Market Summary

European Markets Closing Prices

European

markets are now closed; stock markets across Europe performed as follows:

·

UK's

FTSE: -1.0%

·

Germany's

DAX: -0.2%

·

France's

CAC: -0.3%

·

Spain's

IBEX: -1.0%

·

Portugal's

PSI: -1.3%

·

Italy's

MIB Index: -1.6%

·

Irish

Ovrl Index: -0.3%

·

Greece

ASE General Index: + 0.0%

Before Market Opens

S&P futures vs fair value: -8.70.

Nasdaq futures vs fair value: -14.00.

The S&P 500 futures trade nine points below fair value.

Markets were weak across much of Asia. Pro-democracy protests in Hong Kong grew violent, contributing to a sharp decline in the Hang Seng (-2.6%). Elsewhere, Moody's lowered Japan's credit rating to A1 from Aa3 after markets were closed.

The S&P 500 futures trade nine points below fair value.

Markets were weak across much of Asia. Pro-democracy protests in Hong Kong grew violent, contributing to a sharp decline in the Hang Seng (-2.6%). Elsewhere, Moody's lowered Japan's credit rating to A1 from Aa3 after markets were closed.

·

Economic

data was plentiful:

o China's Manufacturing PMI slipped to 50.3 from

50.8 (expected 50.5) while HSBC Manufacturing PMI held at 50.0, as

expected.

o Japan's Manufacturing PMI ticked down to 52.0

from 52.1 (consensus 52.1)

o Hong Kong's Retail Sales rose 1.4%

year-over-year (expected 0.3%; previous 4.8%)

o India's HSBC Markit Manufacturing PMI rose to

53.3 from 51.6 (expected 51.5)

o Australia's AIG Manufacturing Index rose to 50.1

from 49.4

o New Zealand's Terms of Trade Index fell 4.4%

quarter-over-quarter (expected -4.3%; last 0.1%)

o South Korea's trade surplus narrowed to $5.61

billion from $7.40 billion (expected surplus of $6.20 billion) as imports fell

4.0% (expected -2.2%) and exports dropped 1.9% (consensus 1.8%)

o Indonesia's Core Inflation increased to 4.21%

from 4.02% (expected 4.46%)

------

·

Japan's Nikkei rallied 0.8% to its best level in seven

years. Automakers gained as Toyota Motor and Honda Motor advanced 1.6% and

1.1%, respectively.

·

Hong

Kong's Hang Seng

tumbled 2.6% to a one-week low and closed on the 200-day average. Energy names

lagged as Kunlun Energy and CNOOC both lost 5.5%.

·

China's Shanghai Composite shed 0.1% to end its

seven-day winning streak. Hainan Airlines, outperformed, climbing the limit,

10.0%, as crude oil probed $64 per barrel in overnight trade.

·

India's Sensex slid 0.5% from all-time highs. Commodity

plays were pressured as Oil & Natural Gas Co and Hindalco Industries gave

up 3.9% and 3.8%, respectively.

Major European indices trade lower

across the board with Italy's MIB (-1.6%) pacing the slide. Elsewhere, the

Swiss gold referendum failed with 77% of voters opposing a measure that would

require the Swiss National Bank to hold 20.0% of its balance sheet in gold.

·

Participants

received several data points:

o Eurozone Manufacturing PMI ticked down to 50.1

from 50.4 (expected 50.4)

o Germany's Manufacturing PMI fell to 49.5 from

50.0 (expected 50.0)

o French Manufacturing PMI rose to 48.4 from 47.6

(consensus 47.6)

o Italy's Manufacturing PMI held at 49.0 (expected

49.5). Separately, Q3 GDP was left unrevised at -0.1%, but the year-over-year

reading was revised down to -0.5% from -0.4% (expected -0.4%)

o Spain's Manufacturing PMI jumped to 54.7 from

52.6 (expected 53.1)

------

·

Germany's DAX is lower by 0.4% amid weakness in

financials. Commerzbank and Deutsche Bank are both down near 2.0%. Utilities

lead with E.On and RWE up 4.6% and 1.8%, respectively, after E.On announced its

restructuring plan.

·

In France, the CAC trades down 0.4%. Financials also lag

with AXA, Credit Agricole, and Societe Generale down between 1.8% and 2.7%.

Consumer names outperform with Valeo and Pernod Ricard up 0.5% and 0.2%, respectively.

·

Great

Britain's FTSE has

given up 1.0% with Vodafone leading the decline. The stock has given up 4.1% in

reaction to reports suggesting the company is looking into potential

acquisitions.

·

Italy's MIB holds a loss of 1.6%. Bank shares lag with

Banco Popolare, UnipolSai, UBI Banca, and Unicredit down between 3.1% and 4.0%.

U.S. Equities

·

Futures

point to a heavy open

·

Retailers

will be in focus today as reports trickle in regarding the performance on

'Black Friday'

o S&P Futures -9 @ 2057

o Dow Futures -65 @ 17,747

o Nasdaq Futures -15 @ 4323

Asia

·

Markets

were weak across much of Asia

·

Pro-democracy

protests in Hong Kong grew violent, sending the Hang Seng (-2.6%) to a sharp

decline

·

China's

Manufacturing PMI (50.3 actual v. 50.5 expected, 50.8 previous) missed while

HSBC Final Manufacturing PMI (50.0) was in-line

·

Moody's

lowered Japan's credit rating to A1 from Aa3 after markets were closed

·

Australia's

company operating profits improved 0.5% QoQ (-1.2% QoQ expected)

·

India's

HSBC Manufacturing PMI climbed to 53.3 (51.6 previous)

·

Indonesia's

core inflation climbed to 4.21% YoY (4.02% YoY previous, 4.46% expected)

·

Japan's

Nikkei (+0.8%) rallied to its best level in seven years

·

Hong

Kong's Hang Seng (-2.6%) tumbled to a one-week low and closed on the 200 dma

·

China's

Shanghai Composite (-0.1%) ended its seven-day winning streak

·

India's

Sensex (-0.5%) slid off all-time highs

·

Australia's

ASX (-2.0%) tumbled to a seven-week low

Market Internals

Market Internals -Technical-

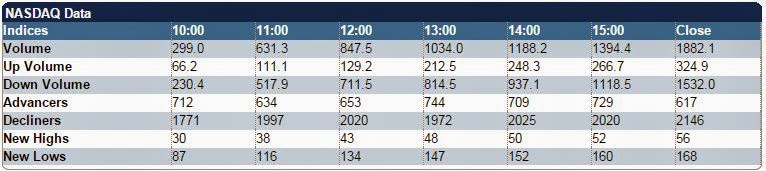

The Nasdaq closed down 64 (-1.34%) at 4727, the S&P 500 closed down 14 (-0.68%) at 2053, and the Dow closed down 51 (-0.29%) at 17777. Action came on mixed volume (NYSE 856 mln vs. avg. of 785; NASDAQ 1718 mln vs. avg. of 1803), with decliners outpacing advancers (NYSE 714/2478, NASDAQ 617/2146) and new lows outpacing new highs (NYSE 142/241, NASDAQ 56/168).

Relative Strength:

Junior Gold Miners-GDXJ +9.84%, Silver Miners-SIL +7%, Volatility-VXX +4.27%, Platinum-PPLT +3.3%, Oil-USO +2.87%, Canadian Dollar-FXC +0.94%, British Pound-FXB +0.77%, New Zealand-ENZL +0.72%, Poland-EPOL +0.63%, Brazilian Real-BZF +0.58%.

Relative Weakness:

MLP Index-AMJ -4.45%, Clean Energy-PBW -4.17%, Natural Gas-UNG -3.76%, Egypt-EGPT -3.55%, Copper Miners-COPX -3.52%, Columbia Index-GXG -3.26%, Rare Earths-REMX -3.25%, Latin America 40-ILF -3.25%, Malaysia-EWM -2.95%, BRICs-EEB -2.88%.

Leaders and Laggards

Technical Updates

Briefing's Commentaries

Closing Market Summary: Stocks Retreat

Amid Global Growth Concerns

The major averages began December on a lower note with relative weakness among cyclical sectors keeping the market under pressure throughout the day. The Nasdaq Composite (-1.3%) and Russell 2000 (-1.6%) paced the slide while the S&P 500 settled lower by 0.7% with eight sectors ending in the red.

Equities faced selling pressure from the opening bell after the overnight session reminded investors about persistent growth concerns around the globe. In Asia, China's HSBC Manufacturing PMI fell to an eight-month low (50.3; expected 50.5) while Japan's debt rating was lowered to A1 from Aa3 at Moody's. Making matters worse, Germany's Manufacturing PMI slid into contraction (49.5; expected 50.0) while the eurozone Manufacturing PMI narrowly avoided the same fate (50.1; expected 50.4).

Accordingly, the concerns about major economies kept cyclical sectors under pressure with five of six growth-sensitive groups ending behind the broader market. The industrial sector (-1.3%) slumped to the bottom of the leaderboard at the start and remained in that spot until the close. Transport stocks were largely responsible for the weakness with the Dow Jones Transportation Average ending lower by 2.7%.

Elsewhere among cyclical sectors, the top-weighted technology space (-1.1%) endured a late-morning plunge in the shares of Apple (AAPL 115.05, -3.88). The largest sector component was down as much 6.3% during the opening hour, but narrowed its loss to 3.3%. Chipmakers fared a bit better than Apple, but worse than the sector as evidenced by a 1.3% decline in the PHLX Semiconductor Index.

The energy sector (+0.8%) was the only cyclical group that finished ahead of the market thanks to a rebound in crude oil. The energy component rallied 4.1% to $69.02/bbl after marking an overnight low at $64.00/bbl. As for the energy sector, the group was underpinned by some of its main components like Chevron (CVX 111.73, +2.86) and ExxonMobil (XOM 92.35, +1.81). The two Dow components gained 2.6% and 2.0%, respectively, to help the price-weighted Dow (-0.3%) finish ahead of the broader market.

Over on the countercyclical side, the utilities sector (+0.2%) spent the bulk of the day in the green while other defensively-oriented sectors ended mixed. Health care (-0.2%) and consumer staples (-0.6%) settled ahead of the S&P 500 while the telecom services sector (-1.0%) lagged.

Treasuries notched their highs shortly after the opening bell and spent the remainder of the day in a steady retreat. The 10-yr yield climbed five basis points to 2.22%.

Today's participation was ahead of average with more than 850 million shares changing hands at the NYSE floor.

Economic data was limited to the ISM Index, which fell to 58.7 from 59.0 while the Briefing.com consensus expected a decline to 58.0. The Production Index fell to 64.4 from 64.8, which resulted from manufacturers delaying production until a later time. New orders improved as the related index increased to 66.0 from 65.8. Meanwhile, order backlogs increased to 55.0 from 53.0 in October.

Tomorrow, the Construction Spending report for October will be released at 10:00 ET (Briefing.com consensus 0.6%).

The major averages began December on a lower note with relative weakness among cyclical sectors keeping the market under pressure throughout the day. The Nasdaq Composite (-1.3%) and Russell 2000 (-1.6%) paced the slide while the S&P 500 settled lower by 0.7% with eight sectors ending in the red.

Equities faced selling pressure from the opening bell after the overnight session reminded investors about persistent growth concerns around the globe. In Asia, China's HSBC Manufacturing PMI fell to an eight-month low (50.3; expected 50.5) while Japan's debt rating was lowered to A1 from Aa3 at Moody's. Making matters worse, Germany's Manufacturing PMI slid into contraction (49.5; expected 50.0) while the eurozone Manufacturing PMI narrowly avoided the same fate (50.1; expected 50.4).

Accordingly, the concerns about major economies kept cyclical sectors under pressure with five of six growth-sensitive groups ending behind the broader market. The industrial sector (-1.3%) slumped to the bottom of the leaderboard at the start and remained in that spot until the close. Transport stocks were largely responsible for the weakness with the Dow Jones Transportation Average ending lower by 2.7%.

Elsewhere among cyclical sectors, the top-weighted technology space (-1.1%) endured a late-morning plunge in the shares of Apple (AAPL 115.05, -3.88). The largest sector component was down as much 6.3% during the opening hour, but narrowed its loss to 3.3%. Chipmakers fared a bit better than Apple, but worse than the sector as evidenced by a 1.3% decline in the PHLX Semiconductor Index.

The energy sector (+0.8%) was the only cyclical group that finished ahead of the market thanks to a rebound in crude oil. The energy component rallied 4.1% to $69.02/bbl after marking an overnight low at $64.00/bbl. As for the energy sector, the group was underpinned by some of its main components like Chevron (CVX 111.73, +2.86) and ExxonMobil (XOM 92.35, +1.81). The two Dow components gained 2.6% and 2.0%, respectively, to help the price-weighted Dow (-0.3%) finish ahead of the broader market.

Over on the countercyclical side, the utilities sector (+0.2%) spent the bulk of the day in the green while other defensively-oriented sectors ended mixed. Health care (-0.2%) and consumer staples (-0.6%) settled ahead of the S&P 500 while the telecom services sector (-1.0%) lagged.

Treasuries notched their highs shortly after the opening bell and spent the remainder of the day in a steady retreat. The 10-yr yield climbed five basis points to 2.22%.

Today's participation was ahead of average with more than 850 million shares changing hands at the NYSE floor.

Economic data was limited to the ISM Index, which fell to 58.7 from 59.0 while the Briefing.com consensus expected a decline to 58.0. The Production Index fell to 64.4 from 64.8, which resulted from manufacturers delaying production until a later time. New orders improved as the related index increased to 66.0 from 65.8. Meanwhile, order backlogs increased to 55.0 from 53.0 in October.

Tomorrow, the Construction Spending report for October will be released at 10:00 ET (Briefing.com consensus 0.6%).

·

Nasdaq

Composite +13.2% YTD

·

S&P

500 +11.1% YTD

·

Dow Jones

Industrial Average +7.2% YTD

·

Russell

2000 -0.7% YTD

Commodities

Closing Commodities: Oil Prices And

Precious Metals Surge; WTI Back Above $69/Barrel

·

Oil

prices surging higher today following the recent OPEC-driven plunge

·

Silver

and gold futures post big gains as well

·

Today,

Jan WTI crude fell as low as $63.72, but has since rallied back over $69/barrel

o Jan WTI crude rose $2.71 in pit trading to

$69.02/barrel

·

Brent

crude oil fell as low as $67.60/barrel, but has come back near $73/barrel and

is now at $73 in electronic trading

·

Jan gold

futures surged 4.3% to $1218.20/oz, while Mar silver soared 7.6% to $16.70/oz

·

Dec

copper rose 5 cents to $2.90/lb

Metals price action; silver surges almost 8%,

gold over +4%

·

Gold rose

$50.60 (or +4.3%) to $1218.20/oz

·

Silver

rose $1.18 (or +7.6%) to $16.70/oz

·

Copper

rose 5 cents to $2.90/lb

Agricultural price action

·

Corn

closed 1 cent lower at $3.76/bushel

·

Wheat

rose 29 cents (or +5%) to $6.07/bushel

·

Soybeans

rose 3 cents to $10.18/bushel

·

Ethanol

rose 1 cent to $1.74/gallon

·

Sugar #11

closed unchanged at 15.59 cents/gallon

Energy price action; WTI crude rises above

$69/barrel

·

Crude oil

rose $2.71 (or +4.1%) to $69.02/barrel

·

Natural

gas fell 9 cents to $4.01/MMBtu

·

Heating

oil rose 9 cents (or +4.2%) to $2.22/gallon

·

RBOB rose

4 cents to $1.88/gallon

Treasuries

Treasuries See First Loss in Seven

Sessions: 10Y: -16/32..2.219%..USD/JPY: 118.35..EUR/USD: 1.2475

·

Treasuries

ended on their lows as selling took hold for the first time in seven

days. Click here to see an intraday

yields chart.

·

Maturities

held small gains into the cash open as China's Manufacturing PMI missed

and Japan was downgraded at Moody's.

·

The

complex tested its best levels of the day into the ISM Index (58.7

actual v. 58.0 expected, 59.0 previous) beat, but began slipping off those

levels as traders digested the data.

·

Trade

would slip over the course of the day.

·

Up front,

the 2Y tacked on +0.4bps to 0.488%. Treasury bears are hoping to reclaim the

0.500% level as support there held throughout the month of November.

·

In the

belly, the 5Y added +1bp to 1.521%. Early buying tested minor support in the

1.450% area before seeing a significant bounce.

·

The 10Y

rallied +2.4bps to 2.218%. The benchmark yield tested the 2.150% area, a 50%

retracement of the move off the October 15 lows, before reversing.

·

Selling

at the long end ran the 30Y up +3.6 to 2.946%. The yield on the long bond

flirted with its lowest close since late-2012 before today's reversal.

·

A steeper

curve developed as the 2-10-yr spread widened to 173bps.

·

Precious

metals rallied sharply with gold up +$37 to $1213 and silver higher by +$0.96

to $16.52.

·

Data: Construction spending (10) and auto/truck

sales (14).

·

Fed Speak: Fed Vice Chair Stanley Fischer sits on a panel

at the 2014 Wall Street CEO Council Annual Meeting (8:10). Fed Chair Janet

Yellen makes opening remarks at the 2014 College Fed Challenge National Finals

(8:30). Fed Governor Brainard opens the Economic Growth and Regulatory

Paperwork Reduction Act Outreach Meeting (12). NY's Dudley appears at Lehman

College (15:30).

On other news....

Currencies

Dollar Dives Below 88.00: 10Y:

-14/32..2.215%..USD/JPY: 118.28..EUR/USD: 1.2477

·

The

Dollar Index lingers near session lows as trade consolidates near 87.80. Click here to see a daily Dollar

Index chart.

·

Today's

weakness has some traders turning their attention back towards 88.50 support.

·

EURUSD is +30 pips @ 1.2480 as trade holds just off the

highs. The single currency tested the key 1.2400 in early trade, but was bid

off the support level following the mixed Italian and Spanish Manufacturing PMI

data. Traders continue to look ahead to Thursday's ECB rate decision,

which has traders contemplating the announcement of a QE-type program. Spanish

unemployment change is due out tomorrow.

·

GBPUSD is +105 pips @ 1.5745 as trader recoups all of

Friday's losses and then some. Sterling probed the key 1.5600 level in

overnight action before finding support in response to the Manufacturing PMI

beat. Resistance near 1.5800 will be watched into tomorrow's Construction PMI

release.

·

USDCHF is flat @ .9640 after 78% voted ‘NO' in the gold

referendum. Traders are more interested in EURCHF, which has tacked

on 10 pips to 1.2030 and is on track to post its best close in three

weeks.

·

USDJPY is -30 pips @ 118.30 as action holds near

seven-year highs. The pair probed the 119.00 level after Moody's lowered

Japan's credit rating to A1 from Aa3, but slipped into the red as the news

was digested. Japanese data scheduled for tonight is limited to average cash

earnings.

·

AUDUSD is +10 pips @ .8505 after rallying sharply off

the overnight lows. The hard currency pressed to a low of .8415 after the disappointing

Chinese Manufacturing PMI number, but has seen steady buying

throughout the session. Australia's building approvals and current account

balance will be released ahead oftonight's Reserve Bank of Australia rate

decision.

·

USDCAD is -85 pips @ 1.1330 as trade gives up all of

Friday's gains. Early buying had the action testing the November highs as trade

probed 1.1450, but selling throughout the day now has the pair on the lows.

Support in the 1.1250 region is helped by the 50 dma.

Next Week In View

Economic Commentaries

Economic summary: November ISM better

than expected; Fed's Dudley and Fischer to speak intraday

Economic Data Summary:

Economic Data Summary:

·

November

ISM Index 58.7 vs Briefing.com consensus of 58.0; October was 59.0

o Nearly all of the regional Federal Reserve

manufacturing surveys showed accelerated manufacturing growth in November. The

slight pullback in the national index goes against those trends. Still,

manufacturing activities were stronger than consensus expectations and remains

close to Q1 2011 highs.

·

November

Markit Manufacturing PMI 54.8 vs 54.7 prelim and 55.9 in October

o While still expanding, the reading represents a

10 month low

·

Chinese

Manufacturing PMI for November: 50.3 vs. 50.5 Briefing.com Consensus; prior:

50.8

Upcoming Economic Data:

·

October

Construction Spending due out Tuesday at 10:00 (Briefing.com consensus of

+0.6%; was -0.4%)

·

November

Auto Sales due out at (Briefing.com consensus of ; was )

Upcoming Fed/Treasury Events:

·

William

Dudley (typically dovish) speaks at 12:15 PM

·

Vice

Chair Stanley Fischer speaks at 13:00 PM

Jason's Commentaries

It came in a little unexpected that the start of dec actually started in the red, especially with the broader market sell down. Apple sunk unexpectedly with a 3.25% drop which caused a huge lag in both S&P500 and Nasdaq Composite. The oil companies managed to gain some ground as oil managed to hit back $69. The discretionary are also affected as there are expectations that the Black Friday and Cyber Monday sales are going to be bad. With all these, it's actually causing a breakdown in the consolidation. I believe today it's likely to test the resistance level. If the test fails... we're going down =D

Market Call: FLAT to upside

Date: 2 Dec 2014

No comments:

Post a Comment