22 Mar 2013 AMC

Market Summary

Market Internals

Leaders and Laggards

Technical Updates

Commentaries

|

| Stock Market Update |

16:25 ET Dow +90.54 at 14512.03, Nasdaq +22.40 at 3245, S&P +11.09 at 1556.89 :[BRIEFING.COM] Equity indices finished today's session firmly higher and the S&P 500 settled with a gain of 0.7%.

Stocks began the final session of the week on a positive note with notable strength in consumer stocks. The consumer discretionary sector paced today's advance from the opening bell after Nike (NKE 59.53, +5.93) and Tiffany (TIF 69.23, +1.32) reported bottom line beats and contributed to the relative strength of retailers. In addition, quick service restaurant operators outperformed after Darden Restaurants (DRI 49.62, +0.66) beat on earnings.

The growth-oriented discretionary sector was followed by its defensively-minded cousin, consumer staples. Food and beverage producers saw relative strength after reports indicated investor Nelson Peltz has built stakes in both Mondelez International (MDLZ 29.73, +1.17) and Pepsico (PEP 78.64, +2.49). The two stocks settled with respective gains of 4.1% and 3.3%.

The mixed sector leadership reflected a certain degree of uncertainty, which remains in the market. Going into the weekend, the situation in Cyprus remains unresolved with the latest reports indicating the Cypriot parliament has made some headway, but considerable funding needs remain unaddressed.

Although equities finished higher and appeared unconcerned by potential negative fallout from the inability to reach agreement, financials did not share that optimism. Bank of America (BAC 12.56, -0.01) and Citigroup (C 45.23, 0.00) ended little changed while the SPDR Financial Select Sector ETF (XLF 18.18, +0.11) underperformed the broader market with a gain of 0.6%. Notably, the financial sector proxy ETF ended the week lower by 1.5% as the possibility of a Cypriot exit from the eurozone weighed.

While major financials were tentative in their advance, the growth-oriented materials sector did not participate in the rally at all. After starting the session in line with the broader market, the SPDR Materials Select Sector ETF (XLB 39.07, +0.05) slid back to its unchanged level, and remained there until the close. The lack of a bounce in basic materials was notable as the sector bore the brunt of yesterday's selling.

Elsewhere, tech shares also underperformed notably in yesterday's action, but finished today in the middle of sector rankings. Although most tech stocks rebounded, Oracle(ORCL 31.98, -0.32) remained under pressure after reporting below-consensus earnings following Wednesday's close.

Trading volume was the lowest of the week as just over 620 million shares changed hands on the floor of the New York Stock Exchange.

Reviewing the final sector performance, consumer discretionary (+1.2%), consumer staples (+0.9%), energy (+0.8%), and telecom (+0.7%) finished in the lead. On the downside, materials (+0.1%), utilities (+0.2%), and financials (+0.5%) trailed behind the broader market.

There was no economic news released today with Monday's economic calendar also free of scheduled reports. |

|

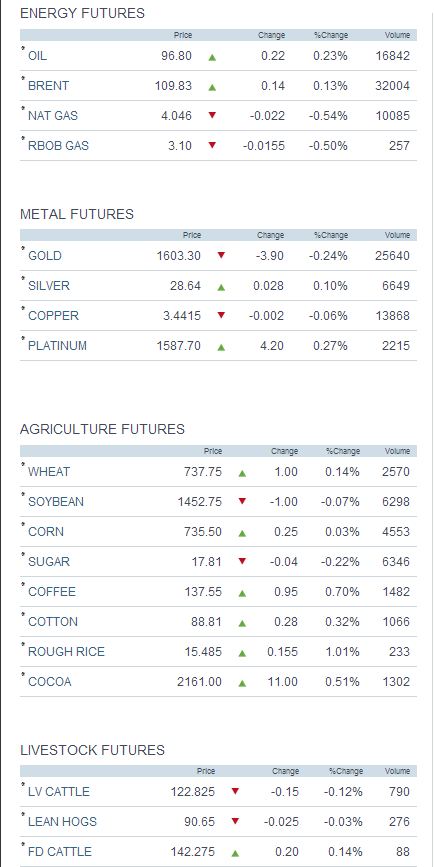

Commodities

Treasuries

Weekly Analysis

Week 38

Technical Updates

Briefing's Commentaries

On Monday, equities began the session amid broad losses after the conditions of a Cypriot bailout put the package in jeopardy of being voted down in the country's parliament. Per the original agreement, Eurozone rescue funds would provide Cyprus with EUR10 billion in recapitalization with a ‘stability levy' imposed on all bank accounts expected to raise an additional EUR5.8 billion. The financial sector bore the brunt of Monday's selling as bank stocks tend to show increased sensitivity in the face of political or economic uncertainty. Morgan Stanley (MS 22.18, +0.12) was the weakest performer among the majors, and the SPDR Financial Select Sector ETF lost 1.0%. Notably, European financials saw wider losses than their U.S. counterparts. Barclays (BCS 17.92, +0.13) and Deutsche Bank (DB 42.11, +0.11) settled lower by 4.1% and 3.6%, respectively. Tuesday's session began with slim gains, but the early strength lacked conviction as uncertainty continued to surround Cyprus and the terms of its proposed bailout. The expectation of a failed parliamentary vote was confirmed during the afternoon when the Cypriot MPs voted down the deposit tax with 36 ‘No' votes and 19 abstentions. The energy sector was the biggest laggard with a decline in the price of crude contributing to the weakness. The energy component slid 1.8% to $92.46. Meanwhile, the SPDR Energy Select Sector ETF (XLE 78.75, +0.62) settled lower by 1.1%. On Wednesday, the S&P 500 settled higher by 0.7% after spending the entire session in positive territory. The otherwise quiet session was highlighted by a policy statement from the Federal Reserve, which was largely in-line with expectations. With regards to economic conditions, the Committee observed a return to "Moderate economic growth following a pause late last year." Regarding price levels, "Inflation has been running somewhat below the Committee's longer-run objective, apart from temporary variations that largely reflect fluctuations in energy prices. Longer-term inflation expectations have remained stable." Industrial component FedEx (FDX 98.48, +1.98) endured a rough session and fell 6.9% after missing on the bottom line. The company also guided fourth quarter earnings below consensus due to a slowdown in global revenues. Thursday began in the red with tech stocks driving the early decline. The technology sector underperformed notably after disappointing earnings and cautious revenue guidance from Oracle contributed to selling in several other large cap names. While tech shares pressured the broader market from the opening bell, producers of basic materials declined steadily after France and Germany surprised the market with contractionary manufacturing and services PMI reports. The growth concerns regarding core eurozone economies weighed on the economically-sensitive sector and the SPDR Materials Select Sector ETF lost 1.7%. ..NYSE Adv/Dec 1877/1083. ..NASDAQ Adv/Dec 1447/955.

Next Week In View

Jason's Commentaries

Jason's Commentaries

Whoa.. Was right for the day. Having a up Friday as the market cheers the earnings from Nike and Tiffany, which resulted the leadership in the Consumer Discretionary Sector in the market. On top of that, a good reason was due to the support found in the Dow. Whichever case, the market is also wary of the highs that It can be making. Cyprus issues remains an unsolved crisis in Europe. On Friday, Cyprus's officials came back empty handed from Russia in hopes with a natural gas deal, after the depositary tax was being rejected in the parliament. As I'm writing the DMA, the Cyprus government reached a deal with the ECB to proceed with the bailout deal of 10 Billion Euros, on the condition to downside the 2 largest Cyprus banks. Futures shot up after the deal was released this afternoon. I'm expecting more sideway consolidation to come as there are a number of FOMC issues coming out this week, and 2 weeks later, it's gonna be the earnings season.

Market Call: FLAT

Date: 25 Mar 2013

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}