19 Apr 2013 AMC

Market Summary

Market Internals

Leaders and Laggards

Technical Updates

Commentaries

|

Commodities

Treasuries

Weekly Analysis

Week 38

Technical Updates

Briefing's Commentaries

On Monday, equities sold off steadily throughout the day, and the S&P 500 lost 2.3%, registering its biggest one-day drop of the year. The major averages were pressured from the opening bell as global growth concerns returned to the forefront. In China, first quarter GDP rose 7.7%, which was below the expected growth of 8.0%. The disappointing report added to the weakness of the commodity complex, which saw an extension of last week's selling. Gold miners endured a rough session as theMarket Vectors Gold Miners ETF (GDX 28.59, +0.37) fell 9.9% on the heels of a 9.5% plunge in gold to $1356.80. Meanwhile, silver tumbled 13.0% to $22.90.

Tuesday brought some relief as the S&P 500 climbed 1.4%. While the economically-sensitive materials space was able to rebound and end atop the leaderboard, the defensively-geared consumer staples were not far behind. Staple stocks received some support from Coca-Cola (KO 42.66, +0.56) after the beverage giant narrowly beat the Capital IQ earnings estimate. A defensive bid also buoyed the health care sector where Johnson & Johnson (JNJ 84.49, +1.31) gained 2.1% after beating on earnings.

Sellers reemerged during Wednesday's session as the S&P 500 tumbled 1.4%. Technology stocks felt the brunt of the drop as the SPDR Technology Select Sector ETF (XLK 29.35, +0.04) lost 2.1%. Apple (AAPL 390.53, -1.52) dipped below $400 for the first time since December 2011, and settled lower by 5.5%.

Thursday saw a continuation of Wednesday's selling. The S&P 500 shed 0.7% to close below its 50-day moving average for the first time since December 28, 2012. Cyclical sectors were under pressure with technology stocks once again finishing among the laggards. Elsewhere, the cyclical discretionary sector also finished in the red as homebuilders slumped. ..NYSE Adv/Dec 2189/817. ..NASDAQ Adv/Dec 1684/780.

Next Week In View

Jason's Commentaries

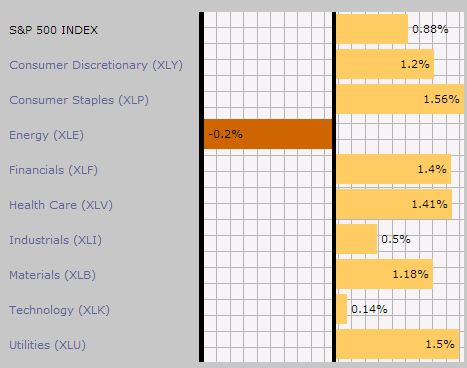

Oh well... Market was up again... it seems that the market still has some strength to sustain not its not going down streak.. Although the Dow lagged behind due to IBM's weak earnings, the wider market is performing well. S&P500 was up near a 1% and the energy sector was the only laggard. Tech outperformed as Google and Microsoft was able to do well in their earnings. However, I do not see much upside in the market as a significant number of the Dow components and the big caps stocks are missing their earnings. Such as IBM, Bank of America etc. On the technical update, on the weekly side we have a chopstick top, while we're likely have a 3rd candle reversal. On Friday, we're also have the treasuries dropping as well. On Monday, we do not have much economic data coming out except the housing data. However, we have much more earnings coming tomorrow, which means it will hell of a gyration on Tuesday

Market Call: Flat to upside

Date: 22 Apr 2013

No comments:

Post a Comment