3 Oct 2013 AMC- Obama do not want to negotiate over debt ceiling?

Market Summary

European

Markets Closing Prices

European

markets are now closed; stock markets across Europe performed as follows:

·

UK's FTSE: + 0.2%

·

Germany's DAX: -0.4%

·

France's CAC: -0.7%

·

Spain's IBEX: -0.6%

·

Portugal's PSI: -0.7%

·

Italy's MIB Index: -0.4%

·

Irish Ovrl Index: -0.2%

·

Greece ATHEX Composite: + 2.1%

Before Market Opens

S&P futures vs fair value:

-4.60. Nasdaq futures vs fair value: -4.50.

The S&P 500 futures trade about five points below fair value.

Markets across most of Asia booked gains as only Japan's Nikkei (-0.1%) and Singapore's Straits Times (-0.3%) ended in the red. The region was boosted by the improvement in China's Non-Manufacturing PMI (55.4 actual versus 53.9 previous), which helped propel Hong Kong's Hang Seng, India's Sensex, and Taiwan's Taiex to gains of at least 1%. Markets on mainland China remained closed for Golden Week while South Korea's Kospi was shuttered for National Foundation Day of Korea. Data from the rest of the region was limited as Hong Kong's retail sales 7.2% year-over-year and Thai consumer confidence slipped to 77.9 (79.3 previous).

The S&P 500 futures trade about five points below fair value.

Markets across most of Asia booked gains as only Japan's Nikkei (-0.1%) and Singapore's Straits Times (-0.3%) ended in the red. The region was boosted by the improvement in China's Non-Manufacturing PMI (55.4 actual versus 53.9 previous), which helped propel Hong Kong's Hang Seng, India's Sensex, and Taiwan's Taiex to gains of at least 1%. Markets on mainland China remained closed for Golden Week while South Korea's Kospi was shuttered for National Foundation Day of Korea. Data from the rest of the region was limited as Hong Kong's retail sales 7.2% year-over-year and Thai consumer confidence slipped to 77.9 (79.3 previous).

·

Japan's Nikkei shed 0.1% amid a quiet trade. Heavyweight

Softbank added 4.0%, finishing at its best level in more than 13 years while

becoming the second heaviest weighted name in the Nikkei. Elsewhere, shares of

Tokyo Electric Power fell 4.8% after a new leak was discovered at its Fukushima

Daiichi plant.

·

In

Hong Kong, the Hang Seng finished

higher by 1.0% as shares were boosted by the Chinese Non-Manufacturing PMI

data. Commodity-related names posted solid gains as gold miner Zhaojin Mining

rose 1.6% and oil explorer Cnooc tacked on 2.2%. Meanwhile, casino shares were

bolstered by solid September revenues with Sands China adding 3.9%.

·

In

China, the Shanghai Composite

was closed.

Major European indices trade in

mixed fashion but their moves have been limited to less than 0.5% in either

direction. In news of note, European Central Bank President Mario Draghi said

he has asked an ECB panel to look into ways of improving bank liquidity.

However no target date has been set for introducing a new plan. Participants received

a fair share of data as Eurozone retail sales rose 0.7% month-over-month (0.2%

expected, 0.5% prior) and the Services PMI ticked up to 52.2 from 52.1 (52.1

forecast). Germany's Services PMI slipped to 53.7 from 54.4 (54.4 expected).

Great Britain's Services PMI ticked down to 60.3 from 60.5 (60.0 forecast).

Separately, the Halifax House Price Index rose 0.3% month-over-month (0.5%

expected, 0.3% prior) while the year-over-year reading increased 6.2% (6.4%

consensus, 5.4% last). French Services PMI rose to 51.0 from 50.7 (50.7

expected). Italy's Services PMI climbed to 52.7 from 48.8 (49.1 forecast).

Elsewhere, Spain's Services PMI fell to 49.0 from 50.4 (51.0 consensus).

·

In

France, the CAC is lower by

0.3% as industrials weigh. Alstom and Schneider Electric hold respective losses

of 3.9% and 2.5%. Oil explorer Technip is the top index performer with a gain

of 1.7%.

·

Germany's DAX trades flat amid a choppy trade. Chemical

producers K+S and Linde lead with gains close to 1.2% apiece. Meanwhile,

financials lag with Allianz and Commerzbank down 0.4% and 1.9%,

respectively.

·

Great

Britain's FTSE trades higher by

0.3% as insurers outperform. Aviva is higher by 1.9% and RSA Insurance Group

sports a gain of 1.1%. Miners trade mostly lower with Fresnillo and Randgold

Resources both down near 2.0%.

Market Internals

Market Internals -Technical-

The Nasdaq closed down 41 (-1.07%) at 3774, the Dow closed down 137 (-0.90%) at 14996, and the S&P 500 closed down 15 (-0.90%) at 1679. Action came on above average volume (NYSE 703 mln vs. avg. of 697; NASDAQ 1794 mln vs. avg. of 1591), with decliners outpacing advancers (NYSE 654/2418, NASDAQ 658/1857) and new highs outpacing new lows (NYSE 98/43, NASDAQ 123/22).

Relative Strength:

Volatility-VXX +3.69%, Taiwan-EWT +1.77%, India-INP +0.98%, Greece-GREK +0.97%, Cotton-BAL +0.73%, Coffee-JO +0.73%, Indian Rupee-ICN +0.57%, Grains-JJG +0.46%, Sugar-SGG +0.41%, Poland-EPOL +0.41%.

Relative Weakness:

Indonesia-IDX -2.47%, Cocoa-NIB -2.19%, Social Media-SOCL -2.04%, Mexico-EWW -1.92%, Copper Miners-COPX -1.88%, Cloud Computing-SKYY -1.87%, Internet Composite-FDN -1.86%, Israel-EIS -1.25%, Latin America 40-ILF -1.15%, Turkey-TUR -1.08%.

Leaders and Laggards

Technical Updates

{kind=link}

{kind=link}

{kind=link}

Briefing's Commentaries

Closing Market Summary: Stocks Slump as Budget Stalemate Continues

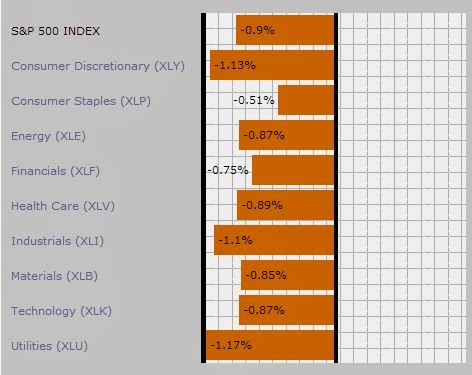

The S&P 500 fell 0.9% as the government shutdown continued for the third day without any strong indications a resolution to the stalemate may be on the horizon.

Even though stocks appeared largely unconcerned during the first two days of the shutdown, today's session featured a reminder from the Treasury, saying the consequences of a default could be worse than the events of 2008.

Equities retreated throughout the morning before finding support in the early afternoon following an article in The New York Times indicating Speaker of the House John Boehner told Republicans he would not allow a default to take place. The story was followed by a statement from the Speaker's office, which said this has always been Mr. Boehner's stance.

Thanks to the rebound, the S&P was able to erase a third of its losses, but could not close above its 50-day moving average (1680). The index endured an afternoon slip in reaction to shots fired near the U.S. Capitol. The scare caused a 30-minute lockdown of the Capitol building, and the suspect was reported dead on the scene.

All ten sectors ended in the red with influential groups like consumer discretionary (-1.0%), industrials (-1.1%), and technology (-1.0%) leading to the downside.

Notably, industrials finished near the bottom of the leaderboard for the second consecutive day. Like yesterday, defense contractors weighed on the sector as the PHLX Defense Index fell 1.0%.The largest index component, General Electric (GE 24.10, -0.23), also lost 1.0%.

The Dow Jones Transportation Average also underperformed, slumping 1.1%, even as airlines displayed relative strength. United Continental (UAL 31.65, +0.72) settled higher by 2.3%.

Elsewhere, the technology sector saw its top components, Apple (AAPL 483.41, -6.15), Google (GOOG 876.09, -11.90), and Qualcomm (QCOM 67.11, -0.57), lose between 0.8% and 1.4% while chipmakers outperformed. The PHLX Semiconductor Index shed 0.3%.

Countercyclical groups ended mixed as consumer staples (-0.5%) and telecom services (-0.4%) finished ahead of the S&P while health care (-1.0%) and utilities (-1.2%) lagged.

Treasuries registered modest gains, and the benchmark 10-yr yield slipped two basis points to 2.61%.

Today's trading volume was a bit below average as 703 million shares changed hands on the floor of the NYSE.

The weekly initial claims level increased to 308,000 from an upwardly revised 307,000 (from 305,000) while the Briefing.com consensus expected a rise to 315,000. After a couple weeks of unreliable claims data, the initial claims level has settled at a little over 300,000. This marks a vast improvement from August when claims were around 330,000.

Normally, this level of claims would suggest a strong gain in nonfarm payrolls. However, over the last couple of months, the strengthening in the claims level had no effect on payroll growth. Employers appear to be content with their workforce; hence, we have seen the drop in layoffs, but not a corresponding spike in hiring activity.

Separately, the September ISM Non-Manufacturing Index fell to 54.4 from 58.6 while the Briefing.com consensus expected the index to drop to 57.2. Last month's reading of the ISM Non-Manufacturing Index was the highest since December 2005 and was expected to pullback in September. The size of the pullback; however, was very unusual.

The non-manufacturing index normally lacks significant monthly volatility and moves in a nice smooth trend. September marked a departure as the index dropped by an unusually large 4.2 points. That was the biggest decline since November 2008. The index has moved at least 4.2 points in a single month only nine times since its inception in 1997.

Tomorrow's September nonfarm payrolls report will not be released due to the ongoing government shutdown.

Commodities

Closing Commodities: Crude Oil Drops In Final Few Minutes Of Pit Trade

Commodities ended the day mostly lower.

Crude oil futures sold off in the last few minutes of pit trading, pulling it below $103/barrel. At the end of today's session, Nov crude oil lost $0.79/barrel to $103.29/barrel.

Nov natural gas futures declined four cents to $3.50/MMBtu.

Precious metals recovered most of its losses today, but copper ends near session low. Dec gold ended the day $3.60 lower at $1317.10/oz, Dec silver closed $0.15 at $21.77/oz. Dec copper fell five cents to $3.27/lb.

COMEX

Metals Closing Prices

·

Dec gold fell $3.6 to

$1317.10/ounce

·

Dec silver fell $0.15 to

$21.77/ounce

·

Dec copper fell 5 cents

to $3.27/lbs

NYMEX

Energy Closing Prices

·

Nov crude oil fell $0.79

to $103.29/barrel

·

Nov natural gas fell 4

cents to $3.50/MMBtu

·

Nov heating oil rose 1

cent to $3.00/gallon

·

Nov RBOB gasoline

remained unchanged at $2.63/gallon

CBOT

Agriculture and Ethanol/ICE Sugar Closing Prices

·

Dec corn settled

unchanged at $4.39/bushel

·

Dec wheat rose 3 cents

to $6.89/bushel

·

Nov soybeans rose 12

cents to $12.86/bushel

·

Nov ethanol rose 4 cents

to $1.67/gallon

·

Nov sugar (#16 (U.S.))

rose 0.31 of a penny to 21.52 cents/lbs

{kind=link}

Treasuries

Treasuries Climb to Two-Month Highs: 10-yr: +02/32..2.611%..USD/JPY: 97.25..EUR/USD: 1.3620

Treasuries finished with small gains as continued banter over the budget/debt ceiling debates stoked a safety bid. Today's advance was sparked by this morning's disappointing ISM Services report (54.4 actual v. 57.2 expected), which posted its biggest drop in over four years. The buying was further exacerbated by a Treasury paper suggesting a debt ceiling default has the potential to lead to "a financial crisis and recession that could echo the events of 2008 or worse."

Treasuries rallied into the noon hour, causing both the 5- and 10-yr yields to probe respective support of 1.350% and 2.600% before selling began to surface on reports House Speaker John Boehner was steadfast in not letting the U.S. default on its debt. Light selling persisted throughout the afternoon, cutting the early gains in half. The benchmark 10-yr yield ended the day off 2 bps at 2.060% to post its lowest close in nearly two months. The 30-yr was a laggard throughout the session as its yield ended little changed at 3.707%. The very front of the curve remains on many traders' radars as another 4.5 bp spike in the 1-month yield produced a climb 0.130%. This marked the highest close since late-November. A flatter yield curve developed as a result of today's action with the 2-10-yr spread tightening to 228.5 bps. Elsewhere, precious metals lost ground as gold fell $3 to $1318 and silver slid $0.15 to near $21.75.

Nonfarm payrolls, nonfarm private payrolls, the unemployment rate, hourly earnings, and the average workweek releases will all be delayed due to the government shutdown. Dallas' Fisher remains in Little Rock to give an economic update to the Central Arkansas Risk Management Association (8:30). NY's Dudley will be in New York City, speaking on "'Fire Sales' as a Driver of Systemic Risk in the Tri-Party Repo and Other Secured Funding Markets" (9:15). Richmond's Lacker discusses "Human Capital Investment as a Major Financial Decision" in front of the Council of Economic Education (12:30). A heavy day of Fed speak concludes with Minny's Kocherlakota in Bloomington, MN speaking on "Monetary Policy Strategy" (13:45).

{kind=link}

Next Day In View

Events and conferences of interest for tomorrow

Events and conferences

of interest for tomorrow

·

BoJ Decision (out

overnight)

·

Fed's Fisher to speak at

8:30

Fed's

Dudley to speak at 9:15

Economic Commentary

Economic Summary: Jobless Claims

lower than expected; ISM services misses expectations; Williams said U.S.

unemployment is still too high and inflation is too low; NFP's to be delayed

tomorrow due to shutdown

Economic Data Summary:

Economic Data Summary:

·

September Challenger Job

Cuts +19.1% (August was 56.5%)

·

Weekly

Initial Claims 308K vs Briefing.com consensus of 315K; Last Week was revised to

307K from 305K

·

Weekly Continuing Claims

2.952 M vs Briefing.com consensus of 2.825 M ; Last Week was 2.823 M

o That is a vast improvement from August when

claims were around 330,000. Normally, this level of claims would suggest a

strong gain in nonfarm payrolls. Over the last couple of months, however, the

strengthening in the claims level had no effect on payroll growth. Employers

appear to be content with their workforce; hence, we have seen the drop in

layoffs, but not a corresponding spike in hiring activity. With the government

shutdown, there is no way of knowing if the drop in claims translated into

stronger September payroll gains. During the last government shutdown, the

initial claims level jumped by a little over 80,000 as federal workers applied

for unemployment claims.

·

August Factory Orders were

delayed due to government shutdown

·

September

ISM Services 54.4 vs Briefing.com consensus of 57.2; August was 58.6

o The size of the pullback, however, was very

unusual. The non-manufacturing index normally lacks significant monthly

volatility and moves in a nice smooth trend. In September, however, the index

dropped by an unusually large 4.2 points. That was the biggest decline since

November 2008.

Fed/Treasury Events Summary:

·

San Francisco Fed

President John Williams (not a voting FOMC member, typically moderate) said

''We are therefore in a situation where U.S. unemployment is still too high and

inflation is too low. The appropriate stance of monetary policy is

very accommodative and that will continue to be the case for quite some time. As

the U.S. economy continues to improve, it will be appropriate for the Fed to

start trimming its asset purchases and eventually stop them altogether'

·

Dallas Fed President

Richard Fisher (not a voting FOMC member this year, will have vote in 2014,

typically hawkish) said bond-purchase message has been 'garbled'; says

uncertainty around U.S. expansion; says if Congress fails to raise the debt

limit the world will never be the same.

·

Atlanta Fed President

Dennis Lockhart (not a voting FOMC member, typically moderate) said October

decision difficult if debt ceiling unresolved; gov't shut down vindicates

September decision.

Upcoming Economic Data:

·

The

Employment Situation Report will be delayed tomorrow due to government shutdown

Upcoming Fed/Treasury Events:

·

Dallas Fed President

Richard Fisher (2014 voter, hawk) to speak tomorrow at 8:30

·

NY Fed President William

Dudley (voting FOMC member, dove) to speak tomorrow at 9:15

·

Fed Governor Jeremy

Stein (voting FOMC member. dove) to speak tomorrow at 9:30

·

Atlanta Fed President

Dennis Lockhart (not a voting FOMC member, typically moderate) to speak

tomorrow at 12:30

·

Minneapolis Fed

President Narayana Kocherlakota (2014 voter, typically dovish) to speak

tomorrow at 13:45

Other International Events of

Interest

·

Eurozone retail sales

rose 0.7% month-over-month (0.2% expected, 0.5% prior) and the Services PMI

ticked up to 52.2 from 52.1 (52.1 forecast).

·

China's

Non-Manufacturing PMI rose to 55.4 from 53.9. Japan's foreign bonds buying

report indicated net purchases in the amount of JPY672.10 billion (JPY175.60

billion prior).

On other news....

Market rebounds further as headlines

cross suggesting the Capitol shooting suspect was captured

·

As mentioned earlier,

the market just dropped on headlines that shots were fired at the U.S. Capitol;

markets are now rebounding off initial knee-jerk lows... See 14:24 for initial

headlines.

·

Capitol buildings are on

lockdown

·

The S&P dropped

around 6 points, DJ dropped around 50 pts

·

Markets are rebounding

off the initial knee-jerk lows now

Gun stocks SWHC, RGR have

also rebounded off of their lows

Currencies

Jason's Commentaries

Things are getting really funky... The fear of the US gov's debt default has been aggravated by stupid and unnecessary political posturing by both the republicans and democrats. To add oil to fire, Obama mentioned last night he is not going to negotiate of the debt ceiling issue. This certainly drove some fear down our spine. To make things worse, there was shooting case outside The Capitol which took the market down, somewhat like a flash crash...

Market started with a bearish bias last night and the bearishness persisted till 12pm ET, where the market started to retrace a little. However, at 2pm ET, market suddenly tanked due to the shooting outside The Capitol. However that recovered quickly. The subsequent period of the day remained flat throughout. Volumes were decent last night at 693m shares traded on the NYSE, the bears definitely took bulls out of the window last night. Consumer discretionary, Utilities and industrials were the main laggard last night with more than 1.1% decline and it's a sea of red last night. While on the technical side, the S&P500 managed to hold on to its 1680 support level. I reckon this volatility will continue until the US gov is able to sit down manage their internal problem. This is what happens when you got 2 parties of almost equal political power in the Congress. Republicans are doing their best to get Obamacare out of the window, and the democrats is definitely painting the Republicans as the bad guys. This is going to be a very nasty fight in the Congress. Have fun and sit back and watch history in the making =D

Read more on debt ceiling here

http://money.cnn.com/2013/10/03/news/economy/debt-ceiling-default/index.html

Market Call: FLAT and volatile

Date: 4 Oct 2013

No comments:

Post a Comment