

for a third session. An early afternoon bid lifted the pair to 1.6600 resistance,

but sellers emerged at the level and have managed to push action back down to

the 50 dma (1.6565). British data out tomorrow is limited to retail

sales.

·

USDCHF is +20 pips @ .8845 as action continues to press

resistance in the area. The pair has struggled at the .8875 area for much of

the past week, but buyers remain steadfast in their efforts to retake the

level. The .8950 region remains key as both the 50 and 100 dma aid resistance

in the area.

·

USDJPY is -25 pips @ 102.00 as action presses

to a one-week low. The 102.50 area has been problematic for

bulls as of late as action has tested the level in each of the last six

sessions. Attention now turns to the lower end of the range near 101.50.

·

AUDUSD is +70 pips @ .9225 as trade holds at

four-month highs. Today's advance in the hard currency was sparked by the

latest Reserve Bank of Australia Financial Stability Report and comments by RBA

Governor Glenn Stevens, both of which suggested rates cannot stay low forever

and warned on the level of home prices. The .9300 area provides the next

level of resistance.

·

USDCAD is -55 pips @ 1.1110 as sellers remain in charge

for a fourth day. The skid has dropped action onto support in the 1.1100 area,

which is aided by the 50 dma.

Jason's Commentaries

It has been increasingly difficult to read the market. Right now, the market has been in a very volatile state, having a one up day, one down day thing again. The market started last night with a lot of divergence once again. And right after the huge spike at the opening bell, the market started to sell against the market makers and push the market all the way down. By lunch time, the market decided to break down even further. The main laggard of the day is the Tech then Financials then industrials. However, if you look at the bigger picture. IT"S ALL RED. While looking at the internals, volumes are at 751.3m shares traded. Suggesting that there are a lot of commitment right now and the internals were favoring the bears. Moreover, looking at the internals, we have the Russells and Nasdaq breaking down from it's trendline. It's time to go short time bear! S&P500 and Dow remained lagged as well. Nonethless, I'm turning bear for this short term. Especially China is producing so much unfavourable news that could drag down Asia. Stay safe, stay bear people!

Market Call: DOWN

Date: 27 March 2014

No comments:

Post a Comment