3 Dec 2014 AMC -Market ended slightly higher while ADP employment reports missed expectation.

Market Summary

European Markets Closing Prices

European

markets are now closed; stock markets across Europe performed as follows:

·

UK's

FTSE: -0.4%

·

Germany's

DAX: + 0.4%

·

France's

CAC: + 0.1%

·

Spain's

IBEX: + 1.2%

·

Portugal's

PSI: + 0.4%

·

Italy's

MIB Index: + 1.0%

·

Irish

Ovrl Index: + 1.2%

·

Greece

ASE General Index: + 1.7%

Before Market Opens

S&P futures vs fair value: +0.20.

Nasdaq futures vs fair value: -1.50.

The S&P 500 futures trade within a point of fair value.

Markets gained across much of Asia.

The S&P 500 futures trade within a point of fair value.

Markets gained across much of Asia.

·

In

economic data:

o Australia's Q3 GDP rose 0.3%

quarter-over-quarter (expected 0.7%; previous 0.5%) while the year-over-year

reading increased 2.7% (consensus 3.1%; last 2.7%). Separately, AIG Services

Index ticked up to 43.8 from 43.6.

o China's Non-Manufacturing PMI ticked up to 53.9

from 53.8 while HSBC Services PMI inched up to 53.0 from 52.9 (expected

52.5)

o Hong Kong's Manufacturing PMI improved to 48.8

from 47.7

o India's HSBC Services PMI rose to 52.6 from

50.0

------

·

Japan's Nikkei climbed 0.3%, gaining for the fourth

consecutive session to finish at a new seven-year high. Continued weakness in

the yen aided exporters with Toyota Motor rising 0.9% and Fanuc adding

0.6%.

·

Hong

Kong's Hang Seng

lost 1.0%, giving up yesterday's gains to finish on the 200-day average.

Casino-related names remained pressured as Sands China and Galaxy Entertainment

both lost 5.1%.

·

China's Shanghai Composite added 0.6% as part of its

ninth advance in ten sessions. Commodity plays posted strong gains as Jiangxi

Copper climbed the limit, 10.0%, and Zijin Mining jumped 7.0%.

·

India's Sensex ended flat, holding near record highs

amid a subdued session. State-owned ONGC added 3% following reports the

government is considering altering subsidies.

Major European indices trade mixed with

Spain's IBEX (+1.1%) outperforming. Elsewhere, United Kingdom's Office of

Budget Responsibility hiked its 2014 GDP forecast to 3.0% from 2.7% and boosted

next year's outlook to 2.4% from 2.3%. Also of note, France confirmed it will

cut EUR3.60 billion from next year's budget and said the 2017 budget deficit to

GDP will come in below the 3.0% target set by the European Commission

·

Investors

received several data points:

o Eurozone Services PMI slipped to 51.1 from 51.3

(expected 51.3) while Retail Sales increased 0.4% month-over-month (expected

0.6%; last -1.2%). Year-over-year, retail sales rose 1.4% (consensus 1.2%;

prior 0.5%)

o Germany's Services PMI held at 52.1, as expected

o Great Britain's Services PMI rose to 58.6 from 56.2 (expected 56.6)

o French Services PMI fell to 47.9 from 48.8

(consensus 48.8)

o Italy's Services PMI improved to 51.8 from 50.8

(expected 50.9)

o Spain's Services PMI dropped to 52.7 from 55.9

(consensus 56.2)

o Swiss Q3 GDP rose 0.6% quarter-over-quarter

(expected 0.3%; last 0.3%) while the year-over -year reading increased 1.9%

(consensus 1.4%; previous 1.6%)

------

·

United

Kingdom's FTSE is

lower by 0.3% with energy names pressured. Petrofac, Royal Dutch Shell, and

Tullow Oil are down between 0.8% and 1.6%. Technology names outperform with ARM

Holdings and Sage Group higher by 1.9% and 4.6%, respectively.

·

In France, the CAC is lower by 0.1% amid weakness in

consumer names. Carrefour, Danone, and Pernod Ricard hold losses between 0.7%

and 1.8%. Financials hold gains with Credit Agricole and Societe Generale up

1.9% and 0.4%, respectively.

·

Germany's DAX holds a modest gain of 0.3% with help from

financials. Deutsche Bank has added 1.0% and Commerzbank trades higher by 0.6%.

Adidas is the weakest performer, down 3.2%, amid concerns about the company's

exposure to Russia.

·

Spain's IBEX leads with a gain of 1.1% amid broad

strength. Construction/engineering companies Abengoa, Acciona, and FCC are up

between 1.9% and 6.2%. Bank shares also trade in the green with Banco Sabedell,

Banco Popular, and Caixabank holding gains between 1.3% and 1.8%.

U.S. Equities

·

Equity

futures suggest little change at the open

·

MBA

Mortgage Index (-7.3%)

·

ADP

Employment Change (208K actual v. 225K expected)

·

Productivity-rev.

(2.3% actual v. 2.4% expected)

·

Unit labor

costs-rev. (-1.0% actual v. 0.0% expected)

o S&P Futures -1 @ 2065

o Dow Futures -3 @ 17859

o Nasdaq Futures unch @ 4306

Asia

·

Markets

gained across much of Asia

·

China's

Non-Manufacturing PMI (53.9 actual v. 53.8 expected) and HSBC Services PMI

(53.0 actual v. 52.9 previous) both improved from their previous readings

·

Australia's

GDP slowed to 0.3% QoQ (0.7% QoQ expected, 0.5% QoQ previous)

·

India's

HSBC Services PMI climbed to 52.6 (50.0 previous)

·

Japan's

Nikkei (+0.3%) gained for a fourth straight session to finish at a new

seven-year high

·

Hong

Kong's Hang Seng (-1.0%) gave up yesterday's gains and finished on the 200 dma

·

China's

Shanghai Composite (+0.6%) gained for the ninth time in ten sessions and closed

at its best level since July 2011

·

India's

Sensex (UNCH) held near record highs amid a subdued session

·

Australia's

ASX (+0.8%) saw a second day of solid gains

Market Internals

Market Internals -Technical-

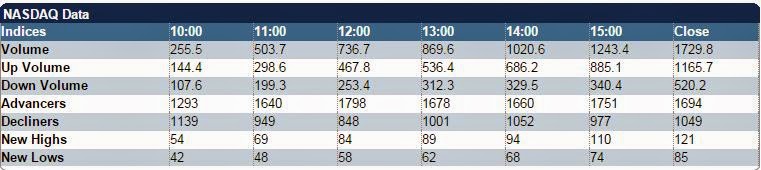

The Nasdaq closed 19 points higher (+0.36%) to 4774, the S&P 500 is up 8 (+0.38%) to 2074, and the Dow is up 33 (+0.18%) to 17912. Action came on mixed average volume (NYSE 756 mln vs. avg. of 703; NASDAQ 1577 mln vs. avg. of 1780), with advancers outpacing decliners (NYSE 2056/1128, NASDAQ 1694/1049) and new highs outpacing new lows(NYSE 197/77, NASDAQ 121/85).

Relative Strength:

Silver Miners-SIL +3.5%, Steel-SLX +2.4%, Oil&Gas Explr.-XOP +2.2%, Metals&Mining-XME +2.2%, Taiwan-EWT +2.1%, Alerian MLP-AMJ +2.0%, Clean Energy-PBW +1.9%, Jr. Gold Miners-GDXJ +1.8%, Semiconductors-SMH +1.7%, Oil Svcs.-OIH +1.6%, Columbia 20-GXG +1.3%, Emrg Mkts E. Eur.-ESR +1.2%, Canada-EWC +1.1%, Latin America 40-ILF +1.0%.

Relative Weakness:

US Nat. Gas-UNG -2.0%, Vix Short-Term-VXX -1.8%, US Diesel/Heating Oil-UHN -1.5%, Livestock-COW -1.4%, Malaysia-EWM -1.3%, Cocoa-NIB -1.2%, Agriculture-DBA -0.9%, Hong Kong-EWH -0.8%, Copper-JJC -0.8%, Turkey-TUR -0.7%, Sugar-SGG -0.7%, Cons. Stpls.-XLP -0.7%, Swiss Franc-FXF -0.6%, China Lg. Cap-FXI -0.5%.

Leaders and Laggards

Technical Updates

Briefing's Commentaries

Closing Market Summary: Russell 2000

Leads Stocks Higher

The stock market ended the midweek session on an upbeat note with the Russell 2000 (+1.0%) pacing the advance for the second day in a row. Meanwhile, the S&P 500 posted a more modest gain of 0.4% with seven sectors ending in the green.

Similar to yesterday, equities were essentially left to their own devices amid a lack of market-moving news. Cyclical sectors were responsible for the bulk of the advance as all six growth-sensitive groups ended in the green while health care (+0.2%) was the lone gainer on the countercyclical side.

The materials sector (+1.4%) settled in the lead after showing relative strength throughout the session. The group benefitted from strength among steelmakers and miners with Market Vectors Steel ETF (SLX 39.15, +0.90) and Market Vectors Gold Miners ETF (GDX 19.60, +0.40) climbing 2.4% and 2.1%, respectively.

Meanwhile, another commodity-related sector—energy (+1.2%)—settled just behind materials, which represented the third consecutive day of relative strength for the recently-battered sector. Today's advance occurred amid a 0.5% gain in crude oil ($67.30/bbl) and helped the sector extend its week-to-date gain to 3.2%.

Elsewhere, the industrial sector (+1.3%) was the only other group to add more than 1.0%. The top-weighted sector component—General Electric (GE 26.38, +0.33)—spiked 1.3% while transport stocks also displayed relative strength. The Dow Jones Transportation Average settled higher by 0.8% with Alaska Air (ALK 56.76, +1.51) setting the pace.

Also of note, the technology sector (+0.5%) underperformed in the morning, but powered to new highs during the final hour. The sector was underpinned by chipmakers and its strength helped the S&P 500 to a new high just ahead of the close. As for chipmakers, the group rallied broadly after Microchip Technology (MCHP 46.59, +1.94) said it is confident the small correction experienced in the third quarter is now in the past. The stock spiked 4.3% while the PHLX Semiconductor Index jumped 2.0%.

Over on the countercyclical side, consumer staples (-0.8%), telecom services (-0.8%), and utilities (-0.3%) ended in the red while health care (+0.2%) turned positive in the early afternoon. Biotechnology contributed to the rebound with the iShares Nasdaq Biotechnology ETF (IBB 308.25, +1.38) climbing 0.5%.

Treasuries spent the bulk of the session near their flat lines before ending close to highs. The 10-yr yield slipped one basis point to 2.28%.

Participation was a bit below average with just over 755 million shares changing hands at the NYSE floor.

Economic data included ADP Employment Change, Q3 Labor Productivity Data, ISM Services, and the MBA Mortgage Index:

The stock market ended the midweek session on an upbeat note with the Russell 2000 (+1.0%) pacing the advance for the second day in a row. Meanwhile, the S&P 500 posted a more modest gain of 0.4% with seven sectors ending in the green.

Similar to yesterday, equities were essentially left to their own devices amid a lack of market-moving news. Cyclical sectors were responsible for the bulk of the advance as all six growth-sensitive groups ended in the green while health care (+0.2%) was the lone gainer on the countercyclical side.

The materials sector (+1.4%) settled in the lead after showing relative strength throughout the session. The group benefitted from strength among steelmakers and miners with Market Vectors Steel ETF (SLX 39.15, +0.90) and Market Vectors Gold Miners ETF (GDX 19.60, +0.40) climbing 2.4% and 2.1%, respectively.

Meanwhile, another commodity-related sector—energy (+1.2%)—settled just behind materials, which represented the third consecutive day of relative strength for the recently-battered sector. Today's advance occurred amid a 0.5% gain in crude oil ($67.30/bbl) and helped the sector extend its week-to-date gain to 3.2%.

Elsewhere, the industrial sector (+1.3%) was the only other group to add more than 1.0%. The top-weighted sector component—General Electric (GE 26.38, +0.33)—spiked 1.3% while transport stocks also displayed relative strength. The Dow Jones Transportation Average settled higher by 0.8% with Alaska Air (ALK 56.76, +1.51) setting the pace.

Also of note, the technology sector (+0.5%) underperformed in the morning, but powered to new highs during the final hour. The sector was underpinned by chipmakers and its strength helped the S&P 500 to a new high just ahead of the close. As for chipmakers, the group rallied broadly after Microchip Technology (MCHP 46.59, +1.94) said it is confident the small correction experienced in the third quarter is now in the past. The stock spiked 4.3% while the PHLX Semiconductor Index jumped 2.0%.

Over on the countercyclical side, consumer staples (-0.8%), telecom services (-0.8%), and utilities (-0.3%) ended in the red while health care (+0.2%) turned positive in the early afternoon. Biotechnology contributed to the rebound with the iShares Nasdaq Biotechnology ETF (IBB 308.25, +1.38) climbing 0.5%.

Treasuries spent the bulk of the session near their flat lines before ending close to highs. The 10-yr yield slipped one basis point to 2.28%.

Participation was a bit below average with just over 755 million shares changing hands at the NYSE floor.

Economic data included ADP Employment Change, Q3 Labor Productivity Data, ISM Services, and the MBA Mortgage Index:

·

The ADP

report revealed that employment in the nonfarm private business sector rose

208K in November, which was below the increase of 225K expected by the

Briefing.com consensus.

·

Q3

nonfarm business productivity was revised up to 2.3% from an originally

reported 2.0% gain while the Briefing.com consensus expected a revision to

2.4%

o Unit labor costs were revised down and now show

a 1.0% decline in the third quarter after initially showing a small 0.3%

increase. The consensus expected a flat reading.

§ This was the second consecutive quarterly

decline

·

The ISM

Services Index for November rose to 59.3 from 57.1 while the Briefing.com

consensus expected an uptick to 57.5

·

The

weekly MBA Mortgage Index fell 7.3% to follow last week's 4.3% decline

Tomorrow's data will be limited to the

Challenger Job Cuts report for November, which will be released at 7:30 ET

while weekly Initial Claims will cross at 8:30 ET (Briefing.com consensus

295K).

·

Nasdaq

Composite +14.3% YTD

·

S&P

500 +12.2% YTD

·

Dow Jones

Industrial Average +8.1% YTD

·

Russell

2000 +1.4% YTD

Commodities

Closing Commodities: Oil Ends With

Modest Gain, Natural Gas Extends Recent Losses

·

Commodities

felt some pressure today as the dollar index continued to hold its gains

·

In

current trade, the index remains near its HoD

·

At the

end of today's session, Jan crude gained $0.33 to $67.30/barrel, even after

pulling back off its HoD

·

Natural

gas was weak again due to a mild weather outlook in the U.S. (49% of U.S. homes

use nat gas for heating)

·

Metals

ended the day mixed...

·

Feb gold

rose $10.40 to $1209/oz today, while Mar silver fell $0.03 to $16.42

·

Mar

copper lost one cent to $2.87/lb

Metals price action

·

Gold rose

$10.40 today to close at $1209/oz

·

Silver

fell $0.03 to $16.42/oz

·

Copper

fell 1 cent to $2.87/lb

Agricultural price action

·

Corn

closed 13 cents lower at $3.82/bushel

·

Wheat

fell 7 cents to $5.96/bushel

·

Soybeans

rose 3 cents to $9.99/bushel

·

Ethanol

rose 7 cents to $1.74/gallon

·

Sugar #11

fell -0.15 cents to 15.09 cents/gallon

Energy price action

·

Crude oil

rose $0.33 to $67.30/barrel

·

Natural

gas fell 8 cents to $3.80/MMBtu

·

Heating

oil fell 2 cents to $2.13/gallon

·

RBOB fell

1 cent to $1.80/gallon

Treasuries

Long Bond Leads Late-Day Rally: 10Y:

+02/32..2.284%..USD/JPY: 119.80..EUR/USD: 1.2313

·

A late-day

rally propelled the Treasury complex to a mixed close. Click here to see an intraday

yields chart.

·

The

complex saw light selling ahead of the cash open and whipped around as today's mixed

data crossed the wires.

·

The soft

ADP Employment Report (208K actual v. 225K expected) got the data

started with both productivity-rev. (+2.3% actual v. +2.4% expected)

and unit labor costs-rev. (-1.0% actual v. 0.0% expected) also missing

estimates.

·

However,

not all of the data was bad as ISM Services (59.3 actual v. 57.5

expected) saw one of its strongest readings on record.

·

Yields

across the complex held in a tight 3bp range throughout the session, and saw some slippage into the close after the

release of the latest Beige Book.

·

The Beige

Book showed 'widespread' job growth and suggested the U.S. economy continues to

expand.

·

Up front,

the 2Y added +1.5bps to 0.551%. The yield is probing the upper end of the

0.500%/0.550% range that was in place throughout November.

·

In the

belly, the 5Y tacked on +1.8bps to 1.608%. The yield reclaimed both the 50 dma

and prior support at the 1.600% level.

·

The 10Y

edged up +0.2bps to 2.287%. The benchmark yield probed the important 2.300%

area early in the session, but was unable to register a close above the mark.

·

The 30Y

slipped -1.1bps to 2.993% thanks to some late-day buying. What was previously

support near 3.000% is now critical resistance.

·

A

slightly flatter curve developed as the 2-10-yr spread tightened to 173.5bps.

·

Precious

metals saw a mixed session as gold rallied +$10 to $1209 and silver eased

-$0.08 to $16.38.

·

Data: Challenger Job Cuts (7:30) and initial and

continuing claims (8:30).

·

Fed Speak: Cleveland's Mester makes opening remarks at

the 2014 Financial Stability Conference (8:30). Fed Governor Brainard

duplicates his speech from the previous day (13:15).

On other news....

Currencies

Dollar Flirts with 89.00: 10Y:

+01/32..2.290%..USD/JPY: 119.82..EUR/USD: 1.2304

·

The

Dollar Index drifts on session highs near 89.00 amid a rather subdued trade. Click here to see a daily Dollar

Index chart.

·

The Index

raced to the level following this morning's data, and has held in a tight range

near the highs for the remainder of the session.

·

EURUSD is -75 pips @ 1.2305 as trade slides to

a 28-month low ahead of tomorrow's European Central Bank policy decision.

Expectations remain low for the central bank to announce a QE-type program, but

traders cannot completely rule out such action.

·

GBPUSD is +55 pips @ 1.5690 action contends with

15-month lows. Sterling has been supported despite the latest Autumn

Forecast Statement suggesting the government is expected to borrow more money

(GBP91.3 bln actual v. GBP86.6 previous) than previously anticipated. The

1.5600 level will be watched closely into tomorrow's Bank of England

rate decision.

·

USDCHF is +60 pips @ .9780 as trade readies for its

best close in over one and a half years. The pair saw little response to the better

than expected Swiss GDP print, and instead remained tightly correlated to

the fluctuations in the euro.

·

USDJPY is +65 pips @ 119.85 as action rallied to its best

levels in over seven years. Buyers emerged early in the session, and

ran the pair to fresh highs after a Nikkei report suggested Prime

Minister Shinzo Abe was likely to win a super majority in the upcoming

election. The psychologically important 1.2000 level remains within

striking distance.

·

AUDUSD is -35 pips @ .8405 as trade readies for its

worst close since July 2010. The hard currency came under pressure in overnight

trade after Australian GDP missed forecasts, but managed to pare

its losses as China's Non-Manufacturing PMI and HSBC Services PMI both

showed improvement from prior readings. Australia's retail sales and

trade balance are due out tonight.

·

USDCAD is -45 pips @ 1.1360 after the Bank of

Canada held its overnight rate at 1.00% and suggested the recent uptick in

inflation was temporary. Trade has struggled in recent days near

1.1400/1.1450. Bank of Canada Governor Stephen Poloz will speak early

this evening in Toronto. Canada's Ivey PMI is scheduled for tomorrow.

Next Week In View

Economic Commentaries

Economic Summary: ADP misses the mark;

ISM Services tops expectations

Economic Data Summary:

Economic Data Summary:

·

Weekly

MBA Mortgage Applications -7.3% (Last Week was -4.3%)

·

November

ADP Employment Change 208K vs Briefing.com consensus of 225K; October was

revised to 233K from 230K

o Goods-producing 32,000

o Service-providing 176,000

·

Third

Quarter Productivity Revenue - Revised - 2.3% vs Briefing.com consensus of

2.4%; Third Quarter - Preliminary - was 2.0%

·

Third

Quarter Unit Labor Costs - Revised -1.0% vs Briefing.com consensus of 0.0%;

Third Quarter - Preliminary - was 0.3%

o Productivity growth is still down from a 2.9%

increase in Q2 2014. As expected from the upward revision to Q3 2014 GDP,

output was revised up to 4.9% in the third quarter from 4.4% in the advance

release. Hours worked were also revised higher, but at a smaller rate (2.5%

from 2.3%). The bigger gain in output compared to hours worked resulted in the

increase in productivity.

·

November

ISM Services 59.3 vs Briefing.com consensus of 57.5; October was 57.1

o The underlying conditions are ripe for further

production gains over the next few months as strong new orders growth were

delegated to backlogs instead of immediate fulfillment. The New Orders Index

increased to 61.4 in November from 59.1 in October. Backlogs increased to 55.5

from 51.5 in Octobers.

Upcoming Economic Data:

·

November

Challenger Job Cuts due out Thursday at 7:30 (Briefing.com consensus of ;

October was 11.9%)

·

Weekly

Initial Claims due out Thursday at 8:30 (Briefing.com consensus of 295K; Last

Week was 313K )

·

Weekly

Continuing Claims due out Thursday at 8:30 (Briefing.com consensus of 2.343 M ;

Last Week was 2.316 M )

Upcoming Fed/Treasury Events:

·

Philadelphia

Fed President (voting FOMC member, hawkish) to speak today at 12:30

·

Dallas

Fed President (voting FOMC member, hawkish) to speak at 19:30

·

Cleveland

Fed President Mayer (voting FOMC member) to speak tomorrow at 8:30 and Friday

at 12:30

Other International Events of Interest

·

China's

Non-Manufacturing PMI (53.9 actual v. 53.8 expected) and HSBC Services PMI

(53.0 actual v. 52.9 previous) both improved from their previous readings

Jason's Commentaries

Well it still seemed that the market still looking bullish while more economic indicator are still looking ok.. It's just that the France's PMI is contracting, while the rest are still expanding. Materials and industrials were the main movers last night with 1.33% and 1.47% gain. Volumes ere dipping slightly be low 800m shares traded on the NYSE. Nothing notable last night besides Dow and S&P500 broke new high again. It appears that the market is likely to profit take at the end of the trading session before the employment report today, which is expected to be much higher ahead of the Black Friday.

Market Call: FLAT to downside

Date: 4 Dec 2014

No comments:

Post a Comment