29 Nov 2015 AMC - Market poised for a volatile week after Thanksgiving

Jason's Commentaries

Approaching the Black Friday and Cyber Monday Sales, the market rallied in anticipation that the sale might be outstanding. This sale could be very critical to the US economy at present moment as the Fed might be looking at it to gauge the strength of the economy. If the sales numbers are good for the holiday sale, I believe the Fed might be more prone to raise the Fed Fund Rate in 2 Weeks time. However, the Fed's hands are tied and the max they can raise is 25 basis points. Facing very low inflation and deflation at the start of the year, Fed can't raise their rates very much else it will definitely send the US economy into a shock.

On the stock market, the market rallied from the drop at the end of Sep, completing the double bottom pattern. Right now, the market seemed to be on the uptrend with all sectors leading except Utilities and the Energy Sector. Nasdaq was able to rally much high and its counterparts due to much agressive M&A actions and earning results.

Volumes have picked up and averaged at around 950mil shares traded on the NYSE. VIX has been consolidating at approx 15 points which suggesting the market is not in a bearish mood at all.

Looking ahead, we're having a very volatile week ahead. With the employment reports coming out next week, we have other central banks like RBA, ECB, BOC annoucing their rates as well. It will be a wild ride for the currencies. However, I believed that the rates are likely to hold while awaiting Fed's decision.

Next week will likely to be consolidating as the economic matters bombard the market.

Market Summary

Before Market Opens

European Markets Closing Prices

European markets are now closed; stock markets across Europe performed as follows:

- UK's FTSE: -0.3%

- Germany's DAX: -0.2%

- France's CAC: -0.3%

- Spain's IBEX: -0.2%

- Portugal's PSI: +0.3%

- Italy's MIB Index: -0.1%

- Irish Ovrl Index: -0.3%

- Greece ASE General Index: +1.1%

S&P futures vs fair value: +2.00. Nasdaq futures vs fair value: +15.60.

Read more: http://www.briefing.com/Platinum/InDepth/InPlay.htm#ixzz3sqpBdLsa

The S&P 500 futures trade two points above fair value.

Asian markets ended lower across the board with China's Shanghai Composite diving 5.5% after securities regulators opened an investigation into securities brokers, including Citic Securities. Adding to the defensive sentiment was the October Industrial Profits report (-4.8%), which showed the fifth consecutive monthly decline.

- In economic data:

- Japan's October Household Spending -2.4% year-over-year (consensus 0.1%; previous -0.4%) and October National CPI +0.3% (expected 0.0%; last 0.0%). Also of note, November Tokyo CPI +0.2% year-over-year, as expected and Tokyo Core CPI 0.0% (consensus -0.1%; prior -0.2%)

------

- China's Shanghai Composite fell 5.5% with financials and brokerage shares leading the retreat. Citic Securities plunged 10.0% while Agricultural Bank of China and Bank of China both lost near 3.0% apiece.

- Hong Kong's Hang Seng fell 1.9% and bank shares were also pressured. China Construction Bank, Industrial & Commercial Bank, and Ping An surrendered between 1.5% and 2.5% while CNOOC also lagged, falling 2.7%.

- Japan's Nikkei shed 0.3% with Sharp, Yahoo Japan, and Konami falling 5.7%, 2.3%, and 1.5%, respectively. On the upside, Toshiba, Casio, and NEC outperformed with gains between 1.0% and 2.4%.

Major European indices trade in the vicinity of their flat lines with UK's FTSE (-0.2%) showing relative weakness. On a separate note, the latest reports regarding Greece indicate the country is expected to implement 13 more financial sector reforms before receiving a EUR1 billion aid package from the EU.

- Economic data was plentiful:

- Eurozone November Consumer Confidence -6.0 (expected -8.0; prior -8.0) and November Business and Consumer Survey 106.1 (expected 105.9; prior 106.1)

- Germany's December GfK Consumer Climate 9.3 (expected 9.2; last 9.4) and October Import Price Index -4.1% year-over-year (consensus -3.9%; prior -4.0%)

- UK's preliminary Q3 GDP +0.5% quarter-over-quarter, as expected; +2.3% year-over-year, as expected. Separately, Q3 Business Investment +2.2% quarter-over-quarter (consensus 1.5%; last 1.6%)

- France's October PPI +0.2% (prior +0.1%) and October Consumer Spending -0.7% month-over-month (expected -0.1%; last 0.1%)

- Italy's November Business Confidence 104.6 (consensus 105.6; last 105.7) and Consumer Confidence 118.4 (expected 116.5; previous 117.0)

- Spain's CPI +0.3% month-over-month (expected 0.2%; previous 0.6%); -0.3% year-over-year (consensus -0.5%; last -0.7%)

------

- UK's FTSE is lower by 0.3% with miners showing relative weakness. Anglo American, BHP Billiton, Fresnillo, and Rio Tinto lead the slight pullback with losses between 2.3% and 6.2%. On the upside, consumer and telecom names outperform with Dixons Carphone and Vodafone up 1.3% and 0.4%, respectively.

- Germany's DAX hovers near its flat line with Infineon Technologies extending yesterday's earnings-driven gain. The stock has surged 3.2% while other advancers show gains of no more than 0.8% (Daimler and Continental). On the downside, RWE is lower by 2.4% and Volkswagen trades down 0.3%.

- In France, the CAC trades flat amid strength in financials. AXA, BNP Paribas, and Credit Agricole have added between 0.2% and 1.4%. Consumer names have struggled with Louis Vuitton and Kering down 1.1% and 0.4%, respectively.

Read more: http://www.briefing.com/Platinum/InDepth/InPlay.htm#ixzz3sqpBdLsa

Market Internals

Market Internals

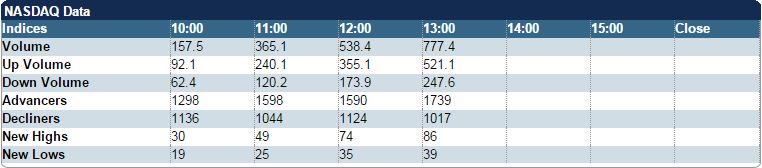

Nasdaq was up to 5128 (+0.22%). Dow was down to 17798 (-0.08%). S&P500 was up to 2090 (+0.06%). Today was half day. Action came on lower than average volume (NYSE 388 mln vs. avg. of 958; NASDAQ 779 mln vs. avg. of 1918), with advancers outpacing decliners (NYSE 1857/1216, NASDAQ 1739/1017) and new highs outpacing new lows (NYSE 94/48, NASDAQ 86/39).

Relative Strength:

First Trust ISE Global Wind Ene-FAN +1.79%, Sweden -EWD +1.25%, PowerShares WilderHill Clean En-PBW +1.21%, Cotton Sub-BAL +1.14%, Italy Capped -EWI +1.13%, Belgium Capped Inv-EWK +1.13%, Germany -EWG +1.12%, Austria Capped Inv-EWO +1.08%, Shipping -SEA +1.01%, iPath S&P 500 VIX Short Term Fu-VXX +0.93%

Relative Weakness:

TR Russia -RSX -3.97%, South Africa -EZA -3.61%, United States Natural Gas -UNG -3.34%, Vietnam -VNM -2.9%, Turkey Investable -TUR -2.85%, United States Oil -USO -2.76%, S&P Middle East & Africa E-GAF -2.72%, S&P Oil & Gas Explor & Pro-XOP -2.38%, Coal -KOL -2.23%, Junior Gold Mine-GDXJ -2.14%

Read more: http://www.briefing.com/Platinum/InDepth/InPlay.htm#ixzz3sqoYpnHK

Leaders and Laggards

Technical Updates

Commentaries

Closing Market Summary: Stocks End Flat Week on Quiet Note

The stock market meandered in a narrow range through the abbreviated Friday session, ending the day and the week on a flat note. The S&P 500 added 0.1% today, ending the week higher by two points (+0.1%).

Unsurprisingly, the Friday session was very quiet with trading volume running well below average. To that point, only 378 million shares changed hands at the NYSE floor. The lack of activity in the U.S. masked a relatively busy overnight session that featured a 5.5% dive in China's Shanghai Composite after regulators expanded their investigation into major securities brokers, including Citic Securities.

Once the focus shifted to the Wall Street session, equities ticked lower due to relative weakness in consumer discretionary (-0.4%) and energy (-0.7%), but gains in the remaining sectors offset the softness in the two cyclical groups.

Media names kept the discretionary sector under pressure with Dow component Disney (DIS 115.13, -3.54) falling 3.0% to mid-November levels. Meanwhile, the energy sector retreated as crude oil fell 2.5% to $41.97/bbl.

On the upside, the consumer staples sector (+0.4%) held the lead throughout the session while top-weighted technology (+0.2%) and financials (+0.2%) also finished ahead of the broader market. Chipmakers underpinned the tech sector after NXP Semiconductor (NXPI 88.36, +3.82) received clearance from the Federal Trade Commission to continue its acquisition ofFreescale Semiconductor (FSL 37.35, +1.45). The two names surged 4.6% and 4.0%, respectively, while the PHLX Semiconductor Index spiked 0.7%.

Treasuries held gains during overnight action, but they returned to little changed intraday with the 10-yr yield at 2.23%.

Investors did not receive any economic data today; however, Monday will include a couple releases with November Chicago PMI (Briefing.com consensus 55.0) and October Pending Home Sales (consensus 0.7%) set to be reported at 9:45 ET and 10:00 ET, respectively.

- Nasdaq Composite +8.3% YTD

- S&P 500 +1.5% YTD

- Dow Jones Industrial Average -0.1% YTD

- Russell 2000 UNCH YTD

Week in Review: Stocks Hold Ground

The stock market began the trading week on a cautious note with the S&P 500 shedding 0.1%. The benchmark index surrendered its opening gain, ending in the middle of its trading range while the Dow (-0.2%) and Nasdaq (-0.1%) registered comparable losses. Equities climbed at the start with the early move supported by three sectors in particular. The energy sector (+0.7%) displayed some early volatility, but ended among the leaders even though crude oil slipped 0.3% to $41.78/bbl after making a brief appearance above $42.50/bbl. WTI crude briefly spiked in the morning after Saudi officials indicated their intent to stabilize the global energy market, but the energy component was back near its flat line in short order. Elsewhere among cyclical sectors, consumer discretionary (+0.4%) and materials (+0.1%) also settled ahead of the broader market. The discretionary sector benefitted from strength among retailers with SPDR S&P Retail ETF (XRT 44.58, +0.42) climbing 1.0%.

Tuesday ended on a flat note with stocks overcoming an opening retreat that was fueled by a military incident, which is likely to invite geopolitical implications going forward. The S&P 500 added 0.1% while the Nasdaq Composite (unch) underperformed. Early in the morning, it was reported that the Turkish military shot down a Russian fighter jet, which allegedly violated Turkish airspace on the country's border with Syria. This marked the first time that a NATO member downed a Russian plane since the 1950s. After initial confusion, Russian military officials said that one pilot was rescued while the other was killed by Syrian opposition fighters after ejecting from the plane. The Russian defense ministry called the incident a "hostile act" while President Vladimir Putin terminated all Russian military cooperation with Turkey. Mr. Putin denied the incursion into Turkey, saying the action represented "backstabbing by accomplices of terrorists" and that it "goes beyond [the] fight against terror." The news was met with a spike in Treasuries and the 10-yr note then notched a new high shortly after the release of the second estimate of Q3 GDP (+2.1%; Briefing.com consensus +2.0%); however, the 10-yr note spent the rest of the day in a slow retreat from morning highs to end with a small gain that lowered the benchmark yield one basis point to 2.24%.

The stock market ended Wednesday on a flat note with trading volume running well below average as some market participants got an early jump on the Thanksgiving holiday. The S&P 500 settled just below its flat line while the Nasdaq Composite (+0.3%) outperformed. Investors received a boatload of economic data in the morning, but there was little response in the market as stocks opened flat and inched higher to establish narrow trading ranges that held throughout the day. For instance, the S&P 500 spent the session in a seven-point range with seven sectors offsetting gains in three groups that outperformed throughout the day. Heavily-weighted health care (+0.5%) and consumer discretionary (+0.5%) seized the lead in the early going and held their ground into the close. The health care sector received support from biotechnology, evidenced by a 1.1% spike in iShares Nasdaq Biotechnology ETF (IBB 338.85, +3.58).

Bond and equity markets were closed on Thursday for Thanksgiving.

Read more: http://www.briefing.com/Platinum/InDepth/InPlay.htm#ixzz3sqocEQPS

Treasuries

Treasury Market Summary: Waiting for the Big Week Ahead

- The Treasury market closed Friday's session looking like the stock market did: mixed and little changed. More of the buying interest (what little there was) was concentrated in shorted-dated securities while longer-dated instruments sort of just sat there.

- 2-yr -2 bps at 0.92%

- 5-yr -2 bps at 1.65%

- 10-yr -1 bp at 2.22%

- 30-yr unch at 3.00%

- The trading action was uneventful, which is not surprising given that it was an abbreviated session following Thursday's Thanksgiving holiday. The lack of any geopolitical upset also allowed for a pretty tame session.

- There was also a wait-and-see element at work with traders cognizant that the coming week is going to contain a host of important developments:

- The IMF decision Monday on whether China's currency will be included in its Special Drawing Rights basket

- Several speaking engagements by Fed Chair Yellen, including her monetary policy testimony before the Joint Economic Committee on Thursday

- Manufacturing PMI reports from around the globe

- Central bank policy meetings for the Reserve Bank of Australia (Monday), the Reserve Bank of India (Tuesday), the Bank of Canada (Wednesday), and the European Central Bank (Thursday)

- OPEC's meeting on Friday; and

- The November Employment Situation Report on Friday

- Friday's excitement was reserved primarily for the currency and commodity markets.

- The US Dollar Index traded as high as 100.20 with the euro and the Swiss franc weakening noticeably in front of next week's ECB meeting; however, the euro recouped just about everything it lost, which dropped the US Dollar Index back to 100.02.

- With the greenback's strength fading, there was no reprieve for oil prices. They settled down 3.1% at $41.71 per barrel. Gold also got hit, falling 1.3% to $1056.20 and suffering its sixth straight weekly decline.

Read more: http://www.briefing.com/Platinum/InDepth/InPlay.htm#ixzz3sqoUcuDg

On other news....

Currencies

Currency Commentary: DXY Holding 100

- The Dollar Index is maintaining the 100 level but it has yet to test the multi-year high of 100.39 set back on March 13. It has been a quiet session as is typical of the post-Thanksgiving Friday. News out over Thanksgiving was light with headlines about the on-going feud between Russia and Turkey over the downed jet and the China 5% decline being the most notable. None of these are having a major impact on trade. Next week, Fed Chair Janet Yellen will speak (Tue & Wed), the Fed Beige book is due out (Wed), and the November Jobs Report (Fri) will be closely followed events.

- The euro is battling to hold the 1.06 level ahead of next week's ECB meeting (Thu). The central bank is expected to expand its current QE program in an attempt to boost growth and pricing. This will remain a significant headwind for the single currency.

- The pound is holding the 1.50 level at the moment. The country did not see any revision to its Q3 GDP number which was up 0.5% q/q.

- The yen continues to trade in the 122-123 area. The country saw its Unemployment Rate fall to 3.1% (from 3.4% in prior) and had a small beat on the CPI. But the inflation gauge remains well below the Bank of Japan's target. Household Spending in the region fell short of expectations.

- The Swiss franc has been garnering attention this morning following its sudden decline at the open of European trade. The franc fell from 1.0230 to 1.0320 against the dollar. Against the euro it dropped from 1.0860 to 1.0920. The moves led to speculation that the SNB was back intervening in the currency. This would mark the first move by the central bank since it surprised markets and removed its 1.20 peg against the euro currency. The theory here is that the SNB is moving to protect its currency ahead of next week's ECB meeting (FOREX, BONDX).

Read more: http://www.briefing.com/Platinum/InDepth/InPlay.htm#ixzz3sqovc3jf

Next Week In View

Economic Commentaries

Economic Summary: No US data today; Existing Home Sales Monday at 10:00 AM ET

Upcoming Economic Data:

- Chicago PMI for November due out Monday at 09:45 ET (Briefing.com consensus 55.0; Prior 56.2) and October Pending Home Sales (Briefing.com consensus +0.7%; prior -2.3%) due at 10:00 ET

Other International Events of Interest

- Eurozone November Consumer Confidence -6.0 (expected -8.0; prior -8.0) and November Business and Consumer Survey 106.1 (expected 105.9; prior 106.1)

- Equities in China tumbled after a few securities brokers disclosed government investigations into their businesses. In addition, industrial profits fell for the fifth consecutive month

Read more: http://www.briefing.com/Platinum/InDepth/InPlay.htm#ixzz3sqp22Ahc

Weekly Market Call: Volatile to downside

Date: 29 Nov 2015