27 Feb 2013

Market Summary

Market Internals

Leaders and Laggards

Technical Updates

Briefing's Commentaries

|

After Hours

18:45 ET BWC +8.8%, ANIK +3.3%, GRPN -26.1%, BSFT -24.5%, MCHX -20.8% following earnings/guidance :

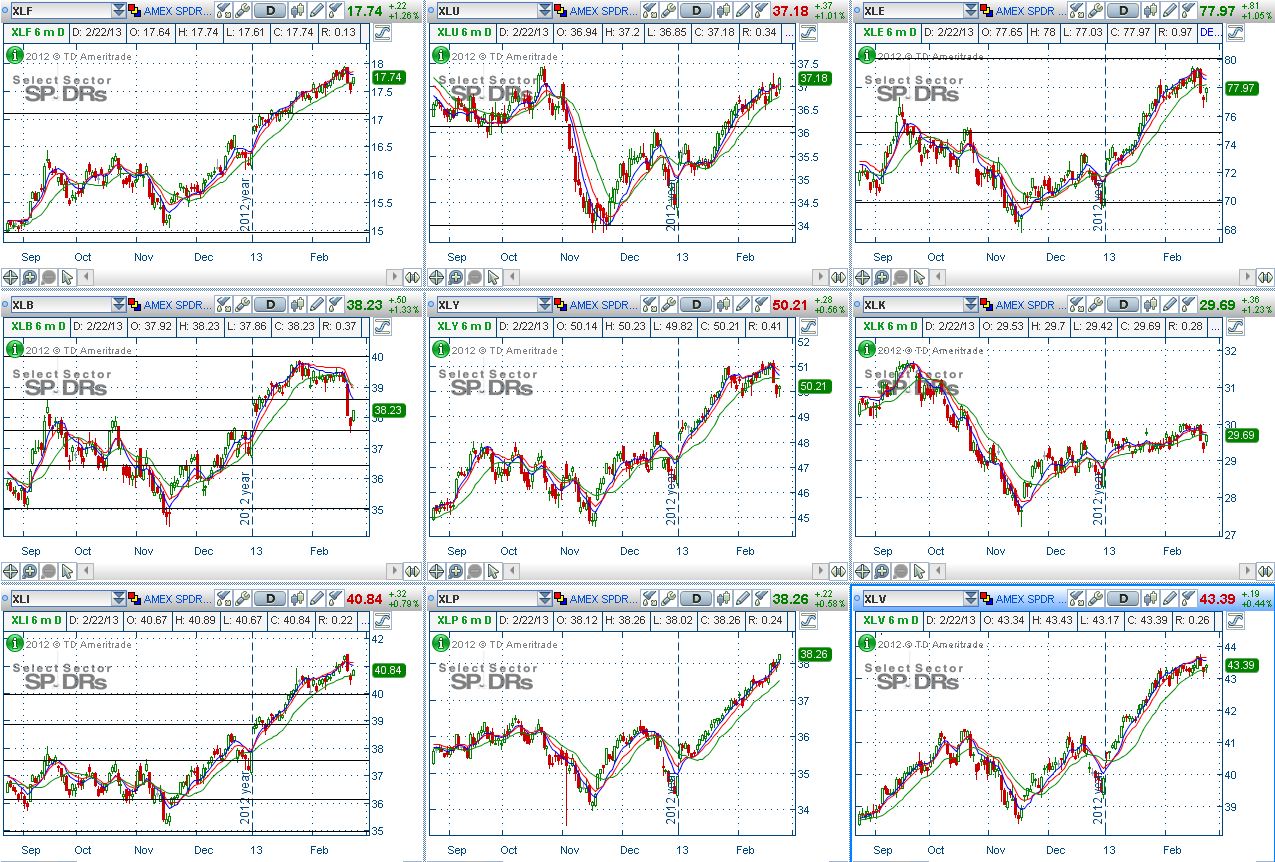

Today's session saw an extension of yesterday's buying as the S&P 500 managed to erase the remainder of its losses from Monday. The broad rally occurred with six of 10 sectors adding in excess of 1.0%. Cyclical stocks led the way with industrials and materials exhibiting relative strength from the start of the session.

Other notable after hours movers on earnings: BWC +8.8%, ANIK +3.3%, RGR +2.7%, MYL +2.6%, CLR +2.4%, PANL +2.2%, UAN +1.9%, CBI +1.2%, GTAT +1.0%, CECO +0.9%, VALE +0.8%, MNST +0.7%, ICFI +0.4%, CSGP +0.2%, GRPN -26.1%, BSFT -24.5%, MCHX -20.8%, ANW -17.3%, JCP -14.9%, VCRA -10.9%, BOOM -2.8%, IILG -1.8%, ARI -1.7%, MBI -1.3%, DAR -1.2%, WES -1.1%, AFCE -0.9%, CHDN -0.9%, PODD -0.9%, PACD -0.8%, LTD -0.7%, DEL -0.5%, HNSN -0.4%, IOC -0.4%, WLL -0.4%, LINTA -0.3%, BEE -0.2%, MWE -0.1%

Today after the close the following companies reported earnings: CBI, ITC, CSGP, MTSN, STNR, WLL, ELGX, MYL, BOOM, AHT, FARO, KRA, RGR, RJET, STAA, WES, AMSF, ARI, DXPE, GMED, MCHX, ICFI, BSFT, CBEY, CHDN, EXAM, MMLP, UAN, VCRA, CWT, DPM, IILG, AFCE, BWC, CDXS , CLR, DVR, EXL, HNSN, MBI, MNST, MWE, PANL, RLJ, AGO, CECO, DAR, EPAM, GRPN, PODD, JCP, ANW, LTD, IOC, CPRT, PLL, GEF, WGP

Futures are mixed after hours: S&P 500 futures are +0.81 from fair value of 1514.59 and Nasdaq100 futures are -0.51 from fair value of 2740.76.

Tomorrow morning before the open three economic reports are scheduled to be released: 1) Initial Claims (Consensus 360k) and Continuing Claims (Consensus 3150k), 2) GDP - Second Estimate (Consensus 0.5%), and 3) GDP Deflator - Second Estimate (Consensus 0.6%).

Tomorrow before the open the following companies are scheduled to report earnings: DTEGY, DPZ, AIXG, LKQ, MTRN, MGLN, IRM, RDC, ANSS, AVD, BRY, CIR, CTRX, GTLS, IRDM, OCN, ORN, RNO, SNAK, VC, WNR, WPX, WWE, VRX, AWR, CVC, ISIS, PKT, TTI, BABY, GVA, NIHD, PQ, VITC, ACIW, FCN, HK, KSS, NXTM, SJI, BDBD, MTG, NAFC, SHLD, CHS, SDRL, BKS, MEI, TD

|

Commodities

Treasuries

Next Day In View

Jason's Commentaries

This has totally caught me with my pants down... I went bear and suddenly the DJIA spiked a 200 points? I find this really disturbing when I got stopped out, I found out that there was no volumes, no news supporting this rally. The volatility is getting wilder now, especially before the congress sit down to discuss their plans about the Sequester on Friday. When I look into the internals, I find it bullish but not very convincing. Perhaps the market makers are coming together to wipe the short interest out? Despite the spike, I am maintaining my view that this will be range bounded especially we're at a high right now. Most sectors led the market by more than 1% gain yesterday. Industrials, especially the defense industry was led by General Dynamics for winning a $200 million contract, have pulling up Lockheed Martin and Boeing in sympathy.

Market Call: DOWN

Date: 28 Feb 2013

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}