1 Feb 2013 AMC

Market Summary

Market Internals

Leaders and Laggards

Technical Updates

Commentaries

|

Commodities

Treasuries

Weekly Analysis

Week 38

Technical Updates

Briefing's Commentaries

Weekly Wrap

Week in Review: Equities Book Solid January Gains

On Monday, the major averages ended the session largely where they began. The S&P 500 and Dow registered modest losses, while the Nasdaq added 0.2%, seeing relative outperformance from Apple (AAPL 453.62). The largest tech stock ended higher by 2.3% after disappointing earnings caused it to lose nearly 13.0% last week. The materials sector was the weakest performer. The observed weakness resulted from a Goldman Sachs downgrade of the U.S. steel sector. Following the downgrade, steel stocks saw broad selling and the Market Vectors Steel ETF (SLX 49.62) shed 1.4%.

Equities finished Tuesday's session on a mixed note. The Dow and S&P 500 gained 0.5% each, while the Nasdaq underperformed and ended flat. However, looking below the surface revealed the sector rotation which took place today. Health care, telecoms, and utilities were among the day's top performers as investors rotated into defensive-oriented stocks. Seagate (STX 33.67, -0.31) fell 9.4% after issuing guidance which disappointed investors. The sell-off occurred after Seagate rallied nearly 50.0% in the eight weeks leading up to its quarterly report.

On Wednesday, equities started the day on a mixed note, but the slightly bearish bias which persisted throughout the session caused the major averages to end near their lows. The S&P 500 slipped 0.4%, and was the weakest performing index. Amazon.com (AMZN 265.00, -0.50) jumped 4.8% after the online merchant reported its operating income well ahead of analyst expectations.

Thursday did not bring much change to the market as the S&P 500 slipped 0.3% and Nasdaq ended flat. Mixed trade unfolded amid economic data which was largely in-line with expectations. The personal income report stood out as the December increase of 2.6% was well ahead of the 0.7% rise expected by the Briefing.com consensus. However, the notable rise in personal income was due to a surge in personal income on assets as investors chose to lock in a lower capital gains tax rate ahead of the New Year. In addition to economic data, investors received several notable earnings reports. Ryder System (R 57.90, +1.12), MasterCard (MA 518.71, +0.31), and Qualcomm (QCOM 66.73, +0.71) gained between 0.5% and 4.6% after beating on earnings.

Month in Review: Equities Soar as Full Force of 'Fiscal Cliff' Averted

Responding favorably to the Congressional compromise on tax rates, the S&P 500 jumped 2.8% in the first week of 2013 and rarely looked back. Despite some mixed economic and earnings news along the way, the S&P 500 closed with a gain in 13 out of 21 sessions and ended January at 1498.27 its best level since December 2007. The Dow Jones Industrial Average for its part surged 5.8% and recorded its best January since 1989.

Economic Data Paints Bleak January Picture

The bulk of economic data reported during the month beat the Briefing.com consensus. However, data reported for the month of January often came up short.

Of the seven January reports, five fell short of expectations.

- The Empire Manufacturing Index, NAHB Housing Index, Philadelphia Fed Survey, Michigan Sentiment, and Consumer Confidence reports all missed expectations.

- Meanwhile, the ADP Employment Change and Chicago PMI surprised to the upside.

- The biggest drag on quarterly growth came in the form of a 6.6% decrease in government spending. This was largely due to a 22.2% decline in defense spending which followed a 12.9% increase during the third quarter.

- The change in private inventories also subtracted 1.27 percentage points from the change in real GDP.

- Personal consumption expenditures, which constitute more than 70% of GDP, rose 2.2%, which was the largest increase since the first quarter of 2012.

- Business investment rose 12.4%, which was the largest uptick since the third quarter of 2011.

The second half of the month saw the start of the fourth quarter earnings season.

- Most companies have beaten on the bottom line per usual, hurdling estimates that had been lowered in many cases by analysts ahead of the reports. Revenue growth is still weak, but similar to earnings, most companies have exceeded depressed top line growth estimates.

- Cautious guidance has been a common theme as many companies see headwinds in the first half of the year, although the default opinion is that the second half of the year should look better.

The Dow Jones Transportation Average gained 9.4% as truckers and railroads joined the rally enjoyed by airlines since mid-November.

Energy stocks also displayed relative strength and the SPDR Energy Select Sector ETF (XLE) advanced 8.3%. This was largely supported by a 6.2% rise in the price of crude oil. The energy component ended the month just a shade under $98.

The Health Care sector has been a standout, trailing behind only energy in the sector rankings on a year-to-date basis (+7.4%).

The discretionary sector has also been among the top performers in the S&P 500.

- Homebuilders continued their strength from 2012. The SPDR S&P Homebuilders ETF (XHB) ended January with a gain of 8.3%. Many builders reported strong fourth quarter earnings, replete with reports of strong backlogs and order trends.

The tech-heavy Nasdaq underperformed the remaining major indices as Apple (AAPL), which is the single largest index component, continued displaying weakness.

- Shares of Apple sold off through the first half of the month before pausing near the $500 level.

- A disappointing January 23 earnings report caused the stock to lose more than 10%. The company fell short of revenue expectations and issued downside guidance.

- The largest tech stock ended the month down 14.4%, at levels last seen in February 2002.

Defensive Stocks Bid into Second Half

During the second half of the month, defensive-oriented sectors started to attract increased buying interest.

- Telecoms (+1.8%) and utilities (+4.5%) registered the bulk of their gains during the second half of the month after the broader market had already seen the majority of its rise.

- Health care stocks enjoyed strength throughout the month as upbeat earnings supported the space.

As the S&P 500 hovers just 4.3% below its all-time high, challenges remain visible.

- A notable drop in consumer confidence occurred as the initial impact of the payroll tax cut expiration was felt by income earners.

- Sequester cuts are scheduled to go into effect in March, with the brunt of the impact to be absorbed by the defense sector.

- The debt ceiling issue has only been deferred rather than fixed.

- Japan's bold bid to weaken its currency and to inflate its economy is raising the risk of currency wars as other countries aim to support their exporters.

- Geopolitical issues are simmering, with conflicts in the Middle East starting to make headline waves (eg. Egypt, Israel/Syria/Iran) and North Korea toying with nuclear tests.

- Rising interest rates threaten to slow the housing recovery.

- Bullish sentiment, which is a contrarian indicator, is picking up noticeably.

Next Week In View

Jason's Commentaries

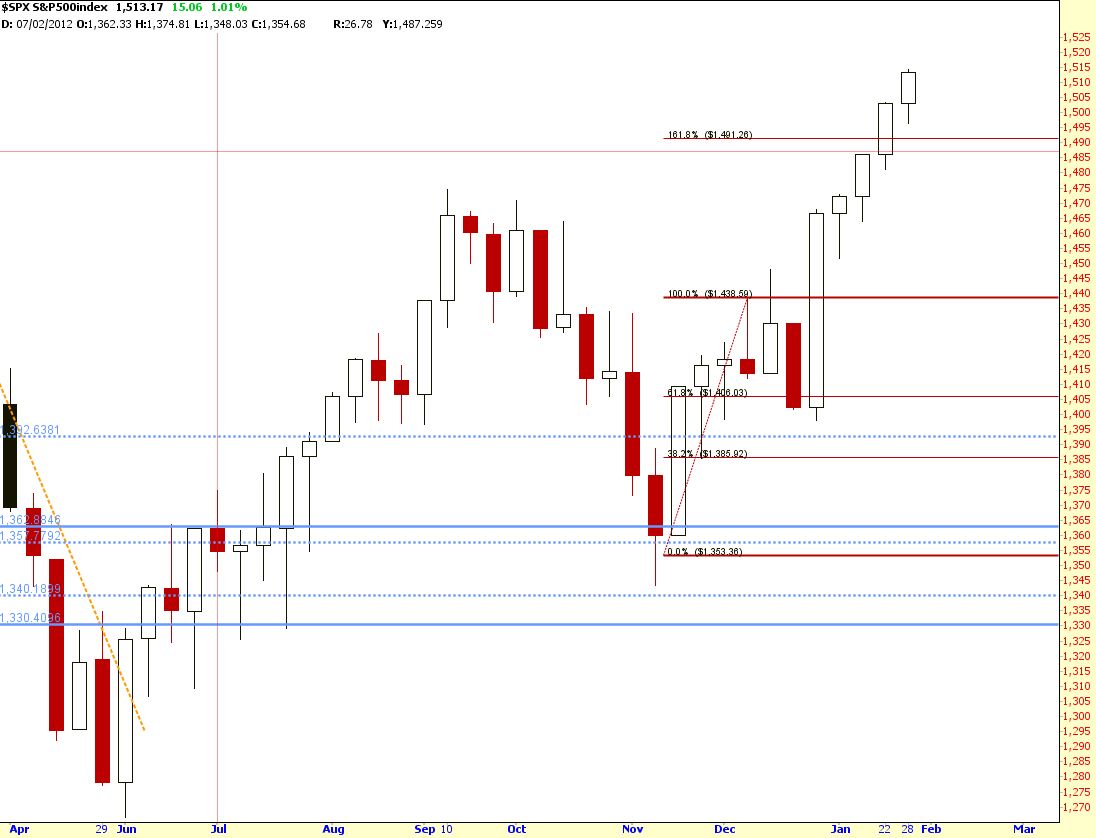

This is the best January the market has ever had since 1989. Market rallied all the way and broke the 14 000 mark on the first day of Feb. As history as shown, whenever the market crashes and recover, it will tend to break the previous high and it has been very reliable.

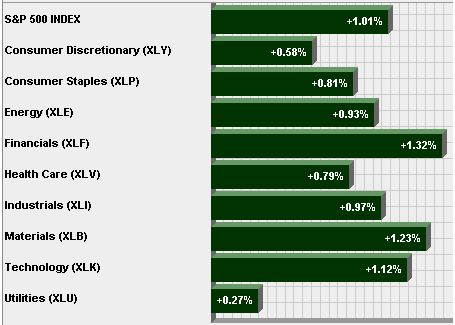

On Friday, we saw some disappointing numbers at the Non-farm Payrolls but surprisingly, it did not managed to drag the market down, while the ISM report showed some positive results to assist in its gains. Out of the 9 Sectors, 4 out of the 9 sectors made more than 1% gain, and industrials were almost gaining 1%. However, on the side note, out of 7 economic report in Jan, 5 showed poor results. It seems that market doesn't really care about the reports for Jan, but I'm sure that those will definitely weight on Feb's gain. Friday is definitely a strong bull day, with more than 700m shares traded in the NYSE and all the internals pointing to a bullish bias. Right now, it's only the industrials and the Tech within the 9 sectors that are not leading right now, which is not a very good thing. I believe Feb will be very volatile as the strong stocks might not be gaining much. Right now, the market is betting on a housing recovery, but the FOMC statement signaled there might be a bond bubble going on... HELLO... we talked about it long time back...

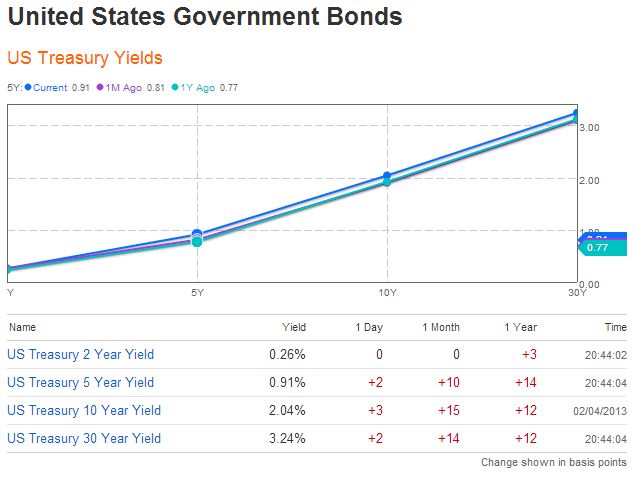

Treasuries rates have been pushed to a low since the subprime, and volumes in the equities market was nothing like before. Where has all the money gone to? Overseas and the Bond Market. Bond usually trap cash for a long period of time, and in anticipation of the Financial crisis, people are pushing money into low risk assets which locked the cash for a long time. This causes liquidity problem. And right now, bond has been selling down, looking at volumes returning to approx an average of 700m, it's good... but it looks like 2007 all over again.

In the first week of Feb, we don't have much reports coming out except for a major report coming out from the ECB. I believe the first week of Feb will likely to be flat and it's gonna be volatile, especially we're still in the earnings period and we're at the all time high at the market.

Market Call: Flat to downside

Market Call(Weekly): Flat to downside

Market Call(Weekly): Flat to downside

Date: 4 Feb 2013

No comments:

Post a Comment