28 Oct 2013 AMC- Market stayed flat ahead of FOMC minutes

Market Summary

Before Market Opens

S&P futures vs fair value:

-1.00. Nasdaq futures vs fair value: flat.

The S&P 500 futures hold a modest loss of 0.1%.

Asian markets finished the subdued Monday session on a generally higher note, paced by Japan's Nikkei (+2.2%) while India's Sensex (-0.6%) sat out the advance. In China, there hasn't been much let up in the Shanghai Interbank Offered Rates as the two-week rate climbed over 53 basis points to nearly 6.40%. Meanwhile, shorter-term rates were little changed. Economic data was limited to South Korea's consumer confidence, which improved to 106 from 102 (103 expected).

The S&P 500 futures hold a modest loss of 0.1%.

Asian markets finished the subdued Monday session on a generally higher note, paced by Japan's Nikkei (+2.2%) while India's Sensex (-0.6%) sat out the advance. In China, there hasn't been much let up in the Shanghai Interbank Offered Rates as the two-week rate climbed over 53 basis points to nearly 6.40%. Meanwhile, shorter-term rates were little changed. Economic data was limited to South Korea's consumer confidence, which improved to 106 from 102 (103 expected).

·

In

Japan, the Nikkei closed

higher by 2.2% as exporters and technology names displayed strength. Konami and

Mitsubishi Motors gained 3.8% and 4.2%, respectively. Yahoo Japan lost 2.2%

after cutting its profit estimates.

·

In

Hong Kong, the Hang Seng added

0.5% as consumer and energy names paced the advance. Want Want China gained

2.9% and CNOOC advanced 1.3%. Casino and gaming names lagged as Galaxy

Entertainment and Sands China both lost near 3.0% apiece.

·

In

China, the Shanghai Composite

settled little changed following a choppy session. Industrial names

outperformed as Aerospace Communications Holding and YUD Yangtze River

Investment jumped close to 6.0% each. Financials lagged with Industrial &

Commercial Bank of China down 0.5%.

Major European indices trade lower

with Spain's IBEX (-1.0%) pacing the decline. The European session has been

suffering from below-average volumes with many British traders away due to a

severe storm going through the region. According to Italian press, the

center-right PDL party may split after Silvio Berlusconi re-launched Forza

Italia. Investors received just one economic data point as Great Britain's CBI

Distributive Trades Survey tumbled to 2 from 34 (33 expected).

·

Great

Britain's FTSE is lower by 0.2% as

discretionary shares lag. EasyJet, GKN, and InterContinental Hotels Group are

all down between 1.7% and 2.7%. Aggreko outperforms with a gain of 5.0% after

the company said it expects 2013 results in-line with prior estimates.

·

In

Germany, the DAX is off 0.2% as

exporters lag. BMW, Daimler, and Volkswagen are all down between 1.3% and

2.1%.

·

France's CAC trades down 0.8%. Financials lag with Credit

Agricole and Societe Generale both down near 2.0%. Telecom provider Orange

outperforms with a gain of 0.4%.

·

Italy's MIB holds a loss of 0.7% and Spain's IBEX

is down 1.0% as banks weigh on both indices.

Market Internals

Market Internals -Technical-

The S&P 500 closed up 2 (+0.13%) at 1762, the Dow closed down 1 (-0.01%) at 15569, and the Nasdaq closed down 3 (-0.08%) at 3940. Action came on slightly above average volume (NYSE 732 mln vs. avg. of 708; NASDAQ 1727 mln vs. avg. of 1648), with decliners outpacing advancers (NYSE 1391/1658, NASDAQ 1254/1299) and new highs outpacing new lows (NYSE 186/10, NASDAQ 177/18).

Relative Strength:

Gasoline-UGA +1.54%, Mexico-EWW +1.48%, Heating Oil-UHN +1.46%, Consumer Staples-XLP +1.31%, Platinum-PPLT +1.05%, Latin America 40-ILF +1.05%, U.S. Consumer Goods-IYK +0.97%, Middle East and Africa-GAF +0.75%, South Korea-EWY +0.70%, South Africa-EZA +0.70%.

Relative Weakness:

Natural Gas-UNG -3.91%, Clean Energy-PBW -2.12%, Grains-JJG -2.05%, Egypt-EGPT -1.85%, Corn-CORN -1.63%, Social Media-SOCL -1.5%, Vietnam-VNM -1.35%, India-INP -1.08%, Spain-EWP -0.92%, Greece-GREK -0.87%.

Leaders and Laggards

Technical Updates

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Briefing's Commentaries

Closing Market Summary: Stocks End

Little Changed

The S&P 500 punctuated an uneventful session with a modest gain, adding 0.1% to extend its October advance to 4.8%.

Stocks alternated between gains and losses through the first two hours of action before the S&P climbed to a fresh record high of 1764.99. Final-hour selling cut the S&P's gain in half, but the index still finished ahead of the Dow (unch) and the tech-heavy Nasdaq (-0.1%), which was challenged by its flat line throughout the session.

Although the third-quarter earnings season is far from being over, today featured just a handful of notable reports. Health care components caught the eye of some participants with Biogen (BIIB 254.43, +2.17) reporting solid results and Merck (MRK 45.35, -1.19) beating bottom-line estimates on below-consensus revenue. Although Merck weighed, the broader health care sector (+0.3%) drew strength from the 6.7% gain in Bristol-Myers Squibb (BMY 52.02, +3.25) after the company announced positive clinical trial data.

Generally speaking, countercyclical sectors followed in health care's lead as consumer staples (+1.2%) and telecom services (+0.4%) outperformed while utilities (-0.2%) lagged.

Meanwhile, cyclical groups were a bit more mixed. Energy (+0.1%) and technology (+0.3%) finished in positive territory while consumer discretionary (-0.2%), financials (-0.2%), industrials (-0.1%), and materials (-0.6%) trailed the S&P.

The technology sector ended among the leaders with its top component, Apple (AAPL 529.88, +3.92), adding 0.7% ahead of its after-hours earnings report. However, the Nasdaq could not build on the relative strength of the sector as momentum names like Facebook (FB 50.23, -1.72), Priceline.com(PCLN 1060.15, -10.70), and Netflix (NFLX 314.00, -14.03) weighed.

Also of note, the industrial space was little changed as defense contractors and transports headed in opposite directions. The PHLX Defense Index shed 0.3% as the second largest component, Boeing (BA 129.88, -1.31), fell 1.0%. On the upside, the Dow Jones Transportation Average rose 0.4% as 12 of 20 members advanced.

Treasuries held inside narrow ranges throughout the session, and the 10-yr yield ended at 2.52%.

Trading volume was in-line with average as just over 730 million shares changed hands on the floor of the New York Stock Exchange.

Today's economic data was limited to September industrial production and pending home sales.

Industrial production increased 0.6% after rising 0.4% in August (Briefing.com consensus +0.3%). That was the largest monthly increase since February.

The headline number is undoubtedly striking for its perceived strength. However, that thought process is actually a misnomer. Rather than coming from manufacturing growth, almost the entire gain came from a 4.4% increase in utilities production. After five consecutive months of declines from cooler-than-normal temperatures, utility production returned to more normal levels as weather conditions reverted to their averages.

Manufacturing growth, which is key for economic growth, increased a very modest 0.1% in September, down from a 0.5% gain in August.

Separately, pending home sales for September tumbled 5.6%, which was worse than the 1.3% decrease forecast by the Briefing.com consensus. Today's reading followed last month's decrease of 1.6%.

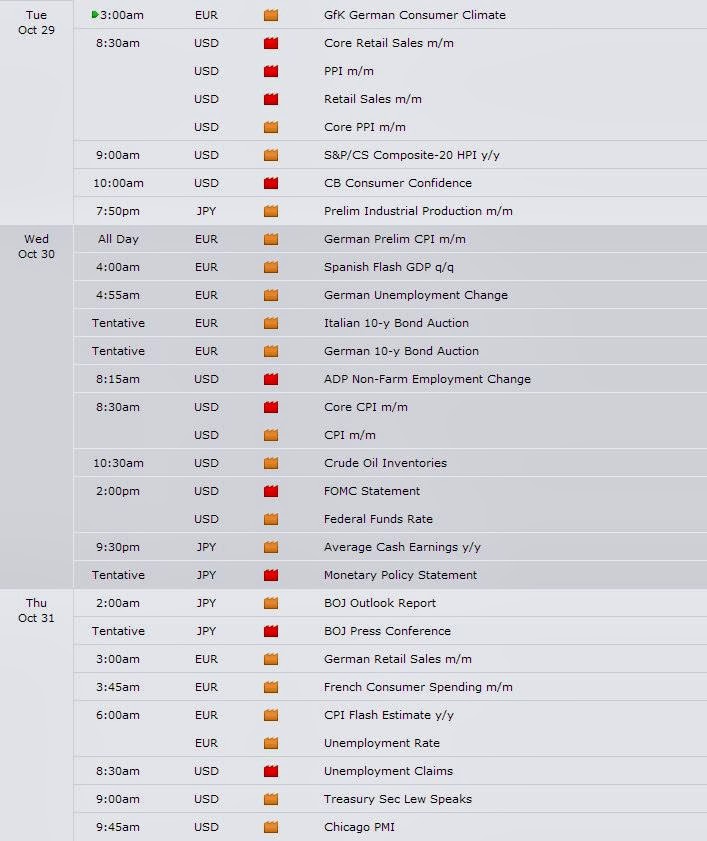

Tomorrow, September retail sales and Producer Price Index will be reported at 8:30 ET, August Case-Shiller 20-City Index will cross the wires at 9:00 ET, and August business inventories will be announced at 10:00 ET. Also at 10:00 ET, the October Consumer Confidence report will be released.

The S&P 500 punctuated an uneventful session with a modest gain, adding 0.1% to extend its October advance to 4.8%.

Stocks alternated between gains and losses through the first two hours of action before the S&P climbed to a fresh record high of 1764.99. Final-hour selling cut the S&P's gain in half, but the index still finished ahead of the Dow (unch) and the tech-heavy Nasdaq (-0.1%), which was challenged by its flat line throughout the session.

Although the third-quarter earnings season is far from being over, today featured just a handful of notable reports. Health care components caught the eye of some participants with Biogen (BIIB 254.43, +2.17) reporting solid results and Merck (MRK 45.35, -1.19) beating bottom-line estimates on below-consensus revenue. Although Merck weighed, the broader health care sector (+0.3%) drew strength from the 6.7% gain in Bristol-Myers Squibb (BMY 52.02, +3.25) after the company announced positive clinical trial data.

Generally speaking, countercyclical sectors followed in health care's lead as consumer staples (+1.2%) and telecom services (+0.4%) outperformed while utilities (-0.2%) lagged.

Meanwhile, cyclical groups were a bit more mixed. Energy (+0.1%) and technology (+0.3%) finished in positive territory while consumer discretionary (-0.2%), financials (-0.2%), industrials (-0.1%), and materials (-0.6%) trailed the S&P.

The technology sector ended among the leaders with its top component, Apple (AAPL 529.88, +3.92), adding 0.7% ahead of its after-hours earnings report. However, the Nasdaq could not build on the relative strength of the sector as momentum names like Facebook (FB 50.23, -1.72), Priceline.com(PCLN 1060.15, -10.70), and Netflix (NFLX 314.00, -14.03) weighed.

Also of note, the industrial space was little changed as defense contractors and transports headed in opposite directions. The PHLX Defense Index shed 0.3% as the second largest component, Boeing (BA 129.88, -1.31), fell 1.0%. On the upside, the Dow Jones Transportation Average rose 0.4% as 12 of 20 members advanced.

Treasuries held inside narrow ranges throughout the session, and the 10-yr yield ended at 2.52%.

Trading volume was in-line with average as just over 730 million shares changed hands on the floor of the New York Stock Exchange.

Today's economic data was limited to September industrial production and pending home sales.

Industrial production increased 0.6% after rising 0.4% in August (Briefing.com consensus +0.3%). That was the largest monthly increase since February.

The headline number is undoubtedly striking for its perceived strength. However, that thought process is actually a misnomer. Rather than coming from manufacturing growth, almost the entire gain came from a 4.4% increase in utilities production. After five consecutive months of declines from cooler-than-normal temperatures, utility production returned to more normal levels as weather conditions reverted to their averages.

Manufacturing growth, which is key for economic growth, increased a very modest 0.1% in September, down from a 0.5% gain in August.

Separately, pending home sales for September tumbled 5.6%, which was worse than the 1.3% decrease forecast by the Briefing.com consensus. Today's reading followed last month's decrease of 1.6%.

Tomorrow, September retail sales and Producer Price Index will be reported at 8:30 ET, August Case-Shiller 20-City Index will cross the wires at 9:00 ET, and August business inventories will be announced at 10:00 ET. Also at 10:00 ET, the October Consumer Confidence report will be released.

·

Russell 2000 +31.6%

YTD

·

Nasdaq +30.5% YTD

·

S&P 500 +23.6%

YTD

·

DJIA +18.8% YTD

Commodities

Closing Commodities: Crude Oil Hits

New HoD In Electronic Trade

·

Commodities are mostly

lower/mixed by the end of today's trading sessionIn metals, there wasn't much

of a change in price as Dec copper ended the day flat at $3.27/lb, Dec gold

lost $0.50 to $1351.90/oz and Dec silver fell $0.21 to $22.52

·

Crude oil rallied right

at the open of pit trading from just under the $97.50/barrel level

·

In electronic trade

here, crude oil extended gains and rose to a new HoD of $98.75/barrel

·

During crude's floor

trading session, it rose $0.84 and finished the day at $98.69/barrel

·

Natural gas was weak all

day and basically continued to extend losses slowly throughout the day

NYMEX

Energy Closing Prices

·

Dec crude oil rose $0.84

to $98.69/barrel

·

Nov natural gas fell 12

cents to $3.59/MMBtu

·

Dec heating oil rose 5

cent to $2.96/gallon

·

Dec RBOB gasoline rose 5

cent to $2.61/gallon

CBOT

Agriculture and Ethanol/ICE Sugar Closing Prices

·

Dec corn fell 10 cents

to $4.30/bushel

·

Dec wheat fell 10 cents

to $6.81/bushel

·

Nov soybeans fell 29

cents to $12.71/bushel

·

Dec ethanol settled

$0.02 lower at $1.68/gallon

·

Jan sugar (#16 (U.S.))

fell 0.10 of a penny to 22.08 cents/lbs

COMEX

Metals Closing Prices

·

Dec gold fell $0.50 to

$1351.90/ounce

·

Dec silver fell $0.12 to

$22.52/ounce

·

Dec copper remain

unchanged at $3.27/lbs

{kind=link}

Treasuries

Treasuries Slip Amid Lackluster

Trade: 10-yr: -01/32..2.515%..USD/JPY: 97.63..EUR/USD: 1.3805

·

Treasuries spent the

entire session hugging their respective flat lines as mixed economic data and a

solid $32 bln 2y note auction had little impact.

·

Today's

economic data was mixed as

industrial production (0.6% actual v. 0.3% expected) and capacity utilization

(78.3% actual v. 78.0% expected) topped estimates while pending home sales

(-5.6% actual v. -1.3% expected) missed.

·

This afternoon's solid

$32 bln 2y note auction drew 0.323% (0.328% when issued) and a 3.32x

bid/cover (12-auction average 3.43x). Both indirect (29.0%) and direct (30.9%)

bidders saw stronger than usual takedowns, leaving primary dealers with just

40.1% of the supply.

·

Light selling caused yields

to tack on as much as 1bp apiece. Click here to see an intraday

yields chart.

·

The

10y was locked in a 2bp range (2.500%-2.520%) throughout the session before

ending +1bp @ 2.512%. Participants

continue to watch the 2.450% area as support there dates back to the

summer.

·

A

steeper curve persisted as the spread between 2s and 10s widened to 220bps.

·

Precious metals saw a mixed

trade with gold +$2 @ $1354 and silver -$0.10 @ 22.55.

·

Tuesday's

Data: Retail sales, retail

sales ex-auto, PPI, Core PPI (8:30), Case-Shiller 20-city Index (9), business

inventories, and consumer confidence (10).

·

Treasury will

auction $35 bln 5y notes.

{kind=link}

Next Day In View

Economic Commentary

Economic Summary: Pending Home sales

fall more than expected; IP tops expectations; Retail Sales & PPI tomorrow

at 8:30; Fed decision Wednesday at 14:00

Economic Data Summary:

Economic Data Summary:

·

September

Industrial Production 0.6% vs Briefing.com consensus of 0.3%; August was 0.4%

o After five consecutive months of declines from

cooler-than-normal temperatures, utility production returned to more normal

levels as weather conditions reverted to their averages. Manufacturing growth,

which is key for economic growth, increased a very modest 0.1% in September,

down from a 0.5% gain in August. The ISM Production Index fell in September,

suggesting that manufacturing production growth would soften in the September

report. However, it remained over 60 for a third consecutive month and signaled

elevated production levels.

·

September Capacity

Utilization 78.3% vs Briefing.com consensus of 78.0%; August was revised to

77.9% from 77.8%

·

September

Pending Home Sales -5.6% vs Briefing.com consensus of -1.3%; August was -1.6%

Upcoming Economic Data:

·

September

Retail Sales due out Tuesday at 8:30 (Briefing.com consensus of -0.1%; August

was 0.2%)

·

September

Retail Sales Ex-Auto due out Tuesday at 8:30 (Briefing.com consensus of 0.2%;

August was 0.1%)

·

September

PPI due out Tuesday at 8:30 (Briefing.com consensus of 0.2%; August was 0.3%)

·

September

Core PPI due out Tuesday at 8:30 (Briefing.com consensus of 0.1%; August was

0.0%)

·

August Case Schiller 20

City Index due out Tuesday at 9:00 (Briefing.com consensus of 12.4%; July was

12.0%)

·

August Business

Inventories due out Tuesday at 10:00 (Briefing.com consensus of 0.2%; July was

0.4%)

Upcoming Fed/Treasury Events:

·

The Treasury is

expected to auction off $96 bln in new debt next week. The results of each

auction will be announced at 13:0

o Monday: $32 bln in 2 year notes

o Tuesday: $35 bln in 5 year notes

o Wednesday: $29 bln in 7 year notes

·

The

Federal Reserve will begin a two day meeting on Tuesday. The policy

announcement will be made Wednesday at 14:00 (no press conference or econ

projections).

Other International Events of

Interest

·

There hasn't been much

let up in the Chinese Shanghai Interbank Offered Rates as the two-week rate

climbed over 53 basis points to nearly 6.40%.

On other news....

Currencies

Dollar Holds Small Gains: 10-yr:

unch..2.510%..USD/JPY: 97.67..EUR/USD: 1.3799

The Dollar Index continues to hold small gains amid a rather uneventful session. Action has been trapped near 79.30 for almost the entire U.S. session as trade climbs off nine-month lows. Click here to see a daily Dollar Index chart.

The Dollar Index continues to hold small gains amid a rather uneventful session. Action has been trapped near 79.30 for almost the entire U.S. session as trade climbs off nine-month lows. Click here to see a daily Dollar Index chart.

·

EURUSD is -15 pips at 1.3790 as a sleepy trade has

limited action to just a 40 pip range. A lack of data and news out of the

eurozone has lead to the lackluster session as traders err on the side of

caution ahead of Wednesday's FOMC rate decision.

·

GBPUSD is -20 pips at 1.6145 as trade presses the lower

end of the 1.6150/1.6250 range that has been in play for much of the past two

weeks. Sterling slipped off its best levels of the session after CBI Realized

Sales posted a sharp decline, but the losses have been limited to the bulls

defend support at the level. British data is limited to net lending to

individuals.

·

USDCHF is +30 pips at .8950 as trade ticks off

23-month lows. Bulls will look to retake the .9000 area over the coming

sessions.

·

USDJPY is +25 pips at 97.65 as action continues to hold

modest gains. Many traders have looked for opportunity elsewhere as the

97.00/99.00 range that has been in place over the past month remains intact. Japanese

data includes household spending and retail sales.

·

AUDUSD is -10 pips at .9570 as trade pushes lower for

the third time in four days. The recent weakness in the hard currency

corresponds with a spike in China's SHIBOR, which has created some liquidity

concerns in the Middle Kingdom. The .9500 area is home to some decent

support. Reserve Bank of Australia Governor Glenn Stevens will speak tonight in

Sydney.

·

USDCAD is -5 pips at 1.0445 as a sleepy trade nears

the finish line. Action during U.S. trade has held in a tight 10 pip range.

Canada's Raw Materials Price Index will cross tomorrow.

Jason's Commentaries

As expected, market stayed flat till the closing bell. Though there are quite some volatility throughout the day, there's really nothing much driving the market anywhere. However, the S&P500 broke another high once again at 1765, but failed to sustain the high and lost the most of its gains. Volumes were rather healthy and internals were all showing flat signs. We're having Apple announcing its earnings AMC and it seems that Apple did pretty for its earnings. That could be the market mover today. If Apple fails to move the market, we're likely to end up with another flat day today... Probably to the downside.

Market Call: FLAT to downside

Date: 29 Oct 2013

No comments:

Post a Comment