18 Jan 2013 AMC

Market Summary

Market Internals

Leaders and Laggards

Technical Updates

Commentaries

|

Commodities

Treasuries

Weekly Analysis

Week 38

Technical Updates

Briefing's Commentaries

Weekly Wrap

Dow +53.68 at 13649.7, Nasdaq -1.29 at 3134.71, S&P +5.04 at 1485.98

Equities began the session on a rather uninspiring note, but managed to climb back into positive territory by day's end. The key indices got off to a slow start despite China reporting its 2012 GDP growth at 7.9%. While the reading beat expectations, investor optimism was contained to the Asian session. Domestically, the lone economic data point came from the University Michigan, which reported its preliminary January consumer confidence measure at 71.3. The report was a disappointment and it contributed to the early weakness observed in the major averages.

The S&P 500 and Dow staged an afternoon recovery back into positive territory after headlines out of Washington indicated Republican lawmakers are open to a three-month debt ceiling extension. While the reports were met with initial resistance from top Democrats, the White House was said to be ‘encouraged' by the proposal.

The 30-stock Dow Jones was the top performing index, and positive earnings fromGeneral Electric (GE 22.04, +0.74) contributed to the relative strength. The conglomerate reported earnings growth in five of its seven segments, and its stock gained 3.5% on the back of the strong results.

While the Dow and S&P 500 registered gains, the Nasdaq ended lower due to pressure from two major components.

Intel (INTC 21.25, -1.43) reported a fourth quarter earnings beat, but its top line results as well as forward guidance were disappointing. The stock slid 6.3% and other semiconductor manufacturers underperformed as well. The PHLX Semiconductor Index slipped 0.5%.

Apple (AAPL 500.00, -2.68) also weighed on tech shares. The stock shed 0.5% after supply concerns were revisited after reports out of Reuters indicated that Sharp, which supplies screens for the iPad, has slowed its production rate. The demand concerns spilled over to other Apple supplier as Qualcomm (QCOM 64.48, -0.45) and Skyworks(SKWS 20.88, -0.78) lost 0.7% and 3.6% respectively.

Additionally, the market received earnings from two major financials. American Express(AXP 59.78, -0.96) settled lower by 1.6% after reporting earnings in-line with its January 10 preannouncement. On the upside, Morgan Stanley (MS 22.38, +1.63) surged 7.9% after reporting a bottom line beat.

Crude oil shed 0.1% and ended at $95.38 after trading in a narrow range for the duration of the session.

Also of note, the CBOE Volatility Index (VIX 12.33, -1.24) sank 9.1% and finished at its lowest level since April 2007.

Floor volume at the New York Stock Exchange was aided by the January options expiration, and totaled 1.07 billion shares, which was well above average.

Sector leadership came from industrials (+1.0%) and the utilities (+0.9%) space. On the downside, technology shares were the biggest laggard (-0.3%), followed by financials (+0.2%).

As mentioned earlier, today's economic data was limited to the preliminary January University of Michigan Consumer Sentiment Survey. The report came in at 71.3, which was lower than the 72.9 that was posted in the prior month, and worse than the reading of 75.0 that had been expected by the Briefing.com consensus.

Note that equity and bond markets will be closed on Monday in observance of Martin Luther King Day. On Tuesday, December existing home sales will be reported at 10:00 ET. Among earnings of note, Google (GOOG 704.51, -6.81) and VerizonCommunications (VZ 42.54, +0.41) are scheduled to report on Tuesday. Verizon will announce its quarterly results ahead of the opening bell while Google is scheduled for an after-hours release.

Week in Review: Equities Climb to Highest Weekly Close Since 2007

Monday's session began on a lower note after pre-market weakness in Apple (AAPL 500.00, -2.68) weighed on the tech-heavy Nasdaq. Meanwhile, the S&P 500 marked its session low in the 1465 area an hour into the session. The benchmark index then reversed and spent the remainder of the session climbing back near its flat line before finishing with a slim loss. Dell (DELL 12.84, +0.02) was on the move today after Bloomberg TV reported the PC maker is in talks with private equity regarding a potential buyout. Dell surged 13.0% on the news.

On Tuesday, equities began the day with a slightly bearish bias after Germany's 2012 GDP was reported below expectations. Though the news weighed at the open, the major averages showed resilience, and spent the remainder of the session climbing off their lows. As a result, the S&P 500 added 0.1% while the Nasdaq underperformed with a loss of 0.2%. Lennar (LEN 42.08, +0.14) was the first homebuilder to report its fourth quarter results. The report was generally positive as the company's earnings and revenue exceeded the Capital IQ consensus estimates. In addition, the company expects its full-year 2013 gross margins to be in-line with analyst estimates. Despite the upbeat earnings, Lennar settled lower by 0.8%. It should be noted the stock has added over 36% over the past five months, thus strong quarterly results have been largely priced-in.

On Wednesday, major stock market averages started the day on a mixed and uneventful note and that's pretty much how they traded the rest of the day. There were plenty of storylines, but there wasn't any conviction on the part of buyers or sellers outside of some individual stock stories. Boeing (BA 75.04, -0.22) underperformed after two Japanese carriers suspended their Dreamliner flights due to safety concerns.

Thursday's session opened on a strong note after weekly initial claims and housing starts were reported ahead of expectations. Meanwhile, a disappointing Philadelphia Fed Survey was not enough to cool optimism. Key indices spent the duration of the day in a steady upward climb, and the S&P 500 made its biggest advance in more than a week to end higher by 0.6%. The market saw notable support from homebuilders after December housing starts data indicated the demand for fresh construction projects remains strong. The SPDR Homebuilders ETF (XHB 28.21, +0.06) settled higher by 1.9%.

Next Week In View

Jason's Commentaries

What a flat day at the start, while at the end of the trading day, the market rallied back as it was a start of a long weekend in observance of Martin Luther King's day, a public holiday in US. The start of the trading day was flat, however gained some inertia from China's GDP report, stating that the Chinese's economy grow by another 7% last quarter. However, other economic report was not as pleasing.

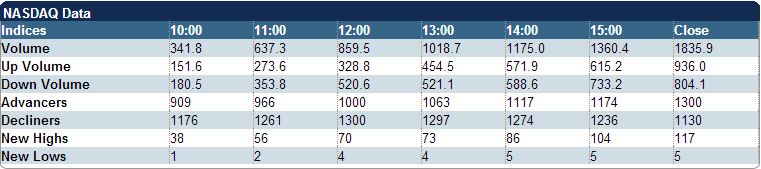

Intel and Apple provided a huge lag to the Tech sectors while GE and Morgan Stanley provided the market a boost as well. Also, the VIX sunk another 7% to a fresh low in 5 years. Looking at the internals, the volumes were exceptionally high on the NYSE on Friday, hitting 1B shares traded, with the UVOL outpacing the DVOL 2:1. Other internals were also pointing towards a bullish Friday.

On the Technical updates, the DOW just hit a fresh high at 13650, despite not very impressive earnings though... I wonder how high would it get. The debt ceiling discussion might prove to be a catalyst for the market to go into a correction? On the weekly chart, it really does seem to be in a rally mode. We're very very likely to end the year with a positive Jan.

While for the next week, we got 2 more housing report coming up. Since the current week's building permits is already pointing to good home sales which got the homebuilders up to a high. I wonder would Conrad's 4 year recessionary cycle would come true. Though, we're delayed in the another recession already... Seems that we might get it this year...

Market Call: DOWN

Date: 22 Jan 2012

No comments:

Post a Comment