12 May 2014 AMC - Market shot up as small caps led rally.

Market Summary

European

Markets Closing Prices

European

markets are now closed; stock markets across Europe performed as follows:

·

UK's FTSE: + 0.6%

·

Germany's DAX: + 1.3%

·

France's CAC: + 0.4%

·

Spain's IBEX: + 0.8%

·

Portugal's PSI: + 1.0%

·

Italy's MIB Index: + 0.5%

·

Irish Ovrl Index: + 0.3%

·

Greece ATHEX Composite: -2.3%

Before Market Opens

S&P futures vs fair value:

+6.00. Nasdaq futures vs fair value: +16.00.

The S&P 500 futures trade six points above fair value.

Markets across Asia ended the Monday session on a mixed note. Indices in China outperformed in reaction to weekend reports suggesting Beijing may look to ease limits on foreign investment in public companies. The reports seemed to take center stage as traders shrugged off comments from Chinese President Xi Jinping suggesting Beijing needs to adjust to a ‘new normal' or slower growth.

The S&P 500 futures trade six points above fair value.

Markets across Asia ended the Monday session on a mixed note. Indices in China outperformed in reaction to weekend reports suggesting Beijing may look to ease limits on foreign investment in public companies. The reports seemed to take center stage as traders shrugged off comments from Chinese President Xi Jinping suggesting Beijing needs to adjust to a ‘new normal' or slower growth.

·

In economic data:

o Chinese new loans grew by CNY775 billion

(expected CNY840 billion).

o Japan's fiscal current account surplus (JPY789.9

billion) was the smallest in nearly 30 years, while the seasonally adjusted

current account deficit widened to JPY780 billion from JPY40 billion (deficit

of JPY540 billion expected).

o Australia's NAB Business Confidence ticked up to

6 from 4.

------

·

Japan's Nikkei shed 0.4%, holding near eight-month lows.

Olympus (+4.8%) outperformed following its upbeat quarterly report.

·

Hong

Kong's Hang Seng gained

1.8%, closing on its 50-day moving average. Internet gaming company Tencent

Holdings was the top performer, up 5.3%.

·

China's Shanghai Composite rallied 2.1%, ending at its

best level in three weeks. Commodity-related names saw the biggest boost from

Beijing's reported action as Yanzhou Coal Mining and Jiangxi Copper gained 10%

and 6.87%, respectively.

Major European indices trade higher

across the board with Germany's DAX (+0.9%) in the lead. On Sunday, Ukraine's

regions of Donetsk and Lugansk voted in favor of independence in referendums

that have not been recognized by the European Union or the U.S. In response,

the EU has placed sanctions on two Crimean companies and 13 Russian

individuals. Economic data was limited to Swiss Retail Sales, which rose 3.0%

year-over-year (expected 2.3%, previous 1.2%).

·

In

France, the CAC is higher by

0.1%. Industrial names Alston and Schneider Electric outperform with respective

gains of 2.9% and 1.8%. On the downside, REIT Unibail-Rodamco lags with a loss

of 4.1%.

·

Great

Britain's FTSE trades up 0.3% amid

strength in miners. Antofagasta, BHP Billiton, Fresnillo, and Rio Tinto hold

gains between 2.4% and 4.0%.

·

Germany's DAX sports an advance of 0.9% as producers of

basic materials outperform. K+S, ThyssenKrupp, and Lanxess are up between 1.2%

and 1.9%. Commerzbank is the weakest performer, down 2.3%.

U.S. Equities

·

Futures press their

overnight highs as traders ready for the opening bell

·

Friday's bid lifted the

DJIA to a record-high finish while the S&P 500 ended just 0.7% off its own

record peak

·

The Nasdaq remains more

than 7% off its best level in more than 14 years

·

The VIX (12.92) holds

near its lowest levels since January

o S&P Futures +7 @ 1881

o Dow Futures +54 @ 16,581

o Nasdaq Futures +19 @ 3567

Asia

·

Markets ended mixed

across Asia.

·

Reports out this past

weekend suggested Beijing may look to ease limits on foreign investment in

public companies. Those reports seem to take center stage as traders shrugged

off comments from Chinese President Xi Jinping suggesting Beijing needs to

adjust to a ‘new normal' or slower growth

·

Chinese new loans grew

by CNY775 bln (CNY840 bln expected)

·

Japan's fiscal current

account surplus (JPY789.9 bln) was the smallest in nearly 30 years

·

Australia's NAB Business

Confidence ticked up to 6 (4 previous).

·

Japan's Nikkei (-0.4%)

held near eight-month lows

·

Hong Kong's Hang Seng

(+1.8%) closed on its 50 dma

·

China's Shanghai

Composite (+2.1%) settled at its best level in three weeks

·

India's Sensex (+2.4%)

rallied to a record high as traders continued to price in the possibility the

opposition Bharatiya Janta Party would win the election

·

Australia's ASX (-0.2%)

slipped amid a quiet trade

·

Vietnam's Ho Chi Minh

Index (-4.7%) saw notable weakness as the recent tension with China weighed

Market Internals

Market Internals -Technical-

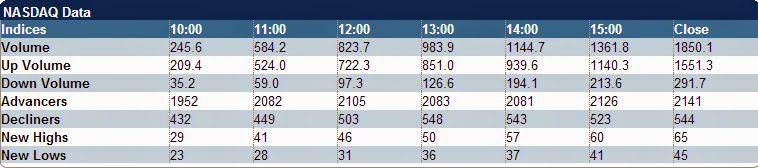

The Nasdaq closed up 72 (+1.77%) at 4144, the S&P 500 closed up 18 (+0.97%) at 1897, and the Dow closed up 112 (+0.68%) at 16695. Action came on below average volume (NYSE 626 mln vs. avg. of 719; NASDAQ 1731 mln vs. avg. of 1990), with advancers outpacing decliners (NYSE 2466/672, NASDAQ 2141/544) and new highs outpacing new lows (NYSE 165/14, NASDAQ 65/45).

Relative Strength:

Copper Miners-COPX +3.78%, Biotechnology-XBI +3.46%, Internet Composite-FDN +3.26%, India-INP +3.18%, Steel-SLX +2.98%, Coffee-JO +2.93%, Hong Kong-EWH +2.34%, China 25 Index-FXI +2.14%, Peru-EPU +2.05%, Indonesia-IDX +1.95%.

Relative Weakness:

Volatility-VXX -2.98%, Natural Gas-UNG -2.39%, Greece-GREK -1.71%, Cotton-BAL -1.6%, Grains-JJG -1.55%, Corn-CORN -1.11%, Brazilian Real-BZF -0.47%, Japanese Yen-FXY -0.32%, Swiss Franc-FXF -0.16%, Chinese Yuan-CYB -0.16%.

Leaders and Laggards

Technical Updates

Briefing's Commentaries

Closing Market Summary: Small Caps

Lead Stocks Higher

The stock market kicked off the new trading week on an upbeat note with small caps leading the advance after showing relative weakness last week. The Russell 2000 surged 2.3%, while the S&P 500 gained 1.0%. Even though the benchmark index posted a slimmer gain than the Russell 2000, it still managed to register a fresh closing record high at 1,896.65. Similarly, the Dow Jones Industrial Average (+0.7%) also settled at a new record high.

Small caps faced some heavy selling last week, while indices with a significant concentration of large cap listings were able to withstand the pressure. Today, however, the areas that struggled last week displayed relative strength, while the Dow and S&P 500 posted more modest gains.

Eight of ten sectors finished in the green with a clear bias towards cyclical groups as consumer discretionary (+1.3%), financials (+1.0%), industrials (+1.5%), materials (+1.3%), and technology (+1.5%) all posted gains of 1.0% or more, while the energy sector (+0.6%) was the only laggard among cyclical sectors.

The largest S&P 500 sector—technology—finished in the lead thanks to a boost from high-growth names like Facebook (FB 59.83, +2.59), LinkedIn (LNKD 152.28, +3.59), and Yelp (YELP 56.60, +2.38); however, it is worth pointing out that other areas of the sector also had a strong showing. Top sector members Apple (AAPL 592.83, +7.29) and Microsoft (MSFT 39.97, +0.43) both gained near 1.1%, while the broad strength among chipmakers sent the PHLX Semiconductor Index higher by 1.8%.

Elsewhere, the discretionary sector also received a measure of support from momentum names, but retailers and homebuilders were not far behind. The SPDR S&P Retail ETF (XRT 84.88, +1.62) and iShares Dow Jones US Home Construction ETF (ITB 23.70, +0.49) posted gains close to 2.0% apiece.

With nearly all cyclical sectors finishing ahead of the broader market, the only soft spots were found on the countercyclical side. The health care sector (+1.0%) ended ahead of the broader market, while consumer staples (+0.1%), telecom services (-0.2%), and utilities (-1.0%) lagged.

Treasuries retreated throughout the session, ending just above their lows. The benchmark 10-yr yield rose two basis points to 2.65%.

Participation was well below average as less than 630 million shares changed hands at the NYSE.

Also of note, Ukraine's regions of Donetsk and Lugansk have declared independence after Sunday referendums showed overwhelming support for breaking away from Ukraine. Following yesterday's vote, the council of Donetsk has petitioned for accession to the Russian Federation.

Economic data was limited to the Treasury budget, which posted a surplus of $106.90 billion in April 2014, down from a surplus of $112.90 billion in April 2013. The Treasury data are not seasonally adjusted and the April surplus cannot be compared with the results from March. The Briefing.com consensus expected a budget surplus of $114.00 billion. The Congressional Budget Office released their monthly budget preview last week and predicted a surplus of $114.00 billion. The market is well aware of the CBO's forecast and generally does not react to the actual budget release.

Tomorrow, the Retail Sales report for April (Briefing.com consensus +0.3%) and April Import/Export Prices will be released at 8:30 ET, while the Business Inventories report for March (Briefing.com consensus +0.4%) will cross the wires at 10:00 ET.

The stock market kicked off the new trading week on an upbeat note with small caps leading the advance after showing relative weakness last week. The Russell 2000 surged 2.3%, while the S&P 500 gained 1.0%. Even though the benchmark index posted a slimmer gain than the Russell 2000, it still managed to register a fresh closing record high at 1,896.65. Similarly, the Dow Jones Industrial Average (+0.7%) also settled at a new record high.

Small caps faced some heavy selling last week, while indices with a significant concentration of large cap listings were able to withstand the pressure. Today, however, the areas that struggled last week displayed relative strength, while the Dow and S&P 500 posted more modest gains.

Eight of ten sectors finished in the green with a clear bias towards cyclical groups as consumer discretionary (+1.3%), financials (+1.0%), industrials (+1.5%), materials (+1.3%), and technology (+1.5%) all posted gains of 1.0% or more, while the energy sector (+0.6%) was the only laggard among cyclical sectors.

The largest S&P 500 sector—technology—finished in the lead thanks to a boost from high-growth names like Facebook (FB 59.83, +2.59), LinkedIn (LNKD 152.28, +3.59), and Yelp (YELP 56.60, +2.38); however, it is worth pointing out that other areas of the sector also had a strong showing. Top sector members Apple (AAPL 592.83, +7.29) and Microsoft (MSFT 39.97, +0.43) both gained near 1.1%, while the broad strength among chipmakers sent the PHLX Semiconductor Index higher by 1.8%.

Elsewhere, the discretionary sector also received a measure of support from momentum names, but retailers and homebuilders were not far behind. The SPDR S&P Retail ETF (XRT 84.88, +1.62) and iShares Dow Jones US Home Construction ETF (ITB 23.70, +0.49) posted gains close to 2.0% apiece.

With nearly all cyclical sectors finishing ahead of the broader market, the only soft spots were found on the countercyclical side. The health care sector (+1.0%) ended ahead of the broader market, while consumer staples (+0.1%), telecom services (-0.2%), and utilities (-1.0%) lagged.

Treasuries retreated throughout the session, ending just above their lows. The benchmark 10-yr yield rose two basis points to 2.65%.

Participation was well below average as less than 630 million shares changed hands at the NYSE.

Also of note, Ukraine's regions of Donetsk and Lugansk have declared independence after Sunday referendums showed overwhelming support for breaking away from Ukraine. Following yesterday's vote, the council of Donetsk has petitioned for accession to the Russian Federation.

Economic data was limited to the Treasury budget, which posted a surplus of $106.90 billion in April 2014, down from a surplus of $112.90 billion in April 2013. The Treasury data are not seasonally adjusted and the April surplus cannot be compared with the results from March. The Briefing.com consensus expected a budget surplus of $114.00 billion. The Congressional Budget Office released their monthly budget preview last week and predicted a surplus of $114.00 billion. The market is well aware of the CBO's forecast and generally does not react to the actual budget release.

Tomorrow, the Retail Sales report for April (Briefing.com consensus +0.3%) and April Import/Export Prices will be released at 8:30 ET, while the Business Inventories report for March (Briefing.com consensus +0.4%) will cross the wires at 10:00 ET.

·

S&P 500 +2.6%

YTD

·

Dow Jones Industrial

Average +0.7% YTD

·

Nasdaq Composite -0.8%

YTD

·

Russell 2000 -2.5% YTD

Commodities

COMEX

Metals Closing Prices

June gold rose $8.30 to $1295.90/oz

·

Gold traded higher today

as it gained support on renewed tension in Ukraine. On Sunday, Ukraine's

regions of Donetsk and Lugansk held independence referendums, but neither Kiev,

nor the international community has recognized the votes as legitimate. In

response, the EU has placed sanctions on two Crimean companies and 13 Russian

individuals. The yellow metal advanced to a session high of $1304.50 in early

morning action but retreated back below the $1300 level as the session progressed.

It eventually settled with a 0.6% gain.

July silver rose $0.44 to $19.55/oz

·

Silver also spent floor

trade in positive territory, trading as high as $19.67 in early morning action.

It then consolidated near the $19.60 level and settled with a 2.3% gain.

July

copper rose 7 cents to $3.15/lbs

CBOT

Agriculture and Ethanol/ICE Sugar Closing Prices

·

July

corn fell 9 cents to

$4.99/bushel

·

July

wheat fell 8 cents to

$7.15/bushel

·

July

soybeans fell 21 cents to

$14.65/bushel

·

June

ethanol fell 2 cents to

$2.14/gallon

·

July

sugar (#16 (U.S.)) fell

0.12 of a penny to 24.43 cents/lbs

NYMEX

Energy Closing Prices

June crude oil rose $0.58 to $100.60/barrel

·

Crude oil chopped around

in positive territory, getting a boost from renewed tension in Ukraine. The EU

has placed sanctions on two Crimean companies and 13 Russian individuals

following independence referendums being held over the weekend in Urkaine's

regions of Donetsk and Lugansk. Neither Kiev, nor the international community

has recognized the votes as legitimate. The energy component rose as high as

$100.97 in morning action and settled with a 0.6% gain.

June natural gas fell 10 cents to $4.43/MMBtu

·

Natural gas, on the

other hand, fell deeper into negative territory after pulling back from its

session high of $4.50 set moments after floor trade opened. Unable to find

buying support, it settled at its session low, or 2.2% lower

June heating oil rose 1 cent to $2.92/gallon

June

RBOB rose 3 cents to $2.92/gallonTreasuries

Treasuries Book Modest Losses:

10-yr: -07/32..2.653%..USD/JPY: 102.13..EUR/USD: 1.3757

·

Treasuries finished with

modest losses amid a sleepy session. Click here to see an intraday

yields chart.

·

The complex saw light

overnight selling persist into U.S. trade as equity markets sported strong

gains from the get go.

·

A lack of

tradable news and data had Treasuries under pressure throughout the

session with the complex marking its lows in response to the small than

anticipated Treasury budget ($106.9 bln actual v. $114 bln expected).

·

Today's weakness weighed

heaviest on the belly as yields there climbed as much as +3.3bps. The 5y ended

@ 1.658% as action bounced off the 100 dma and finished on the 50 dma.

·

The 10y climbed to

2.656%, ending just shy of the 2.670% pivot. The ability to retake that level

would put the upper end of the 2.600%/2.800% range in play.

·

The 30y saw slight

outperformance, adding +32.5bps to 3.492%. Traders continue to track resistance

in the 3.500%/3.550% area that has been in place over the past month.

·

A

slightly flatter curve developed as the 5-30-yr spread narrowed to 183.5bps.

·

Precious metals firmed

as gold added +$9 to $1297 and silver climbed +$0.44 to $19.56.

·

Data: Retail sales, import/export prices (8:30), and

business inventories (10).

·

Fed

Speak: ATL's Lockhart will be

in Saudi Arabia to discuss the U.S. economy (0:30). Richmond's Lacker will give

opening remarks at the Richmond Fed's 2014 Credit Markets Symposium (10:30).

On other news....

Currencies

Dollar Drifts Little Changed: 10-yr:

-10/32..2.663%..USD/JPY: 102.15..EUR/USD: 1.3755

·

The Dollar Index has

clawed back its early losses and now trades flat near 79.90. Click here to see a daily Dollar

Index chart.

·

Many traders continue to

monitor resistance in the 80.00 area, which has held up over the past

month.

·

EURUSD is +5 pips @ 1.3755 as trade has spent

the entire U.S. session in a 20 pip range. The small bid has the single

currency on track to end its three-day skid as buyers have emerged at the 100

dma amid a lack of news and data from the region. Eurozone out tomorrow data

includes ZEW Economic Sentiment and German ZEW Economic Sentiment.

·

GBPUSD is +15 pips @ 1.6870 amid a lackluster trade.

Sterling found early buyers at the open, and has not looked back action has

spent the entire day in positive territory. The 1.6800 area provides near-term

support while any move above 1.7000 would be the best since August 2009.

British data is limited to tonight's release of the BRC Retail Sales Monitor.

·

USDCHF is +10 pips @ .8875 as buyers remain in control

for a fourth session despite today's strong Swiss retail sales print.

Resistance in the .8900/.8925 area that is helped by the 100 dma is all the

stands in the way of a retest of .9000 and the 200 dma.

·

USDJPY is +30 pips @ 102.15 as trade looks likely to

put in its best close in a week after the fiscal 2013 current account

surplus was the smallest in almost 30 years. Traders remain fixated on

the 102.50 pivot as a breakout puts 103.50 in play.

·

AUDUSD is +5 pips @ .9365 as trade checks up

near three-week highs. The hard currency saw an early test of the .9400

level, but has failed to see a follow through bid as traders err on the side of

caution following today's comments from Chinese President Xi Jinping.

Mr. Xi suggested China must face a ‘new normal' of slower growth. Australia's

Home Price Index and home loans will cross the wires this evening before the

release of China's industrial production and fixed asset investment.

·

USDCAD is -10 pips @ 1.0890 as a sleepy session

drifts towards the close. Action has been limited to a 30 pip range amid the

lack of news and data from both Canada and the U.S.

Next Week In View

Economic Commentaries

Economic Summary: Treasury April

Surplus less than expected; Retail sales tomorrow at 8:30

Economic Data Summary:

Economic Data Summary:

·

April

Treasury Budget $106.2 bln vs Briefing.com consensus of $114.0 bln; March was

-$112.9 bln

o The Congressional Budget Office released their

monthly budget preview last week and predicted a surplus of $114.0 bln. The

market is well aware of the CBO's forecast and generally does not react to the

actual budget release. Total revenues increased from $406.7 bln in April 2013

to $414.2 bln in April 2014, a gain of $7.5 bln. Total outlays increased to

$307.4 bln in April 2014 from $293.8 bln, an increase of $13.5 bln.

Year-to-date, the deficit is $306.4 bln, $181.2 bln less than FY 2013.

Upcoming Economic Data:

·

April

Retail Sales due out Tuesday at 8:30 (Briefing.com consensus of 0.3%; March was

1.2%)

·

April

Retail Sales Ex-Auto due out Tuesday at 8:30 (Briefing.com consensus of 0.6%;

March was 0.7%)

·

April Export Prices

Ex-Ag due out Tuesday at 8:30 (March was 0.5%)

·

April Import Prices

Ex-Oil due out Tuesday at 8:30 (March was 0.3%)

·

March Business

Inventories due out Tuesday at 10:00 (Briefing.com consensus of 0.4%; February

was 0.4%)

Upcoming Fed/Treasury Events:

·

Atlanta Fed President

Dennis Lockhart (not a voting FOMC member, moderate) to speak tomorrow at 12:30

AM

·

Richmond Fed President

Jeff Lacker (not a voting FOMC member, hawkish) to speak tomorrow at 10:30

Other International Events of

Interest

·

Reports out this past

weekend suggested Beijing may look to ease limits on foreign investment in

public companies. Those reports seem to take center stage as traders shrugged

off comments from Chinese President Xi Jinping suggesting Beijing needs to adjust

to a ‘new normal' or slower growth

·

Japan's fiscal current

account surplus (JPY789.9 bln) was the smallest in nearly 30 years

Jason's Commentaries

It was a very sudden rally that got Dow and S&P500 very near their all time high once again. Nasdaq and Russells were the main moving factor in the market last night, however on low volumes of 640.7m shares traded on the NYSE. The market rallied right at the start of the trading session and held up high throughout the session. Surprisingly, There is one sector lagging amidst such bullish day. The strongest sector last night was Industrials and Tech, gaining 1.49% and 1.35% respectively. Too many big names gaining more than 2% last night. However, I believe the Tech is likely to face some resistance today, likely to drag down the market.

Market Call: FLAT to downside

Date: 13 May 2014

No comments:

Post a Comment