21 Feb 2014 AMC - S&P500 broke into new high ahead of Ukraine conflict

Market Summary

European markets are now closed; stock markets across Europe performed as follows:

UK's FTSE: 0.0%

Germany's DAX: + 1.1%

France's CAC: + 0.3%

Spain's IBEX: -0.5%

Portugal's PSI: + 1.0%

Italy's MIB Index: + 0.6%

Irish Ovrl Index: + 0.7%

Greece ATHEX Composite: + 1.3%

Before Market Opens

S&P futures vs fair value: -0.10. Nasdaq futures vs fair value: +0.20.

The S&P 500 futures trade right below fair value.

Markets across Asia ended mostly higher, buoyed by yesterday's advance on Wall Street. China's yuan posted it largest weekly decline on record, sliding 0.8% to 6.1448 against the greenback, and closing at its worst levels since July 2013. Also of note, the one-week SHIBOR saw a 9.9 basis point advance to 3.529%.

Japanese data was mostly better than expected as household spending (1.1% year-over-year versus 0.5% expected), preliminary industrial production (4.0% month-over-month versus 3.1% expected), and retail sales (4.4% year-over-year versus 3.9% expected) all outpaced estimates. Tokyo CPI saw a hotter than expected 0.9% year-over-year (0.8% expected) print. Elsewhere, Australia's private sector credit (0.4% month-over-month versus 0.5% expected) missed.

The S&P 500 futures trade right below fair value.

Markets across Asia ended mostly higher, buoyed by yesterday's advance on Wall Street. China's yuan posted it largest weekly decline on record, sliding 0.8% to 6.1448 against the greenback, and closing at its worst levels since July 2013. Also of note, the one-week SHIBOR saw a 9.9 basis point advance to 3.529%.

Japanese data was mostly better than expected as household spending (1.1% year-over-year versus 0.5% expected), preliminary industrial production (4.0% month-over-month versus 3.1% expected), and retail sales (4.4% year-over-year versus 3.9% expected) all outpaced estimates. Tokyo CPI saw a hotter than expected 0.9% year-over-year (0.8% expected) print. Elsewhere, Australia's private sector credit (0.4% month-over-month versus 0.5% expected) missed.

Japan's Nikkei lost 0.6%, sliding for a third straight day as the stronger yen weighed. Honda Motor lost 1.4% and Toyota Motor shed 1.2%.

Hong Kong's Hang Seng finished flat after early strength was rejected by the 100-day moving average. Property developers outperformed as China Overseas Land & Investment added 1.2% and Sino Land gained 1.1%. Meanwhile, financials led to the downside with Bank of Communications and Bank of China off 1.2% and 0.9%, respectively.

China's Shanghai Composite rose 0.4%, gaining for a third straight day. Property developers led as bargain hunters emerged following days of heavy selling. China Vanke led the group's advance, up 2.0%.

Major European indices trade mostly lower with Spain's IBEX (-1.1%) seeing the largest loss amid weakness in financials after the country's government began selling some of its shares in Bankia, which trades lower by nearly 5.0%.

Participants received several economic data points. Eurozone CPI rose 0.8% year-over-year (0.7% expected, 0.8% prior) while core CPI increased 1.0% year-over-year (0.8% consensus, 0.8% previous). Separately, the unemployment rate held steady at 12.0%, as expected. Germany's Retail Sales rose 2.5% month-over-month (1.0% expected, -2.1% prior) while the year-over-year reading increased 0.9% (-1.2% consensus, -1.5% last). French PPI slipped 0.6% month-over-month (-0.3% expected, 0.2% prior) and Consumer Spending fell 2.1% month-over-month (0.2% consensus, 0.2% prior). Italian CPI ticked down 0.1% month-over-month (0.1% expected, 0.2% prior) while the year-over-year reading rose 0.5% (0.7% consensus, 0.7% last). Separately, the monthly unemployment rate rose to 12.9% from 12.7% (12.7% expected).

Participants received several economic data points. Eurozone CPI rose 0.8% year-over-year (0.7% expected, 0.8% prior) while core CPI increased 1.0% year-over-year (0.8% consensus, 0.8% previous). Separately, the unemployment rate held steady at 12.0%, as expected. Germany's Retail Sales rose 2.5% month-over-month (1.0% expected, -2.1% prior) while the year-over-year reading increased 0.9% (-1.2% consensus, -1.5% last). French PPI slipped 0.6% month-over-month (-0.3% expected, 0.2% prior) and Consumer Spending fell 2.1% month-over-month (0.2% consensus, 0.2% prior). Italian CPI ticked down 0.1% month-over-month (0.1% expected, 0.2% prior) while the year-over-year reading rose 0.5% (0.7% consensus, 0.7% last). Separately, the monthly unemployment rate rose to 12.9% from 12.7% (12.7% expected).

Spain's IBEX is lower by 1.1% as financials weigh. Banco Popular Espanol, Banco de Sabadell, and CaixaBank are down between 2.0% and 3.4%.

France's CAC holds a loss of 0.3%. Steelmaker Vallourec is the weakest performer, down 2.6%. On the upside, hotel operator Accor is higher by 1.8%.

Great Britain's FTSE is lower by 0.1% with publisher Pearson seeing the largest loss. The stock trades lower by 7.3% after the company issued a disappointing outlook. On the upside, financials Hargreaves Lansdown and Old Mutual trade higher by 2.7% and 5.8%, respectively.

Germany's DAX trades up 0.2%. Fresenius Medical Care and Bayer hold respective gains of 1.7% and 0.7%. Deutsche Lufthansa underperforms with a loss of 1.4%.

Market Internals

Market Internals -Technical-

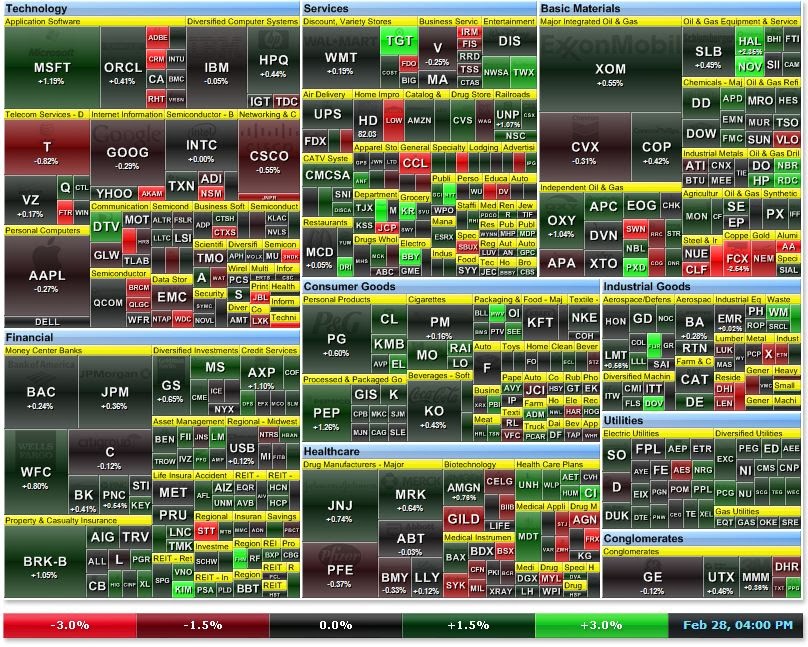

The Dow closed up 49 (+0.30%) at 16322, the S&P 500 closed up 5 (+0.28%) at 1859, and the Nasdaq closed down 11 (-0.25%) at 4308. Action came on above average volume (NYSE 944 mln vs. avg. of 709; NASDAQ 2346 mln vs. avg. of 1927), with advancers outpacing decliners (NYSE 1868/1242, NASDAQ 1199/1418) and new highs outpacing new lows (NYSE 228/19, NASDAQ 207/16).

Relative Strength:

Natural Gas-UNG +2.9%, Grains-JJG +2.36%, Corn-CORN +2.27%, Volatility-VXX +1.79%, Livestock-COW +1.64%, Poland-EPOL +1.48%, Egypt-EGPT +1.21%, Columbia Index-GXG +1.19%, Israel-EIS +1.07%, Swiss Franc-FXF +1.04%.

Relative Weakness:

Biotechnology-XBI -4.07%, Biotechnology-IBB -2.84%, Sugar-SGG -2.61%, Russia-RSX -2.32%, Telecommunications-IYZ -1.61%, Austria-EWO -1.5%, BRICs-EEB -1.48%, South Africa-EZA -1.33%, Middle East and Africa-GAF -1.33%, Technology-Software-IGV -1.23%.

The Dow closed up 49 (+0.30%) at 16322, the S&P 500 closed up 5 (+0.28%) at 1859, and the Nasdaq closed down 11 (-0.25%) at 4308. Action came on above average volume (NYSE 944 mln vs. avg. of 709; NASDAQ 2346 mln vs. avg. of 1927), with advancers outpacing decliners (NYSE 1868/1242, NASDAQ 1199/1418) and new highs outpacing new lows (NYSE 228/19, NASDAQ 207/16).

Relative Strength:

Natural Gas-UNG +2.9%, Grains-JJG +2.36%, Corn-CORN +2.27%, Volatility-VXX +1.79%, Livestock-COW +1.64%, Poland-EPOL +1.48%, Egypt-EGPT +1.21%, Columbia Index-GXG +1.19%, Israel-EIS +1.07%, Swiss Franc-FXF +1.04%.

Relative Weakness:

Biotechnology-XBI -4.07%, Biotechnology-IBB -2.84%, Sugar-SGG -2.61%, Russia-RSX -2.32%, Telecommunications-IYZ -1.61%, Austria-EWO -1.5%, BRICs-EEB -1.48%, South Africa-EZA -1.33%, Middle East and Africa-GAF -1.33%, Technology-Software-IGV -1.23%.

Leaders and Laggards

Technical Updates

Commentaries

Closing Market Summary: Stocks End Upbeat Week on Mixed Note

The stock market finished an upbeat week on a mixed note amid the return of concerns about the immediate future of Ukraine. The S&P 500 added 0.3% after holding a solid 0.6% gain through the bulk of the trading day. The Nasdaq Composite and Russell 2000 lagged, falling 0.3% and 0.4%, respectively.

The early advance occurred after the release of several data points that were cast in a bullish light.

Specifically, the second estimate for Q4 GDP was weak, revised down to 2.4% from 3.2%. That was able to be spun as a basis for why the Fed isn't going to hurry the pace of its tapering or the timing of the first hike in the federal funds rate. The Chicago PMI and Consumer Sentiment reports were better than expected, providing some hope that recent economic weakness is primarily a weather phenomenon. And, finally, pending home sales were up a disappointing 0.1% in January, playing back into the notion that the Fed is going to be deliberate with its handling of monetary policy.

The major averages reached their highs by midday, but the Nasdaq was much more tentative in its advance as large cap names traded little changed while biotechnology lagged. Appropriately, the afternoon selloff was paced by the index, which underperformed earlier in the day. Biotechnology was pressured considerably, sending the iShares Nasdaq Biotechnology ETF (IBB 264.42, -7.73) lower by 2.8%.

The afternoon weakness came about after multiple reports indicated that Russian troops have increased their presence in Crimea, which is located in Southern Ukraine. In addition to yesterday's seizure of the parliament building, armed gunmen also took control of two airports as well as the local television station and a telecommunications company. The reports were followed by comments from Ukraine's acting President Oleksandr Turchynov, who said Russia invaded the country ‘as a guise of exercise' with intent to ‘provoke a conflict.' President Turchynov urged Russian President Vladimir Putin to ‘show reason' and pull back the forces.

Despite the selloff, the S&P 500 was able to return into positive territory thanks to relative strength of heavily-weighted sectors like consumer discretionary (+0.5%), consumer staples (+0.7%), and financials (+0.5%).

With uncertainty back in the picture, participants rushed in search of volatility protection, which sent the CBOE Volatility Index (VIX 13.99, -0.05) from a session low of 13.49% to 14.79%. This represented a 9.6% swing in the near-term volatility measure before it settled near the middle of its range.

Elsewhere, Treasuries reclaimed a large portion of their morning losses. The benchmark 10-yr yield ended higher by two basis points at 2.66% after notching a session high at 2.70%.

Participation was above average with 944 million shares changing hands at the NYSE. MSCI rebalancing, which took place at the close, likely added some volume to the final tally.

Economic data included four reports:

The stock market finished an upbeat week on a mixed note amid the return of concerns about the immediate future of Ukraine. The S&P 500 added 0.3% after holding a solid 0.6% gain through the bulk of the trading day. The Nasdaq Composite and Russell 2000 lagged, falling 0.3% and 0.4%, respectively.

The early advance occurred after the release of several data points that were cast in a bullish light.

Specifically, the second estimate for Q4 GDP was weak, revised down to 2.4% from 3.2%. That was able to be spun as a basis for why the Fed isn't going to hurry the pace of its tapering or the timing of the first hike in the federal funds rate. The Chicago PMI and Consumer Sentiment reports were better than expected, providing some hope that recent economic weakness is primarily a weather phenomenon. And, finally, pending home sales were up a disappointing 0.1% in January, playing back into the notion that the Fed is going to be deliberate with its handling of monetary policy.

The major averages reached their highs by midday, but the Nasdaq was much more tentative in its advance as large cap names traded little changed while biotechnology lagged. Appropriately, the afternoon selloff was paced by the index, which underperformed earlier in the day. Biotechnology was pressured considerably, sending the iShares Nasdaq Biotechnology ETF (IBB 264.42, -7.73) lower by 2.8%.

The afternoon weakness came about after multiple reports indicated that Russian troops have increased their presence in Crimea, which is located in Southern Ukraine. In addition to yesterday's seizure of the parliament building, armed gunmen also took control of two airports as well as the local television station and a telecommunications company. The reports were followed by comments from Ukraine's acting President Oleksandr Turchynov, who said Russia invaded the country ‘as a guise of exercise' with intent to ‘provoke a conflict.' President Turchynov urged Russian President Vladimir Putin to ‘show reason' and pull back the forces.

Despite the selloff, the S&P 500 was able to return into positive territory thanks to relative strength of heavily-weighted sectors like consumer discretionary (+0.5%), consumer staples (+0.7%), and financials (+0.5%).

With uncertainty back in the picture, participants rushed in search of volatility protection, which sent the CBOE Volatility Index (VIX 13.99, -0.05) from a session low of 13.49% to 14.79%. This represented a 9.6% swing in the near-term volatility measure before it settled near the middle of its range.

Elsewhere, Treasuries reclaimed a large portion of their morning losses. The benchmark 10-yr yield ended higher by two basis points at 2.66% after notching a session high at 2.70%.

Participation was above average with 944 million shares changing hands at the NYSE. MSCI rebalancing, which took place at the close, likely added some volume to the final tally.

Economic data included four reports:

Fourth quarter GDP was revised down from 3.2% to 2.4% in the second estimate while the Briefing.com consensus expected GDP to be revised down to 2.6%. Just about all of the data that came in over the last couple weeks were worse than what the BEA expected when it released its advance estimate. There was really nothing new in the GDP report that was a surprise from the most current monthly releases. The important takeaway is that real final sales, which were revised down to 2.3% from 2.8%, now show absolutely no breakout from trends that go back to Q1 2012. The "surge" in economic growth that led to strong 2014 economic forecasts did not actually happen.

The Chicago PMI for February increased to 59.8 from 59.6 while the Briefing.com consensus expected a decline to 56.0. Analysts have been quick to point to extreme winter weather conditions as the culprit for the recent poor economic data trends. Yet, the blustery weather in February had absolutely no effect on Chicago-area manufacturers. This is another data point suggesting the weather is being used as a scapegoat during a cyclical down period.

The final University of Michigan Consumer Sentiment Index for February was revised up to 81.6 from 81.2 while the Briefing.com consensus expected an increase to 81.5. While the index moved in the opposite direction from the Conference Board's Consumer Confidence index, overall sentiment trends were relatively flat this month. Gains in equity prices offset slightly weaker employment conditions. Changes in gasoline prices and media reports likely had little effect on overall confidence values. The Current Conditions Index strengthened to 95.4 in the final reading from 94.0 in the preliminary. The Expectations Index was revised down to 72.7 from 73.0.

Pending home sales for January rose 0.1%, which was worse than the 0.8% increase forecast by the Briefing.com consensus. Today's reading followed last month's revised decrease of 5.8% (from -8.7%).

Nasdaq Composite +3.2% YTD

Russell 2000 +1.9% YTD

S&P 500 +0.6% YTD

Dow Jones Industrial Average -1.5% YTD

Commodities

Closing Commodities: Natural Gas Gains 2.4%, Crude Oil Rises 0.2%

Apr gold fell into negative territory despite weakness in the dollar index. The yellow metal retreated from its session high of $1333.20 per ounce and settled with a 0.8% loss at $1321.40 per ounce. Still, gold gained 6.6% in February on soft economic data and political unrest in Ukraine.

May silver also slipped into the red after pulling back from a session high of $21.42 set at floor trade open. Prices sold off further heading in to the close, leaving silver to settle 0.6% lower at $21.22 per ounce. The metal gained 10.8% in February.

April crude oil touched a session low of $101.80 per barrel moments after pit trade opened but rallied into positive territory later in morning action. It advanced to a session high of $102.96 per barrel and settled with a 0.2% gain at $102.58 per barrel. The energy component rose 6.1% over the month as it gained support on inventory data and a weaker dollar index.

Apr natural gas trended higher after lifting from its session low of $4.54 per MMBtu. It peaked at $4.66 per MMBtu and settled at $4.62 per MMBtu, or 2.4% higher. The April contract gained 3.8% over the month.

CBOT Agriculture and Ethanol/ICE Sugar Closing Prices

May corn rose 7 cents to $4.63/bushel

May wheat rose 10 cents to $6.01/bushel

May soybeans rose 27 cents to $14.15/bushel

Apr ethanol rose 10 cents to $2.23/gallon

May sugar (#16 (U.S.)) fell 0.02 of a penny to 22.13 cents/lbs

NYMEX Energy Closing Prices

· Apr crude oil rose $0.20 to $102.58/barrel

Crude oil touched a session low of $101.80 moments after pit trade opened but rallied into positive territory later in morning action. It advanced to a session high of $102.96 and settled with a 0.2% gain. The energy component gained 6.1% over the month as it gained support from inventory data and a weaker dollar index.

· Apr natural gas rose 11 cents to $4.62/MMBtu

Natural gas trended higher today after lifting from its session low of $4.54. It peaked at $4.66 and settled with a 2.4% gain. The April contract rose 3.8% over the month.

· Apr heating oil settled unchanged at $3.01/gallon

· Apr RBOB rose 2 cents to to $2.98/gallon ts/lbs

COMEX Metals Closing Prices

· Apr gold fell $10.40 to $1321.40/oz

Gold fell into negative territory despite weakness in the dollar index. The yellow metal retreated from its session high of $1333.20 and settled with a 0.8% loss. Still, gold gained 6.6% in February on soft economic data and political unrest in Ukraine.

· May silver fell $0.13 to $21.22/oz

Silver also slipped into the red after brushing a session high of $21.42 at floor trade open. Prices sold off further heading into the close, leaving silver to settle 0.6% lower. Despite today's loss, the metal gained 10.8% in February.

· May copper fell 1 cent to $3.19/lbs

Treasuries

Yields End Near Lowest Levels in Three Weeks: 10-yr: -03/32..2.657%..USD/JPY: 101.76

The Week in Review

The Week in Review

Treasuries saw a mixed week as light selling took hold up front and a moderate bid developed at the long end. Click here to see an intraweek yields chart.

{kind=link}

Economic data was mixed as Case-Shiller 20-city Index (13.4% actual v. 13.6% expected), consumer confidence (78.1 actual v. 80.8 expected), GDP - Second Estimate (2.4% actual v. 2.6% expected), and pending home sales (0.1% actual v. 0.8% expected) missed while Chicago PMI (59.8 actual v. 56.0 expected), durable orders (-1.0% actual v. -1.1% expected), Michigan Sentiment - Final (81.6 actual v. 81.5 expected), and new home sales (468K actual v. 400K expected) beat.

This week's auctions were strong.

Tuesday's solid $32 bln 2y note auction drew 0.340% and a strong 3.60x bid/cover. A strong indirect takedown (34.3%) helped offset the slightly disappointing direct bid (19.2%).

Wednesday's $35 bln 5y note auction drew 1.530% and a strong 2.98x bid/cover (12-auction average 2.62x). A 50.6% indirect bid helped offset the light 9.1% direct takedown.

Thursday's $29 bln 7y note auction drew 2.105% and solid 2.72x bid/cover as a strong direct takedown (24.6%) provided support to the in-line indirect bid (41.1%). Primary dealers ended up with just 34.3% of the supply.

Fed Chair Janet Yellen took her semi-annual testimony to the Senate and suggested it is still too early to determine how much of an impact the winter weather is having on the data.

This week's bid pushed longer dated yields down to their lowest levels in three weeks.

The 30y shed -10bps over the course of the week, ending @ 3.592%. Traders will be watching support in the 3.550%/3.600% area over the coming days with a breaking dropping action to levels last seen in July.

This week's action in the 10y (-7bps @ 2.658%) dropped the benchmark yield to its own three-week low. Action has probed the 200 dma in recent days, but remains in search of its first close below the mark since the beginning of May, when the Fed first began talk of trimming its QE program.

The 5y ended the week little changed @ 1.511%. Action throughout the month of February has been confined to a tight 10bp range between 1.450%/1.550%.

Up front, the 2y edged up +1bp to 0.325%. Most of the action during February took place between 0.300%/0.340%.

A flatter curve took hold as the 2-10-yr spread narrowed to 233.5bps.

The Week Ahead

Monday's data is heavy as personal income, personal spending, PCE Prices - Core (8:30), ISM Index, construction spending (10), and auto/truck sales (14) are due out.

There is no data on Tuesday. The Senate Banking Committee will hold hearings on the nominations of Stanley Fischer, Jerome Powell, and Lael Brainard to the Fed's Board of Governors (10). Richmond's Lacker will give an "Update From the Fed" (16:15).

Data picks back up on Wednesday with the release of the weekly MBA Mortgage Index (7), ADP Employment Change (8:15), ISM Services (10), and the Fed's Beige Book (14). Dallas' Fisher will take place in a discussion in Mexico City (19:00) and SF's Williams will speak on the purpose of the Federal Reserve (20:30).

Thursday will see Challenger Job Cuts (7:30), initial and continuing claims, productivity-rev., unit labor costs-rev. (8:30), and factory orders (10). New York's Dudley takes part in a discussion with Dow Jones and the Wall Street Journal (8:15) before Philly's Plosser speaks in London on "Perspectives on the Economy and Monetary Policy" (13) and ATL's Lockhart gives his economic outlook (18).

Friday's data is the most anticipated of the week as nonfarm payrolls, nonfarm private payrolls, unemployment rate, hourly earnings, average workweek, trade balance (8:30), and consumer credit (15) are released. New York's Dudley discusses local economic conditions (12 noon).

On other news....

News

Amazon.com (AMZN) in talks to music labels about streaming service, according to reports

Freeport-McMoRan (FCX) discloses its Indonesian unit, PT-FI, may be required to declare force majeure

Gap's (GPS) Old Navy opens its first store in Mainland China

Goldman Sachs (GS): In 10-K filing sees possible aggregate loss to be approx $3.6 bln in excess of the aggregate reserves as off Dec 31; firm projected possible loss in excess of reserves of $4.0 bln at the end of Q3

IBM (IBM) has begun cutting US jobs as part of restructuring, according to reports

JosABank (JOSB) rejected $63.50 per share tender offer; agrees to meet with the Men's Warehouse (MW) - willing to consider a higher price

Mattel (MAT) and MEGA Brands announce definitive agreement for Mattel's acquisition, through a wholly-owned subsidiary of Mattel, of MEGA Brands for $460 mln

Noble Corp (NE) provides update on the status of drilling rig in Brazil; 77 non-essential personnel were evacuated from the rig without injuries, and no pollution has been reported

PepsiCo (PEP) Director Cook in letter to activist Nelson Peltz: Board and mgmt are comfortable and in complete alignment in rejecting your proposal

Perrigo (PRGO) acquires a basket of value-brand OTC products sold in Australia and New Zealand from Aspen Global for $51 mln in cash

Currencies

Dollar Hammered to Lowest Levels of 2014: 10-yr: -07/32..2.668%..USD/JPY: 102.02..EUR/USD: 1.3810

The Dollar Index presses its worst levels of 2014 as action probes the 79.80 area. Click here to see a daily Dollar Index chart.

{kind=link}

This level will be watched closely in the days ahead with a breakdown setting up a test of the key 79.00/79.20 region.

EURUSD is +100 pips @ 1.3810 and is threatening its best close since November 2011. The single currency is holding on its 2014 highs after this morning's eurozone Flash CPI reading printed a hotter than expected 0.8% YoY (0.7% YoY expected), causing some to scale back their calls for a European Central Bank-type QE program. Italian and Spanish Manufacturing PMI will released Monday.

GBPUSD is +55 pips @ 1.6740 as trade remains on track to end at its best level since November 2009. Today's advance has sterling higher for the fourth time in five sessions despite the lack of news and data out of the UK as trade has been dragged higher by the strength of the euro. Britain's Manufacturing PMI and net lending to individuals are set for release on Monday.

USDCHF is -80 pips @ .8800 as trade presses its worst levels since November 2011. Many traders continue to look elsewhere for opportunity as action is a derivative of the euro thanks to the Swiss National Bank peg. Swiss data is limited to SVME PMI.

USDJPY is -10 pips @ 102.00 as action hovers little changed. The pair slumped to nearly 101.50 in overnight trade in response to a hot Tokyo Core CPI number, but action was able to hold the 100 dma (101.83), which has provided help during the month of February. Many participants are waiting for a breakout from the 101.50/102.50 range that has been in place throughout February before getting involved. Japanese data is limited to capital spending.

AUDUSD is -35 pips @ .8925 as trade presses session lows. Support in the .8900/.8950 area, which has held up for the entire month of February, is under close watch as action tests its lowest levels of the month. ANZ Job Advertisements and company operating profits are due out Sunday. China's Manufacturing PMI will cross the wires tonight while Non-Manufacturing PMI and HSBC Final Manufacturing PMI are due out Sunday evening.

USDCAD is -70 pips @ 1.1050 as trade flushes to its lowest levels in one and a half weeks. Today's selling developed despite the disappointing Canadian GDP number (-0.5% MoM actual v. -0.2% MoM expected), and has trade testing key support in the area. A breakdown puts 1.0950 in the crosshairs. Canada's Raw Materials Price Index will be released Monday.

Weekly Analysis

Week 1

Technical Updates

{kind=link}

{kind=link}

Briefing's Commentaries

Week in Review: S&P 500 Registers Fresh Record Close

On Monday, the stock market kicked off the new trading week on an upbeat note, sending the S&P 500 (+0.6%) to a fresh nominal intraday record high of 1858.71. Despite the rally, selling during the final hour kept the benchmark index from finishing the session above its 2013 closing high of 1848.36. Although the catalyst for the buying rush could be debated, some attributed the bullish tone to the resilience of the S&P 500 futures in the face of some disappointing economic data and market performance in China. To clarify, a bearish catalyst was there for the taking, but it wasn't taken. Once the U.S. stock market started with a bullish bias, a fear of missing out on further upside helped fuel some renewed buying interest following Friday's lackluster session. Seven of ten sectors posted gains with energy (+1.5%) ending in the lead. The sector seized the lead at the open and maintained its outperformance throughout the session.

The stock market spun its wheels during the Tuesday session, ending essentially where it started. The S&P 500 shed 0.1% after spending the bulk of day within a striking distance of its flat line. Equity indices tried to build on the relative strength of the two consumer sectors, but the rally attempts were stifled by the daylong underperformance of the top three groups. Financials (-0.6%), health care (-0.2%), and technology (-0.3%) lagged from the opening bell and slumped to lows during the final hour of action. Since the three sectors account for more than 46.0% of the entire S&P 500, their underperformance acted as a headwind.

Equity indices finished the Wednesday session on a flat note after surrendering their modest intraday gains. More importantly, the S&P 500 was unable to register a fresh record closing high for the third day in a row. Stocks slipped from their opening levels, but the early weakness was erased in a flash when it was reported that new home sales in January surpassed estimates (468,000 versus Briefing.com consensus 400,000). The upbeat report sent stocks to new highs, but the S&P 500 ran into resistance just below the 1853 area, which the index was unable to penetrate throughout the afternoon. Eight of ten sectors ended in the red with energy (-0.6%) seeing the largest loss. However, the daylong underperformance of financials (-0.1%) was more notable as it marked the second day of relative weakness for the bellwether sector.

Stocks finished the Thursday session on an upbeat note with the S&P 500 settling above its 2013 closing high of 1848.36 after three unsuccessful attempts. Stocks climbed throughout the session despite starting the day on a cautious note. The early weakness could be traced to European markets, which were pressured by news of renewed tensions in the pro-Russian region of Crimea in Southern Ukraine. The developments weighed on European equities and contributed to a risk-off sentiment in the foreign exchange market where the yen strengthened notably against all major currencies. The dollar/yen pair fell as low as 101.70, which fueled worries about forced unwinds of yen-based carry trades. Those worries were calmed by a rebound that sent the currency pair to a session high of 102.20. Meanwhile, the stock market began the trading day on a flat note and continued climbing throughout the day. Participants heard from Fed Chair Janet Yellen, but Ms. Yellen struck a familiar tone during her appearance before the Senate Banking Committee.

On Monday, the stock market kicked off the new trading week on an upbeat note, sending the S&P 500 (+0.6%) to a fresh nominal intraday record high of 1858.71. Despite the rally, selling during the final hour kept the benchmark index from finishing the session above its 2013 closing high of 1848.36. Although the catalyst for the buying rush could be debated, some attributed the bullish tone to the resilience of the S&P 500 futures in the face of some disappointing economic data and market performance in China. To clarify, a bearish catalyst was there for the taking, but it wasn't taken. Once the U.S. stock market started with a bullish bias, a fear of missing out on further upside helped fuel some renewed buying interest following Friday's lackluster session. Seven of ten sectors posted gains with energy (+1.5%) ending in the lead. The sector seized the lead at the open and maintained its outperformance throughout the session.

The stock market spun its wheels during the Tuesday session, ending essentially where it started. The S&P 500 shed 0.1% after spending the bulk of day within a striking distance of its flat line. Equity indices tried to build on the relative strength of the two consumer sectors, but the rally attempts were stifled by the daylong underperformance of the top three groups. Financials (-0.6%), health care (-0.2%), and technology (-0.3%) lagged from the opening bell and slumped to lows during the final hour of action. Since the three sectors account for more than 46.0% of the entire S&P 500, their underperformance acted as a headwind.

Equity indices finished the Wednesday session on a flat note after surrendering their modest intraday gains. More importantly, the S&P 500 was unable to register a fresh record closing high for the third day in a row. Stocks slipped from their opening levels, but the early weakness was erased in a flash when it was reported that new home sales in January surpassed estimates (468,000 versus Briefing.com consensus 400,000). The upbeat report sent stocks to new highs, but the S&P 500 ran into resistance just below the 1853 area, which the index was unable to penetrate throughout the afternoon. Eight of ten sectors ended in the red with energy (-0.6%) seeing the largest loss. However, the daylong underperformance of financials (-0.1%) was more notable as it marked the second day of relative weakness for the bellwether sector.

Stocks finished the Thursday session on an upbeat note with the S&P 500 settling above its 2013 closing high of 1848.36 after three unsuccessful attempts. Stocks climbed throughout the session despite starting the day on a cautious note. The early weakness could be traced to European markets, which were pressured by news of renewed tensions in the pro-Russian region of Crimea in Southern Ukraine. The developments weighed on European equities and contributed to a risk-off sentiment in the foreign exchange market where the yen strengthened notably against all major currencies. The dollar/yen pair fell as low as 101.70, which fueled worries about forced unwinds of yen-based carry trades. Those worries were calmed by a rebound that sent the currency pair to a session high of 102.20. Meanwhile, the stock market began the trading day on a flat note and continued climbing throughout the day. Participants heard from Fed Chair Janet Yellen, but Ms. Yellen struck a familiar tone during her appearance before the Senate Banking Committee.

Next Week In View

Economic Commentaries

Economic Summary: Q4 GDP revised down, and below estimates; Michigan Sentiment in line with estimates; Chicago PMI beats expectations

Economic Data Summary:

Economic Data Summary:

Fourth Quarter GDP- Second Estimates 2.4% vs Briefing.com consensus of 2.6%; Third Quarter was 3.2%

Fourth Quarter GDP Deflator- Second Estimate 1.6% vs Briefing.com consensus of 1.3%; Third Quarter was 1.3%

. There was really nothing new in the GDP report that was a surprise from the most current monthly releases. The important takeaway is that real final sales, which were revised down to 2.3% from 2.8%, now show absolutely no breakout from trends that go back to Q1 2012. The "surge" in economic growth that led to strong 2014 economic forecasts did not actually happen. Looking at the details, downward revisions to retail sales in December led to a weaker consumption print.

February Chicago PMI 598.8 vs Briefing.com consensus of 56.0; January was 59.6

. This is another data point that suggests the weather is being used as a scapegoat during a cyclical down period. The increase in the PMI was primarily the result of a strong uptick in employment levels. The employment Index reversed a one-month contraction and increased to 59.3 from 49.2. N

February Michigan Sentiment 81.6 vs Briefing.com consensus of 81.5; January was 81.2

While the index moved in the opposite direction from the Conference Board's Consumer Confidence index, overall sentiment trends were relatively flat this month. Gains in equity prices offset slightly weaker employment conditions. Changes in gasoline prices and media reports likely had little effect on overall confidence values.

January Pending Home Sales 0.1% vs Briefing.com consensus of 0.8; December was -8.7%

Upcoming Economic Data:

January Personal Income due out Monday at 8:30 (Briefing.com consensus of ; December was 0.0%)

January Personal Spending due out Monday at 8:30 (Briefing.com consensus of ; December was 0.4%)

January PCE Prices - Core due out Monday at 8:30 (Briefing.com consensus of ; December was 0.01%)

February ISM Index due out Monday at 10:00 (Briefing.com consensus of ; January was )

January Construction Spending due out Monday at 10:00 (Briefing.com consensus of ; December was )

Upcoming Fed/Treasury Events:

Chicago Fed President Charlie Evans (dove, non voter) and Philadelphia Fed President Charles Plosser (voter, hawkish) to speak today at 13:30

Other International Events of Interest

Eurozone CPI rose 0.8% year-over-year (0.7% expected, 0.8% prior) while core CPI increased 1.0% year-over-year (0.8% consensus, 0.8% previous). Separately, the unemployment rate held steady at 12.0%, as expected.

Jason's Commentaries

The S&P500 broke into new high last Friday as the volumes surge to above 900m shares traded on the NYSE. At the market top, I have a good feeling that it is likely to reverse soon. It was a volatile session throughout the session. The market started with a strong bullish bias that can't sustain the high which lost most of its gains by midday. Over the weekend, Russia and Ukraine's conflict intensified which caused the Asia market to sunk. Futures were down by 0.8% already. i got a strong feeling that the market is likely to use it as an excuse to profit take.

Market Call: Down

Date: 3 Mar 2014

No comments:

Post a Comment