31 August 2012

Market Summary

What a crazy gyration during the Jackson Hole Symposium... Right at the start of Ben Bernanke's speech, market was up 100 points on the DOW. The moment Bernanke start talking, the DOW wiped out its gains for the day until his last sentence, sent the DOW back up to about 100 points.

Here's Bernanke's last line for his speech...

By the last sentence of his speech,

Here's Bernanke's last line for his speech...

By the last sentence of his speech,

as the line says ' the Federal Reserve will provide additional policy accommodation as needed to promote a stronger economic recovery and sustained improvement...' hints the readiness of Ben to start another QE and his defence of the past QEs versus the benefits/costs.

This is really a bullish day.....

Check the internals out...

Bears were totally out of the picture until the last hour where people started to profit take in view of Draghi's speech on Monday.

Prepare for some crazy gyration for the coming weeks!

Market Internals

Leaders and laggards

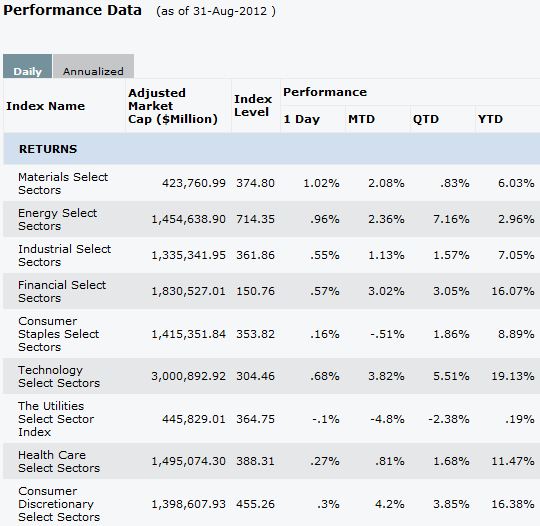

I was pretty surprised that the financial did not lead the day but except Materials and Energy...

Technical Updates

A chopstick bottom on the DOW and a Bullish Harami on the SPX. Seems that it's heading upwards... but if Draghi comes out with something lesser than the market's expectation.... the pattern gonna fail!

Commentaries

|

Commodities

Treasuries

The treasuries sold off when helicopter ben spoke.... Man... this man's mouth is powerful....

Week 35

Technical Updates

Commentaries

| Weekly Wrap

Dow +90.13 at 13096.02, Nasdaq +18.25 at 3066.96, S&P +7.10 at 1406.58

Stocks got off to a strong start before stumbling slightly when Federal Reserve Chairman Ben Bernanke did not hint at additional easing, but instead reaffirmed his commitment to act if economic conditions worsen. Mr. Bernanke commented on the stagnation of the labor market, calling it a "grave concern" which bears monitoring. While Bernanke wasn't expected to roll out a new round of quantitative easing at this venue, the discussion of the costs of nontraditional policies may temper expectations for additional easing in the absence of greater economic deterioration. As a result, the S&P 500 finished higher by 0.5%.

Shares of major financials were broadly higher early in the session. However, most names slipped off their highs after it became clear that additional quantitative easing is not imminent. Goldman Sachs (GS 105.72, +1.00) and American Express (AXP 58.30, +1.13) ended higher by 1.0% and 2.0%, respectively. Meanwhile, European financials saw even bigger advances as plans to create a Spanish "bad bank" surfaced. Banco Bilbao Vizcaya Argentaria (BBVA 7.53, +0.36) gained 5.0%, while Deutsche Bank (DB 35.45, +1.59) and Credit Suisse (CS 19.25, +0.68) advanced 4.7% and 3.7%, respectively.

Energy stocks outperformed the broader market with the S&P energy sector firmer by 0.9% as the fear of hurricane-related disruptions dissipates. Anadarko Petroleum (APC 69.27, +1.01), and EOG Resources (EOG 108.30, 2.41) added roughly 1.7%. Elsewhere in the sector, China Ming Yang Wind Power Group (MY 1.21, +0.06) jumped 5.2% after forming a joint venture to develop additional wind and solar power technology with Huaneng Renewables. On the downside, Arch Coal (ACI 6.11, -0.07) slipped 1.1% after announcing the company's Senior Vice President of Marketing, David Warnecke, will retire in May 2014.

Utility stocks underperformed the broader market as most names in the SPDR Utilities Select Sector ETF (XLU 36.35, -0.04) traded lower. PG&E (PCG 43.41, -0.15), Exelon (EXC 36.47, -0.12), and Southern Company (SO 45.33, -0.05) were all down near 0.3%. Meanwhile, U.S. listings of Brazilian utility companies were under heavy pressure as Centrais (EBR 6.50, -0.45), Companhia Paranaense de Energia (ELP 17.79, -0.71), and Cia Energetica de Minas Gerais (CIG 17.00, -0.84) slumping between 4.5% and 6.5%.

Facebook (FB 18.06, -1.03) fell 5.4% after Stifel Nicolaus said that despite attractive valuation, it may still be too early to invest in the company as insider selling continues. Today's selling has pushed the stock down to $18.06, which is the lowest price since the initial public offering in May. Zynga (ZNGA 2.80, -0.09) and Groupon (GRPN 4.15, -0.04), two companies which have recently held their initial public offerings, slid 3.1% and 1.0%, respectively. Zynga traded $0.15 above its all-time low, while Groupon marked fresh lows.

The volatility index, or VIX, shed 1.5%, to 17.56. Two weeks ago, the volatility measure marked a 5-year low at 13.45, and has been on a steady rise since. This week alone, the VIX has risen by 8.5%.

Today's economic data was mixed. The August Chicago PMI of 53.0 surprised to the downside as economists had generally expected a reading of 53.8 to follow the prior month's 53.7. Elsewhere, the University of Michigan's final Consumer Sentiment Survey for August rose to 74.3 from the 73.6 that was posted in the preliminary Survey. Separately, July Factory Orders showed an increase of 2.8%, which was better than the Briefing.com consensus of a 2.0% increase.

On Tuesday, the August ISM Index and July construction spending will be reported at 10:00 ET. In addition, August auto and truck sales will be released at 14:00 ET.

Week in Review: Markets Quiet Ahead of Jackson Hole

Monday's session began on a positive note before stocks retreated to the unchanged line. As the European markets closed for the day, U.S. stocks lifted to session highs, but the gains did not hold into the close. As a result, the S&P 500 finished flat on low volume while the Dow shed 0.3%. Apple (AAPL 665.24, +1.37) advanced 1.9% after winning its patent battle against Samsung.

On Tuesday, Equities spent the majority of the session within points of the unchanged line. The August consumer confidence report printed at 60.6, which was the lowest level in nine months. Following the report, stocks briefly turned lower before snapping back to the unchanged line where they held for the remainder of the session. Luxury goods maker Movado (MOV 35.16, +0.19) soared 17.4% after beating earnings expectations by $0.14 a share.

Wednesday's lackluster session saw equities hover within points of the flat line for the majority of the day. Economic data was mostly positive, but did little to inspire investor confidence. As a result the S&P 500 ended higher by 0.1% on light volume. Yelp (YELP 22.00, +0.31) surged 22.5% despite the share lock-up expiry.

On Thursday, equities hit session lows during the first hour of trade before spending the rest of the day climbing off those levels. Headlines out of Europe indicated the International Monetary Fund sees a "major challenge" in implementing measures for Greece. Another comment which rattled the markets came from Slovak Prime Minister, Robert Fico, who suggested there is a 50% chance of a euro area breakup. The news resulted in a sharp sell-off in risk assets as crude oil, gold, silver, and the euro all fell to session lows. Stocks were able to recover some of their losses before succumbing to late-day selling pressure which resulted in the S&P 500 closing lower by 0.8%. Costco Wholesale (COST 97.87, -0.72) advanced 1.5% after August same store sales increased by 6.0%.

|

Next Week in View

Market Call: 1 Sept

Market Call(Weekly): NO CALL!!! DRAGHI IS SPEAKING!AND NON FARM PAYROLLS!

Date: Week 36

No comments:

Post a Comment