21 June 2013 AMC

Market Summary

Market Internals

Leaders and Laggards

Technical Updates

Commentaries

|

|

| Stock Market Update |

16:10 ET Dow +41.08 at 14799.4, Nasdaq -7.39 at 3357.25, S&P +4.24 at 1592.43 :[BRIEFING.COM] The major averages ended on a mixed note as the S&P 500 added 0.3% while Nasdaq shed 0.2%.

Technology stocks lagged from the opening bell with Oracle (ORCL 30.14, -3.07) contributing to the underperformance. Shares of the software company fell 9.3% in reaction to a disappointing earnings report. Other major tech components like Apple(AAPL 413.50, -3.34) and Google (GOOG 880.93, -3.81) also settled in the red. The weakness in large technology shares pressured the Nasdaq, which trailed behind the broader market throughout the day.

Equities received a midday boost off session lows after Jon Hilsenrath of The Wall Street Journal put out a piece suggesting the markets might be misreading the Fed's messages and that there were overlooked dovish signals in Chairman Bernanke's press conference. This gave the S&P some fuel for an afternoon rally.

The second-half climb stalled briefly after yet another headline made the rounds. This time, International Monetary Fund's David Lipton said the withdrawal of Federal Reserve's stimulus is a positive, but there may be a case for central banks and governments to step in if markets become disorderly.

Notably, while the Wall Street Journal story sparked a fire under equities, the Treasury market's response was limited.

Rising Treasury yields have been in focus all week with the climb continuing today. The 10-yr note began selling off prior to the start of the U.S. session and continued sliding to end on its lows. As a result, the benchmark 10-yr yield jumped almost ten basis points to 2.514%, its highest level since August 2011.

Despite the ongoing rise in yields, income-oriented sectors held up well today as telecom services and utilities ended with respective gains of 0.6% and 1.3%. The relative strength of these sectors in the face of climbing yields suggests some seller exhaustion may have taken place. Despite today's advances, the two defensive sectors ended the week with respective losses of 3.7% and 2.8%.

Also of note, the financial sector ended in line with the broader market, but major banks came under pressure after a Bloomberg story suggested U.S. regulators are kicking around the idea of doubling minimum capital requirements for the country's largest banks.Bank of America (BAC 12.70, -0.20) lost 1.5% while Citigroup (C 46.87, -1.03) settled lower by 2.2%.

The CBOE Volatility Index (VIX 18.78, -1.71) ended near its lows after yesterday's session sent it to its highest level of the year. |

|

Commodities

Treasuries

Weekly Analysis

Week 38

Technical Updates

Briefing's Commentaries

Week in Review: Federal Reserve Comments Taper Buying Interest The major averages ended Monday's session with solid gains. The S&P 500 rose 0.8% after spending most of the day near its highs. The index stumbled in the afternoon after a Financial Times report suggested Federal Reserve Chairman Ben Bernanke was likely to discuss modifying the Fed's asset purchase program at Wednesday's press conference.Netflix (NFLX 216.90, -6.62) jumped 7.1% after the company announced a multi-year partnership with DreamWorks Animation (DWA 24.28, -0.17).

On Tuesday, the major averages ended higher across the board and the S&P 500 advanced 0.8%. Equities climbed steadily since the opening bell as investors prepared for Wednesday's policy decision. The steady climb leading into the Wednesday session suggests investors expected mostly reassuring words from Chairman Bernanke.

The first half of Wednesday's session was rather uneventful, but the afternoon FOMC Statement and subsequent comments from Chairman Bernanke sent equities and Treasuries to their lows while also providing a significant boost to the dollar. During his remarks, Chairman Bernanke said if conditions continue to improve, the Fed could reduce the pace of purchases later this year with a potential end to purchases coming in the middle of 2014. He also suggested downside risks have diminished since the fall, but the Fed will not sell securities as long as the market remains in normalization stage. The Dollar Index saw the sharpest post-FOMC move as investors dumped other currencies in favor of the greenback. The afternoon bid sent the Index higher by 0.9% and allowed it to regain its 200-day moving average. Elsewhere, Treasuries fell victim to aggressive selling pressure as a loss of more than one point ran the 10-yr yield up 14 basis points to 2.332%. This marked the highest close since March 2012.

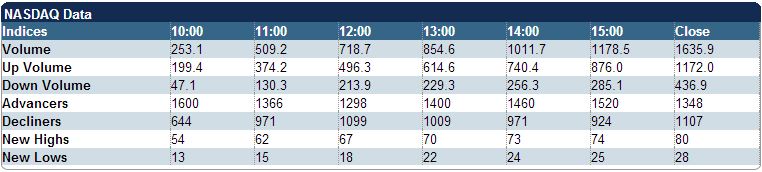

On Thursday, equities ended with sharp losses across the board as Wednesday's selling persisted into the next day, and dragged global shares into the fray. The S&P 500 fell 2.5% after losing its 50-day moving average at the open. Elevated Treasury yields contributed to selling in high-yielding, defensively oriented sectors. To that end, the consumer staples sector led to the downside with a loss of 3.0%. Health care (-2.6%) and utilities (-2.9%) also saw significant selling. Precious metals had a flashback to mid-April as gold sank 6.8% to $1280.10 per ounce while silver dropped 9.4% to $19.59 per ounce. ..NYSE Adv/Dec 1534/1521. ..NASDAQ Adv/Dec 1486/1016.

Raytheon Missile Systems Co., Tucson, Ariz., was awarded a sole-source, cost-plus-incentive-fee contract modification to contract HQ0276-13-C-0001. The total value of this effort is $126,000,000, increasing the total contract value from $53,446,254 to $179,446,254. Under this modification, the contractor will procure the material required to manufacture up to 29 SM-3 Block IB missiles. Work will be performed in Tucson, Ariz. with an estimated completion date of Sept. 30, 2016. Fiscal 2013 Defense Wide Procurement funds will be used to fund this effort. Contract funds will not expire at the end of the current fiscal year. This is not a foreign military sales acquisition. Missile Defense Agency, Dahlgren, Va., is the contracting activity.

Next Week In View

Jason's Commentaries

Jason's Commentaries

This week is really a very bearish week. Monday and Tuesday were apparently market pricing in for FOMC statements. After FOMC statements, where the Fed stated that they might taper QE later this year or in 2014. The key thing is, they're going to taper no matter what. The tapering of QE will likely not happen when Ben Bernanke is in office. After the release of FOMC statements, market went into a 2 day straight loss which wiped out the entire gains in May and June. Asia was also not spared from this bearish menace. STI wiped out its entire year's gain. Asia was also hammered by the fact that China's data was overstated.

Volume on Friday was at 1600m shares traded on NYSE on a expiration Friday. Bulls and Bears were approx having the same strength. Sectors were mixed with Tech and Materials down by 1% . Market was being lifted by Staples and Healthcare. On the broader sector movement, most sectors are being hammered and is on a down trend. On the technical side, it seemed that the market is likely to head down to 14200 on the Dow.

On the weekly side, we're heading towards the end of June. It seems that Sell in May has been pushed back to June. Perhaps Sell in May will end in June. Since we do not have much data coming out this week, perhaps we're likely end the week flat while the market is looking to gain back some gains that it lost from this week. Heads up for the volatility!

Market Call: DOWN

Date: 24 June 2013

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}