7 September 2012

Market Summary

Well.. the market seems to be confused after the employment report that came out on Friday, 830am ET.

After ECB's Chairman, Mario Draghi's decision to carry out the european's version of QE, which is only buying bonds in the short term(3 years). However, Germany's Chancellor Merkel has not decided to participate in Draghi's campaign. I believe Merkel's participation in Draghi's campaign is essential as Germany is the strongest Euro country as of now.

The employment report came in way under expectation, causing the market to gyrate in a very confused manner. However, market started to rally through the last hour in the trading day.

I believe with this Euro QE coming, Bernanke will further boost the fire by coming up with QE 3, especially such a disappointing employment report on Friday. Anything in all, we shall take a look at the FOMC statement on Thursday Sep 13, 1230pm ET.

Market Internals

Despite it being a flat day...the ADVN clearly outpaced the DECN. Volumes started improving already, getting above 679 million shares traded in the NYSE. New Highs outpacing New lows. It's a bullish day.

Leaders and laggards

Materials, Energy, Financials taking the lead for the day, with utilities and staples lagging behind... Money might be flowing into the leading sectors already.... With the Financials, Consumer discretionary leading from MTD, it's a bullish sign for the market.

Technical Updates

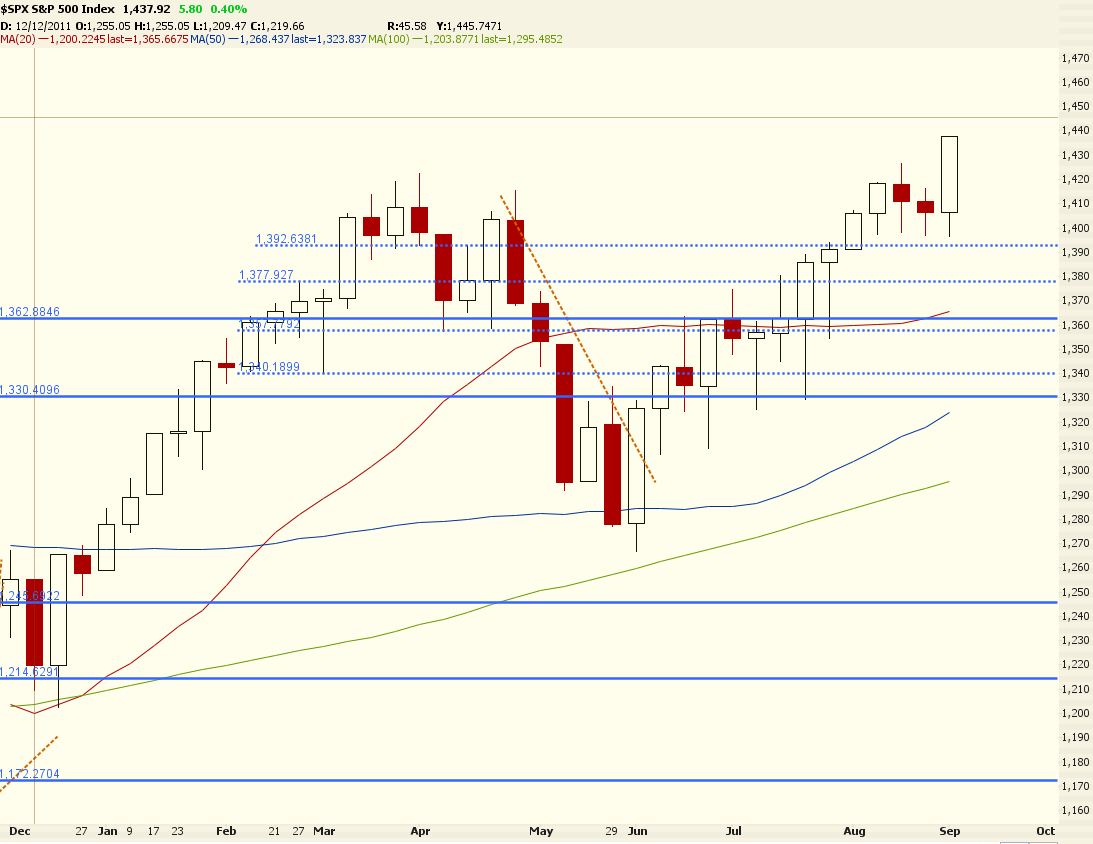

On the technical note, the DOW hit its 2yr high at 13300. Felt a little constipation over there. However, the SPX broke above its resistance at 1420.

Commentaries

|

Commodities

With the Crude Oil hitting a resistance at 97.50, and with an under production in oil, i believe that resistance should be broken soon. We should be seeing a $100 oil very soon......

Treasuries

Well... money is flowing back into the risk market for a while for now... guess the treasuries gonna suffer a little now...

Technical Updates

On a technical note on the weekly charts, SPX finished it's third candle reversal on a breakout and DOW finished it's third candle reversal.

Commentaries

| Weekly Wrap

Dow +14.64 at 13311.82, Nasdaq +0.61 at 3136.42, S&P +5.80 at 1437.92

Stocks got off to a mixed start after this morning's jobs data proved to be a disappointment. The anemic numbers turned into yet another argument in favor of additional easing while lower guidance from a technology bellwether contributed to a divergence in the major averages. The S&P 500 finished higher by 0.4% while the Nasdaq ended flat.

Nonfarm payrolls were reported at 96K versus the 130K Briefing.com consensus. The prior reading was revised down to 141K from 163K. In addition, nonfarm private payrolls added 103K against the 144K consensus. Separately, the unemployment rate was reported at 8.1% versus the 8.3% consensus estimate as the dip in the unemployment rate was attributed to more people leaving the workforce.

Major financials rallied after disappointing jobs data sparked another round of quantitative easing hopes. The SPDR Financial Select Sector ETF (XLF 15.68, +0.16) advanced 1.0% as Bank of America (BAC 8.80, +0.45) and Morgan Stanley (MS 17.08, +0.83) gained over 5.0% each. Other major names showed less robust advances as Citigroup(C 32.06, +0.94) and Goldman Sachs (GS 116.33, +2.79) added 3.0% and 2.5%, respectively. Meanwhile, European financials continued their exuberance for the second day in a row. Barclays (BCS 13.17, +0.86) and Deutsche Bank (DB 40.20, +2.59) jumped near 7.0% each.

Stocks listed in the Dow underperformed the broader market as two notable components showed weakness. Kraft Foods (KFT 39.99, -2.32) slid 5.5% after providing an update on its planned spin-off. Beginning October 1, 2012 the company will separate into two entities. Kraft Foods Group which will hold the North America grocery business will begin trading under the ticker ‘KRFT' while Kraft Foods will be renamed Mondelez International and trade under the symbol ‘MDLZ.' Today's weakness came after the company announced it expects Kraft Foods full-year 2013 earnings at $2.60 per share. Meanwhile, technology companies within the index are slumped after Intel (INTC 24.19, -0.90) cut its third quarter guidance below consensus. The technology bellwether slid 3.6% while Cisco(CSCO 19.56, -0.16), Microsoft (MSFT 30.95, -0.39), and Hewlett-Packard (HPQ 17.42, -0.17) lost between 0.8% and 1.5%.

Technology stocks outside of the Dow were also under pressure after Intel's guidance cut. Peer AMD (AMD 3.45, -0.21) slumped 5.7% while related names, NVIDIA (NVDA 13.40, -0.33) and Micron (MU 6.42, -0.25) slipped 2.4% and 3.8%, respectively.

The materials sector settled higher by 2.0% as it outperformed other sectors. Over the past two days, China announced plans to increase infrastructure spending which may bode well for basic materials demand. Iron and steel names showed biggest gains asCliffs Natural Resources (CLF 39.91, +5.05) jumped 14.5%. Meanwhile, United States Steel (X 20.89, +1.68), AK Steel (AKS 5.78, +0.41), and Freeport-McMoRan (FCX 39.43, +3.09) posted advances near 8.0%.

Within the healthcare space, biotechnology stocks weighed on the rest of the sector. TheSPDR S&P Biotech ETF (XBI 91.59, -0.43) slipped 0.5%. Spectrum Pharmaceuticals(SPPI 12.01, -0.59) posted the biggest loss within the group as it finished lower by 4.7%. Meanwhile, Medivation (MDVN 105.65, -2.97) and Theravance (THRX 23.91, -0.28) fell 2.7% and 1.2%, respectively. On the upside, pharmaceutical company Peregrine (PPHM 4.50, +1.43) surged 46.6% after reporting that its Bavituximab drug has doubled the median overall survival rate in lung cancer patients who are taking part in the company's phase II trial.

Internet radio provider Pandora (P 10.47, -2.10) slumped 16.7% after reports suggestedApple (AAPL 680.44, +4.17) may include internet radio on its devices and integrate the service into its iTunes store. Apple finished higher by 0.6% after marking a fresh all-time high at $681.50 while today's selling has dropped shares of Pandora back to levels last seen before its August 30 earnings report.

Week in Review: Mario Draghi Press Conference Highlights the Week

On Monday, stocks got off to a strong start before stumbling slightly when Federal Reserve Chairman Ben Bernanke did not hint at additional easing, but instead reaffirmed his commitment to act if economic conditions worsen. Mr. Bernanke commented on the stagnation of the labor market, calling it a "grave concern" which bears monitoring. As a result, the S&P 500 finished higher by 0.5%. European financials saw broad advances as plans to create a Spanish "bad bank" surfaced. Banco Bilbao Vizcaya Argentaria(BBVA 8.27, +0.23) gained 5.0%.

On Tuesday, stocks opened unchanged before falling into the red after economic data missed expectations. The August ISM Index was reported at 49.6 versus the 50.0 Briefing.com consensus, while July construction spending fell 0.9% month-over-month, against the expected increase of 0.5%. After reaching session lows 90 minutes after the open, stocks staged a slow climb higher which was punctuated by a broad-based mid-afternoon rally. Stocks rallied back near the flat line where they remained until the end of the day. As a result, the S&P 500 slipped 0.1% while Nasdaq gained 0.3%. NVIDIA(NVDA 13.40, -0.33) slid 5.4% after being downgraded from ‘equal weight' to ‘underweight' by Evercore.

Wednesday's session was spent mostly around the unchanged line. The early morning volatility coincided with a Bloomberg TV report which indicated the European Central Bank bond purchase program was said to pledge unlimited, sterilized buying of bonds. However, the exuberance was short-lived as European Central Bank officials declined to comment, and reports out of Germany suggested Chancellor Angela Merkel would only support the program in the near-term. Afternoon trade was mostly quiet as the S&P 500 remained in a narrow range before closing lower by 0.1%. FedEx (FDX 87.38, -0.16) shed 2.0% after lowering its first quarter guidance, citing weaker global demand.

On Thursday, equities began sharply higher, and added to their gains throughout the opening hour of trade. The remainder of the day was spent hovering near session highs. The bullish sentiment was sparked after Mario Draghi confirmed Thursday's reports of a European Central Bank plan to buy bonds of troubled sovereigns who ask for aid. The program will be limited to bonds maturing within three years. Better-than-expected U.S. economic data also added to the upbeat tone which resulted in a broad market rally. The Nasdaq closed at a 12-year high while the S&P 500 settled at levels not seen since January 2008. The two indices finished higher by 2.2% and 2.0%, respectively. The SPDR Financial Select Sector ETF (XLF 15.68, +0.16) added 2.4%.

|

Next Week in View

this coming week is going to be another data heavy week with the FOMC statement and CPI, Retail sales report coming out.

I believe the market will be quiet before Thursday and the whole week will be centered on Ben Bernanke's speech.

Market Call: 9 Sept

Date: NO CALL!!! FOMC STATEMENT

Market Call(Weekly): NO CALL!!! FOMC STATEMENT

Date: NO CALL!!! FOMC STATEMENT

Market Call(Weekly): NO CALL!!! FOMC STATEMENT

No comments:

Post a Comment