30 April 2014 AMC- Market ended higher as Fed maintains $10b taper course

Market Summary

European

Markets Closing Prices

European

markets are now closed; stock markets across Europe performed as follows:

·

UK's FTSE: + 0.2%

·

Germany's DAX: + 0.2%

·

France's CAC: -0.2%

·

Spain's IBEX: 0.0%

·

Portugal's PSI: + 0.2%

·

Italy's MIB Index: -0.9%

·

Irish Ovrl Index: + 0.4%

·

Greece ATHEX Composite: + 3.1%

Before Market Opens

S&P futures vs fair value:

-2.40. Nasdaq futures vs fair value: -10.80.

The S&P 500 futures trade two points below fair value.

Asian markets ended mixed, with Hong Kong's Hang Seng (-1.4%) trailing the remainder of the region. Elsewhere, the Bank of Japan met overnight, but the subsequent statement was a non-event as the central bank opted to maintain its current policy stance.

Economic data was plentiful. Japan's Manufacturing PMI fell to 49.4 from 53.9 (53.0 expected) and Industrial Production ticked up 0.3% month-over-month (expected 0.5%, prior -2.3%). Separately, Average Cash Earnings increased 0.7% year-over-year (consensus 0.2%, prior -0.1%), Construction Orders fell 8.8% year-over-year (prior 12.3%), and Housing Starts decreased 2.9% year-over-year, as expected (previous 1.0%). South Korea's Industrial Production rose 2.7% year-over-year (expected 3.7%, prior 4.3%), while Retail Sales fell 0.3% month-over-month (consensus 0.5%, prior -3.2%). Singapore's Unemployment Rate increased to 2.1% from 1.8% (expected 1.8%). Australia's Private Sector Credit expanded 0.4% month-over-month, as expected. New Zealand's Building Consents jumped 8.3% month-over-month (expected 2.0%, previous -1.6%), while ANZ Business Confidence slipped to 64.8% from 67.3%.

The S&P 500 futures trade two points below fair value.

Asian markets ended mixed, with Hong Kong's Hang Seng (-1.4%) trailing the remainder of the region. Elsewhere, the Bank of Japan met overnight, but the subsequent statement was a non-event as the central bank opted to maintain its current policy stance.

Economic data was plentiful. Japan's Manufacturing PMI fell to 49.4 from 53.9 (53.0 expected) and Industrial Production ticked up 0.3% month-over-month (expected 0.5%, prior -2.3%). Separately, Average Cash Earnings increased 0.7% year-over-year (consensus 0.2%, prior -0.1%), Construction Orders fell 8.8% year-over-year (prior 12.3%), and Housing Starts decreased 2.9% year-over-year, as expected (previous 1.0%). South Korea's Industrial Production rose 2.7% year-over-year (expected 3.7%, prior 4.3%), while Retail Sales fell 0.3% month-over-month (consensus 0.5%, prior -3.2%). Singapore's Unemployment Rate increased to 2.1% from 1.8% (expected 1.8%). Australia's Private Sector Credit expanded 0.4% month-over-month, as expected. New Zealand's Building Consents jumped 8.3% month-over-month (expected 2.0%, previous -1.6%), while ANZ Business Confidence slipped to 64.8% from 67.3%.

·

Japan's Nikkei (+0.1%) eked out a slim gain with help

from industrials. Mitsubishi Electric and Komatsu gained 3.1% and 2.6%,

respectively.

·

Hong

Kong's Hang Seng (-1.4%) ended

near its low amid weakness in blue chip names. Li & Fung lost 2.6% and

Tencent Holdings tumbled 5.2%. On the upside, telecom names built on

yesterday's gains, with China Unicom climbing 5.9%.

·

China's Shanghai Composite (+0.3%) posted a modest gain,

with support from media names. Zhe Jiang Daily Media surged 8.2%.

Major European indices trade in

mixed fashion after a barrage of economic data. Eurozone CPI increased 0.7%

year-over-year (consensus 0.8%, prior 0.5%), while Core CPI rose 1.0% (forecast

1.0%, previous 0.7%). Germany's Unemployment count declined 25,000 (expected

-10,000, prior -14,000), while the Unemployment Rate held steady at 6.7%, as

expected. Also of note, Retail Sales fell 0.7% month-over-month (consensus

-0.7%, prior 0.4%) and the year-over-year reading declined 1.9% (expected

+1.6%, prior 1.9%). French PPI fell 0.4% month-over-month (expected -0.3%,

previous -0.1%), while Consumer Spending rose 0.4% month-over-month (consensus

0.3%, prior -0.1%). Italy's CPI rose 0.6% year-over-year, as expected, while

PPI fell 1.6% year-over-year (consensus -1.3%, last -1.4%). Separately, Monthly

Unemployment Rate held steady at 12.7% (expected 13.0%). Spain's GDP rose 0.4%

quarter-over-quarter, as expected, while the year-over-year reading indicated

an expansion of 0.6% (expected 0.5%). Also of note, Retail Sales fell 0.5%

year-over-year (expected 0.1%, prior -0.4%).

Among news of note, the euro rallied following the softer-than-expected CPI reading on the belief that the slight miss is not enough to force the European Central Bank into action. Currently, the single currency trades near 1.3860 against the dollar.

Among news of note, the euro rallied following the softer-than-expected CPI reading on the belief that the slight miss is not enough to force the European Central Bank into action. Currently, the single currency trades near 1.3860 against the dollar.

·

Italy's MIB holds a loss of 0.7% amid weakness in

financials. Banca Popolare dell'Emilia Romagna, Banco Popolare, and BMPS are

down between 1.7% and 3.1%.

·

In

France, the CAC is lower by

0.5% as utilities weigh. GDF Suez and Veolia Environnement hold respective

losses of 3.6% and 5.2%. BNP Paribas is also among the laggards, down

4.4%.

·

Germany's DAX trades up 0.1%. Financials lag, while producers

of basic materials outperform. Commerzbank and Deutsche Bank are both down near

1.0%. On the upside, K+S and ThyssenKrupp trade higher by 1.8% and 1.1%,

respectively.

·

Great

Britain's FTSE outperforms with a

slight gain of 0.2%. Energy names lead, with Royal Dutch Shell and Tullow Oil

up 4.4% and 2.8%, respectively. Insurer Admiral Group is the weakest performer,

down 3.1%.

U.S. Equities

·

Equity futures point to

little change at the open as traders await this afternoon's FOMC rate decision

·

Both the DJIA and

S&P 500 hold within 1% of their all-time closing highs

·

MBA Mortgage Index

(-5.9% actual)

·

ADP Employment Change

(220K actual v. 215K expected)

·

GDP-Adv. (0.1% actual v.

1.0% expected)

·

GDP Deflator-Adv. (1.3%

actual v. 1.8% expected)

·

Employment Cost Index

(0.3% actual v. 0.5% expected)

o S&P Futures -1 @ 1871

o Dow Futures unch @ 14,467

o Nasdaq Futures -10 @ 3554

Asia

·

Markets ended mixed

across Asia.

·

Japan's Nikkei (+0.1%)

eked out a gain after the Bank of Japan kept policy unchanged and suggested

inflation would hit its 2% target in two years.

·

China's Shanghai

Composite (+0.3%) saw a boost from earnings while Hong Kong's Hang Seng (-1.4%)

was hit by a wave of profit-taking ahead of the two-day holiday.

·

Australia's ASX (+0.1%)

and India's Sensex (-0.2%) finished little changed.

Market Internals

Market Internals -Technical-

The S&P 500 closed up 6 (+0.30%) at 1884, the Dow closed up 45 (+0.27%) at 16581, and the Nasdaq closed up 11 (+0.27%) at 4115. Action came on mixed volume (NYSE 892 mln vs. avg. of 730; NASDAQ 1909 mln vs. avg. of 2009), with advancers outpacing decliners (NYSE 2067/1039, NASDAQ 1520/1144) and mixed new highs/lows (NYSE 108/38, NASDAQ 46/74).

Relative Strength:

Greece-GREK +-3.53%, Turkey-TUR +-2.72%, New Zealand-ENZL +-2.1%, Peru-EPU +-1.71%, Nordic 30-GXF +-1.65%, Telecommunications-IYZ +1.52%, Wind Energy-FAN +1.36%, Timber-CUT +1.11%, Sugar-SGG +1.05%, Technology-Software-IGV +1.03%.

Relative Weakness:

Middle East and Africa-GAF -2.56%, Coffee-JO -2.31%, Hong Kong-EWH -1.84%, Copper-JJC -1.76%, Junior Gold Miners-GDXJ -1.75%, Silver-SLV -1.6%, Heating Oil-UHN -1.52%, South Korea-EWY -0.89%, Taiwan-EWT -0.81%, Israel-EIS -0.75%.

Leaders and Laggards

Technical Updates

{kind=link}

{kind=link}

{kind=link}

Briefing's Commentaries

Closing Market Summary: Stocks and

Bonds Climb While Fed Tapers Again

Equity indices spent some time on either side of their respective flat lines on Wednesday, but when the dust settled, they ended with modest gains. The Dow Jones Industrial Average, S&P 500, and Nasdaq all added 0.3%, with the Dow registering a new record closing high at 16,580.84, which represented its first green close for the year.

Today's session featured another heavy dose of earnings and a full slate of economic data. Prior to the open, index futures jumped in reaction to a better-than-expected ADP Employment report, but promptly surrendered those gains when it was reported that GDP increased a puny 0.1% in the first quarter (Briefing.com consensus 1.0%).

The disappointing report ensured a lower start for the major averages, but they only took one more step down before forging a rebound on the back of the industrial sector (+0.5%), which drew strength from transports. The Dow Jones Transportation Average jumped 0.7%, bolstered by above-consensus earnings reported by C.H. Robinson (CHRW 58.90, +2.91).

The S&P 500 and Dow were able to reclaim their flat lines within the first hour of action, while the Nasdaq remained in the red a bit longer as biotechnology and high-beta tech names weighed.

After clawing back to unchanged, the key indices maintained narrow ranges until the Federal Open Market Committee released its latest policy statement, which called for another $10 billion reduction to monthly asset purchases, lowering the total to $45 billion.

There were few changes overall in the language the FOMC used to communicate its stance. One switch came in the opening sentence as the committee acknowledged that growth in economic activity has picked up recently, after having slowed sharply during the winter in part because of adverse weather conditions. In March, the directive stated that "growth in economic activity slowed during the winter months, in part reflecting adverse weather conditions."

What that opening sentence, and the decision to cut another $10 billion from its monthly asset purchases implied, was that the FOMC is clearly expecting pent-up demand to shine through in the second quarter and to overshadow the feeble 0.1% GDP growth rate for the first quarter.

In any event, equity indices gyrated a bit following the release, but climbed to new session highs into the close. The late-afternoon move allowed the Nasdaq to catch up to its peers, while also giving a boost to biotechnology. The iShares Nasdaq Biotechnology ETF (IBB 230.25, +1.16) gained 0.5%, while the broader health care sector (+0.1%) underperformed amid weakness in Express Scripts (ESRX 66.58, -4.43) after the company reported disappointing quarterly results.

The post-FOMC move also lifted some of the high-beta tech names off their lows, but shares of Twitter (TWTR 38.97, -3.65) still finished at a new all-time low after reporting its quarterly results. The stock tumbled 8.6% after Twitter's disappointing user growth overshadowed its above-consensus earnings.

On the downside, the energy sector (-0.01%) ended just below its flat line, but still finished April ahead of the remaining nine groups with a gain of 5.1%.

Treasuries retreated overnight, but reversed course following this morning's GDP report. The 10-yr note advanced 12 ticks, pressuring its yield four basis points to 2.65%.

Boosted by month-end flows, trading volume was above average as 892 million shares changed hands at the NYSE floor.

Reviewing today's data:

Equity indices spent some time on either side of their respective flat lines on Wednesday, but when the dust settled, they ended with modest gains. The Dow Jones Industrial Average, S&P 500, and Nasdaq all added 0.3%, with the Dow registering a new record closing high at 16,580.84, which represented its first green close for the year.

Today's session featured another heavy dose of earnings and a full slate of economic data. Prior to the open, index futures jumped in reaction to a better-than-expected ADP Employment report, but promptly surrendered those gains when it was reported that GDP increased a puny 0.1% in the first quarter (Briefing.com consensus 1.0%).

The disappointing report ensured a lower start for the major averages, but they only took one more step down before forging a rebound on the back of the industrial sector (+0.5%), which drew strength from transports. The Dow Jones Transportation Average jumped 0.7%, bolstered by above-consensus earnings reported by C.H. Robinson (CHRW 58.90, +2.91).

The S&P 500 and Dow were able to reclaim their flat lines within the first hour of action, while the Nasdaq remained in the red a bit longer as biotechnology and high-beta tech names weighed.

After clawing back to unchanged, the key indices maintained narrow ranges until the Federal Open Market Committee released its latest policy statement, which called for another $10 billion reduction to monthly asset purchases, lowering the total to $45 billion.

There were few changes overall in the language the FOMC used to communicate its stance. One switch came in the opening sentence as the committee acknowledged that growth in economic activity has picked up recently, after having slowed sharply during the winter in part because of adverse weather conditions. In March, the directive stated that "growth in economic activity slowed during the winter months, in part reflecting adverse weather conditions."

What that opening sentence, and the decision to cut another $10 billion from its monthly asset purchases implied, was that the FOMC is clearly expecting pent-up demand to shine through in the second quarter and to overshadow the feeble 0.1% GDP growth rate for the first quarter.

In any event, equity indices gyrated a bit following the release, but climbed to new session highs into the close. The late-afternoon move allowed the Nasdaq to catch up to its peers, while also giving a boost to biotechnology. The iShares Nasdaq Biotechnology ETF (IBB 230.25, +1.16) gained 0.5%, while the broader health care sector (+0.1%) underperformed amid weakness in Express Scripts (ESRX 66.58, -4.43) after the company reported disappointing quarterly results.

The post-FOMC move also lifted some of the high-beta tech names off their lows, but shares of Twitter (TWTR 38.97, -3.65) still finished at a new all-time low after reporting its quarterly results. The stock tumbled 8.6% after Twitter's disappointing user growth overshadowed its above-consensus earnings.

On the downside, the energy sector (-0.01%) ended just below its flat line, but still finished April ahead of the remaining nine groups with a gain of 5.1%.

Treasuries retreated overnight, but reversed course following this morning's GDP report. The 10-yr note advanced 12 ticks, pressuring its yield four basis points to 2.65%.

Boosted by month-end flows, trading volume was above average as 892 million shares changed hands at the NYSE floor.

Reviewing today's data:

·

The ADP Employment

report indicated that employment in the nonfarm private business sector rose by

220K in April, which was above the increase of 215K expected by the

Briefing.com consensus.

·

Q1 GDP increased 0.1%

quarter-over-quarter, which represented the lowest quarterly increase since GDP

rose by the same amount in Q4 2012. The Briefing.com consensus expected GDP to

increase 1.0%. Many analysts over the last couple months have theorized that

the softness in the first quarter is the result of extreme winter weather

conditions. In our opinion, economic growth has tended to slow during the first

half of the year for the past several years. The slowdown in Q1 2014 was not

extraordinary and we do not expect a snap back from pent up demand to occur

immediately in Q2 2014.

·

Manufacturing activities

in the Chicago region rebounded in April as the Chicago PMI jumped to 63.0 from

55.9 that was reported in March. That was the strongest reading since the index

reached 66.6 in October. The Briefing.com consensus expected the PMI to

increase to 56.5. The increase in the Chicago PMI was predicated on a large

boom in production. The production index jumped to 70.5 in April from 61.7 in

March. More importantly, a solid increase in order backlogs (54.9 from 50.4) is

likely to keep upward pressure on production growth over the next few

months.

·

The weekly MBA Mortgage

Index fell 5.9% to follow last week's decline of 3.2%.

Tomorrow, the Challenger Job Cuts

report for April will be released at 7:30 ET, while weekly initial claims,

March Personal Income, Personal Spending, and core PCE Prices will all be

reported at 8:30 ET. March Construction Spending and the April ISM Index will

both be released at 10:00 ET, while auto and truck makers will be reporting

their April sales throughout the day.

·

S&P 500 +1.9%

YTD

·

Dow Jones Industrial

Average +0.03% YTD

·

Nasdaq Composite -1.5%

YTD

·

Russell 2000 -2.9% YTD

Commodities

Closing Commodities: Gold Ends 20

Cents Lower, Silver Drops 1.9%

·

June gold traded in the

red for most of today's floor trade as investors awaited the release of the

FOMC's latest policy statement at 14:00ET.

·

The yellow metal popped

to a session high of $1297.50 per ounce after it was reported that Q1 GDP rose

by just 0.1% vs a 1.0% increase expected by the Briefing.com consensus, but

quickly fell back into negative territory.

·

It gained some momentum

heading into the close and settled at $1296.00 per ounce, just 20 cents below

the unchanged line.

·

July silver pulled back

from its session high of $19.44 per ounce set in early morning action and

traded as low as $19.08 per ounce. Unable to find buying support, it settled

with a 1.9% loss at $19.16 per ounce.

·

June crude oil fell for

the first time in three sessions as the EIA reported that inventories for the

week ending April 25 gained 1.698 mln barrels to a total of 399.4 mln barrels,

the highest level since the EIA began reporting data in 1982.

·

Consensus called for a

build of 2.1-2.4 mln barrels. The energy component dipped to a session low of

$99.34 per barrel and eventually settled at $99.78 per barrel, or 1.5%

lower.

·

June natural gas rallied

to a session high of $4.85 per MMBtu in afternoon action after trading as low

as $4.75 per MMBtu in the session. It sold off back into the red as it headed

into the close and settled with a 0.2% loss at $4.82 per MMBtu.

COMEX

Metals Closing Prices

June gold fell $0.20 to $1296.00/oz

·

Gold traded in the red

for most of today's floor trade as investors awaited the release of the Federal

Reserve's latest policy statement at 14:00ET. The yellow metal popped to a

session high of $1297.50 after it was reported that Q1 GDP rose by just 0.1% vs

a 1.0% increase expected by the Briefing.com consensus, but quickly fell back

into negative territory. It gained some momentum heading into the close and

settled just 20 cents below the unchanged line.

July silver fell $0.38 to $19.16/oz

·

Silver pulled back from

its session high of $19.44 set in early morning action and traded as low as

$19.08. Unable to find buying support, it settled with a 1.9% loss.

July

copper fell 4 cents to $3.03/lbs

CBOT

Agriculture and Ethanol/ICE Sugar Closing Prices

·

July

corn fell 3 cents to

$5.19/bushel

·

July

wheat rose 6 cents to

$7.22/bushel

·

July

soybeans fell 4 cents to $15.12/bushel

·

May

ethanol fell 4 cents to

$2.26/gallon

·

July

sugar (#16 (U.S.)) rose 0.11

of a penny to 24.45 cents/lbs

NYMEX

Energy Closing Prices

June crude oil fell $1.49 to $99.78/barrel

·

Crude oil fell for the

first time in three sessions as the EIA reported that inventories for the week

ending Apr 25 had a build of 1.698 mln barrels when a build of 2.1-2.4 mln

barrels was anticipated. The gain brought stockpiles to a total of 399.4 mln

barrels, the highest level since the EIA began reporting data in 1982. The

energy component dipped to a session low of $99.34 and eventually settled with

a 1.5% loss.

June natural gas fell 1 cent to $4.82/MMBtu

·

Natural gas rallied to a

session high of $4.85 in afternoon action after trading as low as $4.75 earlier

in the session. It sold off back into the red as it headed into the close and

settled with a 0.2% loss.

June heating oil fell 3 cents to $2.93/gallon

June

RBOB fell 5 cents to $2.96/gallon{kind=link}

Treasuries

Treasuries Rally as Fed Tapers:

10-yr: +10/32..2.657%..USD/JPY: 102.15..EUR/USD: 1.3869

·

Treasuries closed on their

highs as buyers emerged in response to the latest Fed taper. Click here to see an intraday

yields chart.

·

The

FOMC announced "growth in economic activity picked up recently, after

having slowed sharply during the winter in part because of adverse weather

conditions," and that it was reducing its monthly asset purchases from $55

bln to $45 bln.

·

The Treasury complex saw

light overnight selling give a boost to yields ahead of the cash open with

yields running to session highs following the strong ADP Employment

Change (220K actual v. 215K expected).

·

The bear case was

short-lived as the GDP-Adv. (0.1% actual v. 1.0% expected) miss produced

a sharp reversal and maturities rallied into positive territory.

·

A choppy trade persisted

into early afternoon action before the post-FOMC bid dropped yields to session

lows at the close.

·

Aggressive buying

dropped the 5y -6bps to 1.681%. The yield flushed below 1.700% support, setting

up a test of the 1.650% area that is defended by both the 50 and 100 dma.

·

The 10y shed -4.7bps to

close @ 2.648%. Many traders have the 2.600% level in the cross hairs as that

level marks the lower bound of the 2.600%/2.800% range that has held up since

the beginning of February.

·

At the long end, the 30y

lagged throughout the session before ending lower by -3.3bps @ 3.458%. The

yield on the long bond narrowly avoided its lowest close in 10 months.

·

Today's

bid swung the curve steeper as the 5-30-yr spread widened to 177.5bps.

·

Precious metals saw a

third straight day of selling as gold fell -$5 to $1291 and silver shed $0.33

to $19.15.

·

Data: Challenger Job Cuts (7:30), initial and

continuing claims, personal income and spending, PCE Prices - Core (8:30), ISM

Index, construction spending (10), and auto/truck sales (14).

·

Fed

Speak: Fed Chair Janet Yellen

will speak at the Independent Community Bankers of America Annual Washington

Policy Summit (8:30).

{kind=link}

Next Day In View

Economic Commentary

Economic Summary: Fed tapers by $10

bln; GDP grows only at 0.1%, missing expectations; Chicago PMI blows past

estimates; Yellen to speak tomorrow at 8:30

Economic Data Summary:

Economic Data Summary:

·

Weekly MBA Mortgage

Applications -5.9% (Last Week was -3.3%).

·

April ADP Employment

Change 220K vs Briefing.com consensus of 215K; March was 191K

·

First

Quarter GDP- Advance 0.1% vs Briefing.com consensus of 1.0%; Fourth Quarter was

2.6%

o Many analysts over the last couple months

have theorized that the softness in the first quarter is the result of extreme

winter weather conditions. In our opinion, economic growth has tended to slow

during the first half of the year for the past several years. The slowdown in

Q1 2014 was not extraordinary and we do not expect a snap back from pent up demand

to occur immediately in Q2 2014. Real final sales, which exclude inventories,

increased 0.7%. That was down from a 2.7% gain in Q4 2013 and the weakest gain

since final sales increased 0.2% in Q1 2013. The one bright spot was

consumption. Real personal spending increased by a solid 3.0% after increasing

3.3% in Q4 2013. That was the first time since 2005 that spending exceeded 3.0%

for two consecutive quarters. Unfortunately, most of the gain was a result of a

4.4% increase in services spending, which was a result of higher utilities

bills from the harsh winter.

·

First Quarter Chain

Deflator Advance 1.3% vs Briefing.com consensus of 1.8%; Fourth Quarter was

1.6%

·

First Quarter Employment

Cost Index 0.3% vs Briefing.com consensus of 0.5%; Fourth Quarter was 0.5%

·

April

Chicago PMI 63.0 vs Briefing.com consensus of 56.5; March was 55.9

o The production index jumped to 70.5 in April

from 61.7 in March. More importantly, a solid increase in order backlogs (54.9

from 50.4) will keep upward pressure on production growth over the next few

months. New orders levels strengthened as the related index increased to 68.7

in April from 58.8 in March. The Employment Index increased to 57.8 in April.

That nearly erased the entire March loss when the index fell to 50 from 59.3 in

February.

Fed/Treasury Events Summary:

·

Fed

tapered its asset purchases to $45 bln from $55 bln last month ($20 bln in MBS

and $25 bln in treasuries).

·

Apr 30: Information

received since the Federal Open Market Committee met in March indicates that

growth in economic activity has picked up recently, after having slowed

sharply during the winter in part because of adverse weather conditions...

Mar 19: Information received since the Federal Open Market Committee met in

January indicates that growth in economic activity slowed during the winter

months, in part reflecting adverse weather conditions.

Upcoming Economic Data:

·

April Challenger Job

Cuts due out Thursday at 7:30 (Briefing.com consensus of ; March was -30.2%)

·

Weekly Initial claims

due out Thursday at 8:30 (Briefing.com consensus of 315K; Last Week was 329K)

·

Weekly Continuing Claims

due out Thursday at 8:30 (Briefing.com consensus of 2.752 M ; Last Week was 2.680

M )

·

March Personal Income

due out Thursday at 8:30 (Briefing.com consensus of 0.4%; February was 0.3%)

·

March Personal Spending

due out Thursday at 8:30 (Briefing.com consensus of 0.6%; February was 0.3%)

·

March PCE Prices -- CORE

due out Thursday at 8:30 (Briefing.com consensus of 0.2%; February was 0.1%)

·

April ISM Index due out

Thursday at 10:00 (Briefing.com consensus of 54.5; March was 53.7)

·

April Construction

Spending due out Thursday at 10:00 (Briefing.com consensus of 0.4%; March was

0.1%)

Upcoming Fed/Treasury Events:

·

Fed

Chair Janet Yellen scheduled to speak tomorrow at 8:30

Other International Events of

Interest

·

Eurozone CPI Flash

Estimate (0.7% YoY actual v. 0.8% YoY expected) fell short of estimates,

sparking more speculation the European Central Bank will be forced to launch a

QE-style program sooner rather than later.

On other news....

Federal Reserve releases FOMC statement

Information received since the Federal Open Market Committee met in March indicates that growth in economic activity has picked up recently, after having slowed sharply during the winter in part because of adverse weather conditions. Labor market indicators were mixed but on balance showed further improvement. The unemployment rate, however, remains elevated. Household spending appears to be rising more quickly. Business fixed investment edged down, while the recovery in the housing sector remained slow. Fiscal policy is restraining economic growth, although the extent of restraint is diminishing. Inflation has been running below the Committee's longer-run objective, but longer-term inflation expectations have remained stable.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. The Committee expects that, with appropriate policy accommodation, economic activity will expand at a moderate pace and labor market conditions will continue to improve gradually, moving toward those the Committee judges consistent with its dual mandate. The Committee sees the risks to the outlook for the economy and the labor market as nearly balanced. The Committee recognizes that inflation persistently below its 2 percent objective could pose risks to economic performance, and it is monitoring inflation developments carefully for evidence that inflation will move back toward its objective over the medium term.

The Committee currently judges that there is sufficient underlying strength in the broader economy to support ongoing improvement in labor market conditions. In light of the cumulative progress toward maximum employment and the improvement in the outlook for labor market conditions since the inception of the current asset purchase program, the Committee decided to make a further measured reduction in the pace of its asset purchases. Beginning in May, the Committee will add to its holdings of agency mortgage-backed securities at a pace of $20 billion per month rather than $25 billion per month, and will add to its holdings of longer-term Treasury securities at a pace of $25 billion per month rather than $30 billion per month. The Committee is maintaining its existing policy of reinvesting principal payments from its holdings of agency debt and agency mortgage-backed securities in agency mortgage-backed securities and of rolling over maturing Treasury securities at auction. The Committee's sizable and still-increasing holdings of longer-term securities should maintain downward pressure on longer-term interest rates, support mortgage markets, and help to make broader financial conditions more accommodative, which in turn should promote a stronger economic recovery and help to ensure that inflation, over time, is at the rate most consistent with the Committee's dual mandate.

The Committee will closely monitor incoming information on economic and financial developments in coming months and will continue its purchases of Treasury and agency mortgage-backed securities, and employ its other policy tools as appropriate, until the outlook for the labor market has improved substantially in a context of price stability. If incoming information broadly supports the Committee's expectation of ongoing improvement in labor market conditions and inflation moving back toward its longer-run objective, the Committee will likely reduce the pace of asset purchases in further measured steps at future meetings. However, asset purchases are not on a preset course, and the Committee's decisions about their pace will remain contingent on the Committee's outlook for the labor market and inflation as well as its assessment of the likely efficacy and costs of such purchases.

To support continued progress toward maximum employment and price stability, the Committee today reaffirmed its view that a highly accommodative stance of monetary policy remains appropriate. In determining how long to maintain the current 0 to 1/4 percent target range for the federal funds rate, the Committee will assess progress--both realized and expected--toward its objectives of maximum employment and 2 percent inflation. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial developments. The Committee continues to anticipate, based on its assessment of these factors, that it likely will be appropriate to maintain the current target range for the federal funds rate for a considerable time after the asset purchase program ends, especially if projected inflation continues to run below the Committee's 2 percent longer-run goal, and provided that longer-term inflation expectations remain well anchored.

When the Committee decides to begin to remove policy accommodation, it will take a balanced approach consistent with its longer-run goals of maximum employment and inflation of 2 percent. The Committee currently anticipates that, even after employment and inflation are near mandate-consistent levels, economic conditions may, for some time, warrant keeping the target federal funds rate below levels the Committee views as normal in the longer run.

Voting for the FOMC monetary policy action were: Janet L. Yellen, Chair; William C. Dudley, Vice Chairman; Richard W. Fisher; Narayana Kocherlakota; Sandra Pianalto; Charles I. Plosser; Jerome H. Powell; Jeremy C. Stein; and Daniel K. Tarullo.

FOMC Statement Changes

·

Apr

30: Information

received since the Federal Open Market Committee met in March indicates that

growth in economic activity has picked up recently, after having slowed sharply

during the winter in part because of adverse weather conditions... Mar

19: Information received since the Federal Open Market Committee met

in January indicates that growth in economic activity slowed during the winter

months, in part reflecting adverse weather conditions.

·

Apr

30: Labor market

indicators were mixed but on balance showed further improvement. The

unemployment rate, however, remains elevated.... Mar 19: Same.

·

Apr

30: Household spending

appears to be rising more quickly... Mar 19: Household

spending and business fixed investment continued to advance.

·

Apr

30: Business fixed

investment edged down... Mar 19: See above.

·

Apr

30: Inflation

has been running below the Committee's longer-run objective, but longer-term

inflation expectations have remained stable... Mar 19: Same.

·

Apr

30: The Committee expects

that, with appropriate policy accommodation, economic activity will expand at a

moderate pace and labor market conditions will continue to improve gradually,

moving toward those the Committee judges consistent with its dual mandate... Mar

19: Same.

·

Apr

30: The Committee sees

the risks to the outlook for the economy and the labor market as nearly

balanced... Mar 19: The Same.

·

Apr

30: $10 bln taper

here, all else the same.

·

Paragraphs

4-6 the same.

·

Dissenters- Korchelakota back in the fold as there is

no dissents.

Currencies

Dollar Holds Near Lows as Fed

Tapers: 10-yr: +08/32..2.662%..USD/JPY: 102.21..EUR/USD: 1.3870

·

The Dollar Index hovers

on session lows near 79.50 as trade has seen little reaction to the Fed

announcing another $10 bln taper to its asset purchase program. Click here to see a daily Dollar

Index chart.

·

Today's

taper drops the Fed's monthly purchases to $45 bln combined of Treasury

securities and MBS.

·

EURUSD is +50 pips @ 1.3860 as action holds just off

its best levels of the morning. The single currency saw some early selling

following the cooler than anticipated eurozone Flash CPI Estimate,

but has managed to reverse those losses as trade regained the 1.3800 support

level. Today;s action has the single currency on track to close at its best

level in nearly three weeks. Banks across the eurozone are closed

tomorrow in observance of Labor Day.

·

GBPUSD is +45 pips @ 1.6870 as trade busts out to its

best levels since August 2009. Sterling briefly probed the 1.6900 level in

early U.S. trade, and is now looking at a test of the 100 mma (1.6976). British

data includes Nationwide Home Price Index, Manufacturing PMI, and net lending

to individuals.

·

USDCHF is -35 pips @ .8800 as trade has reversed all of

yesterday's gains. Minor support in the .8750 area is all that prevents a

retest of the March lows. Swiss banks are shuttered tomorrow for Labor

Day.

·

USDJPY is -45 pips @ 102.20 as trade flushes back below

the 50 dma. The pair was offered in overnight action after the Bank of

Japan held policy unchanged and suggested its 2% inflation target is likely to

be reached in about two years. A push through 102.00 sets up a test of

the bottom of the range near 101.00/101.50.

·

AUDUSD is +10 pips @ .9275 as trade drifts aimlessly

amid a lackluster trade. Support in the .9250 area remains under close watch.

Australian data is limited to import prices. China's Manufacturing PMI is due

out tomorrow. Chinese banks are closed tomorrow for Labor Day.

·

USDCAD is flat @ 1.0945. The pair has seen little

response to the in-line Canadian GDP (0.2% MoM) and cooler

than anticipated Raw Materials Price Index (0.6% MoM actual v. 1.2% MoM

expected).

Jason's Commentaries

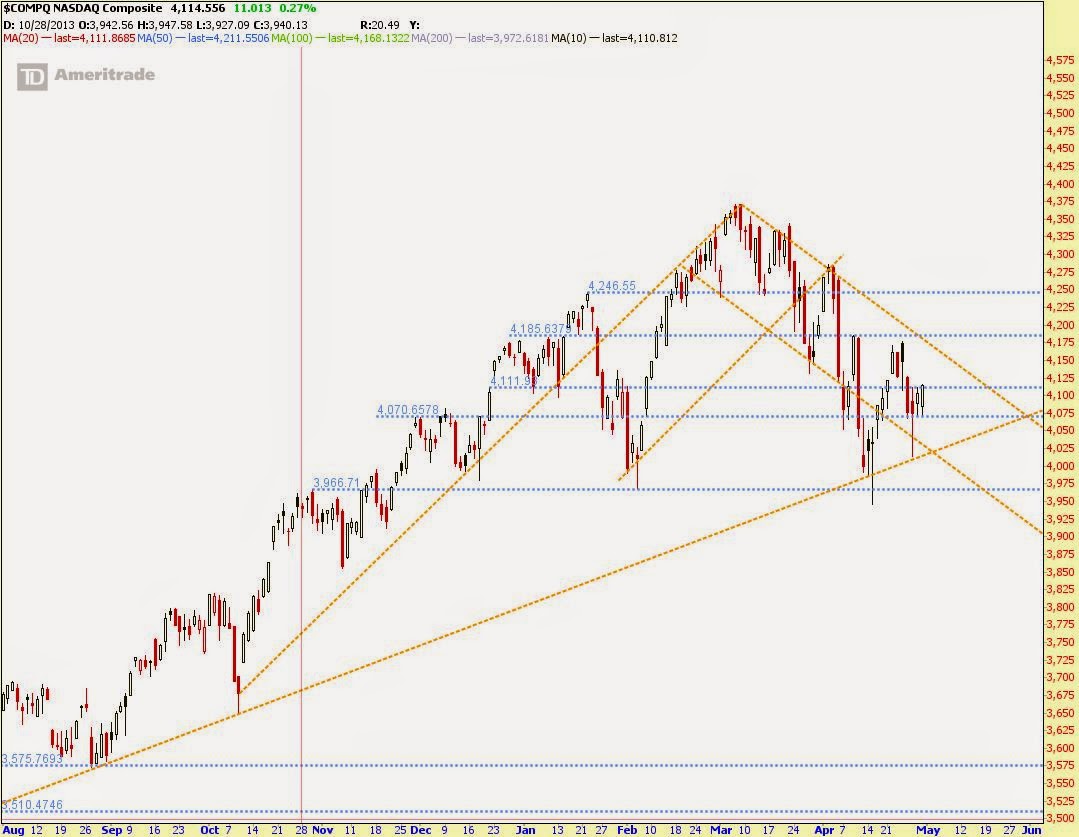

The market was generally flat to the upside before the FOMC statements as ADP employment report came in much better than expected while the Advance GDP came in much worse. This caused the market having wild gyrations before the FOMC statements. However, when the statement came out as expected, Fed continues to taper with another $10b, cutting asset purchase program from $55b to $45b. The market, as usual, gyrated violently, which ended the day in green.The broader market remains flat, with the energy companies lagging. The drag was being off set by companies like Oracle, Mastercard and some biotech companies. Volumes were at 908m shares traded on the NYSE. A exceptionally high volume on a FOMC day. That ended April in the green. And today, we're heading towards May. Dow is at it's resistance of 16600 while the S&P500 is also at its resistance. I reckon the market is going to take a step back and wait for the employment report on Friday. Also to note that Yellen will be speaking today at 830am ET. Hope she don't gyrate the market too much.

Market Call: DOWN

Date: 1 May 2014

No comments:

Post a Comment