10 Oct 2012

Market Summary

Whoa... the market went down more than I expected... so it seems that i'm kinda right isn't it! HAHA.

I suspect that this headline scares the shit of many people. Btw, there was a G7 meeting yesterday and came out with such headlines... that's not very promising.

IMF Sees ‘Alarmingly High’ Risk of Deeper Global Slump

A few days ago, there was a news paper article stating that Singapore may enter a technical recession. If the strongest economy in the ASEAN is facing such headlines... what do you think the entire region will face? You come up with your own conclusion...

What surprises me was VIX went down when the market went down.... that shows many players in the market... didn't bother hedging... but sold off straight again...

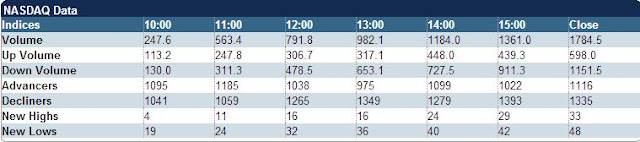

Market Internals

.

Looking at that volume.... it's not a very high commitment day isn't it... the bulls aren't coming in... only the bears are in the game...

Leaders and Laggards

The main laggards are the materials and the energy sector...

AA and CXV were the main laggards in the DOW and in their respective sectors. So I would say that the drop was not entirely in the broader market...

Technical Updates

On the DOW and SPX... some very scary is forming... the H & S... if these 2 indices don't hold that neckline.. we're going to see a correction before the presidential election!

Commentaries

|

| Stock Market Update |

16:15 ET Dow -128.56 at 13344.97, Nasdaq -13.24 at 3051.78, S&P -8.92 at 1432.56 :[BRIEFING.COM] Equities got off to a mixed start as the key indices chopped around their respective unchanged lines during the first hour. Sellers took control after traders digested the wholesale inventories data, pushing the major averages to their worst levels. Afternoon trade was mostly quiet as the three averages hovered near session lows. As a result, the S&P 500 finished lower by 0.6%.

Earlier, the Federal Reserve released its September Beige Book. In its report, the twelve Federal Reserve Districts reported that economic activity "expanded modestly since the last report." Residential real estate conditions as well as the nonfinancial services sector also showed modest improvement.

The manufacturing sector was described as mixed but somewhat healthier than what was observed in the last report. Meanwhile, the industrial market was also described as mixed. While the Philadelphia, New York, Cleveland, and Atlanta districts all showed strength, conditions in Richmond deteriorated slightly. The Beige Book also commented on consumer spending by saying it was mostly unchanged since the previous report.

Financials registered the slimmest losses and the SPDR Financial Select Sector ETF(XLF 15.94, -0.01) shed 0.1%. Among the majors, Citigroup (C 35.14, +0.54) andJPMorgan Chase (JPM 41.77, +0.39) were the top performers. The two names registered respective gains of 1.6% and 0.9% after Bank of America/Merrill Lynch resumed coverage of the two stocks with a ‘buy' rating. Note that JPMorgan Chase will report its third quarter earnings before Friday's open.

European financials saw mixed performance as Deutsche Bank (DB 41.17, +0.33) added 0.8% while Spanish Banco Bilbao Vizcaya Argentaria (BBVA 7.59, -0.10) slipped 1.3%.

Energy stocks were the biggest laggard of the session. Chevron (CVX 112.45, -4.91) slid 4.2% after announcing that its third quarter earnings are expected to be substantially lower than results from the previous quarter. Penn Virginia (PVA 5.10, -0.39) andTesoro (TSO 38.70, -2.29) lost 7.1% and 5.6%, respectively.

The Dow Jones Transportation Average outperformed the broader market with a gain of 0.1%. However, the strength was largely due to FedEx (FDX 89.52, +3.94). The bellwether stock gained 5.2% after announcing a program which targets $1.7 billion in annual profit improvements by the end of fiscal year 2016. In addition, the company reaffirmed its second quarter and full-year 2012 guidance which it had revised down on September 18.

Elsewhere, Alcoa (AA 8.71, -0.42) dipped 4.6% after beating on earnings and revenues. However, the company's third quarter revenue of $5.833 billion represents a 9.1% year-over-year decrease. In addition, AA lowered its 2012 global aluminum demand growth forecast from 7.0% to 6.0%.

Engine maker Cummins (CMI 87.79, -3.05) slid 3.4% after lowering its third quarter and full-year 2012 guidance due to weak demand. Caterpillar (CAT 83.16, -1.59) slipped 1.9% in sympathy.

Ambarella (AMBA 6.06, +0.06) made its public debut today. The producer of video processing semiconductors priced its initial public offering at $6, which was well below the expected price range of $9 to $11. The stock settled higher by 1.0% after shares began trading at $6.66.

August wholesale inventories increased by 0.5%. This was slightly lower than the increase of 0.6% which had been broadly forecast.

Weekly initial and continuing jobless claims, August trade balance, September export prices ex-agriculture, and September import prices ex-oil will all be reported at 8:30 ET.

The U.S. Treasury will look to make it three strong auctions for the week with tomorrow's $13 billion, 30-yr reopening. ..NYSE Adv/Dec 1144/1890. ..NASDAQ Adv/Dec 1121/1337 | | |

|

After Hours

17:18 ET MSW +5.7%, RT -7.4%, PVTB -1.8% following earnings/guidance :

Equities got off to a mixed start as the key indices chopped around their respective unchanged lines during the first hour. Sellers took control after traders digested the wholesale inventories data, pushing the major averages to their worst levels. Afternoon trade was mostly quiet as the three averages hovered near session lows. As a result, the S&P 500 finished lower by 0.6%.

Today after the close the following companies are scheduled to report earnings: DRWI, PVTB, RELL, RT, VOXX, SCMR

Futures are lower after hours: S&P 500 futures are -3.74 from fair value of 1427.24 and Nasdaq100 futures are -4.47 from fair value of 2722.47.

Tomorrow morning before the open three economic reports are scheduled to be released: 1) Initial Claims (Consensus 370k) and Continuing Claims (Consensus 3275k), 2) Trade Balance (Consensus -43.8B) and 3) Export Prices ex-ag. and Import Prices ex-oil.

Tomorrow before the open the following companies are scheduled to report earnings: CMN, FAST, SWY, WGO

Commodities

Treasuries

Not much movement in the treasuries...

The only market mover is likely to be the trade balance and the unemployment claims today...

Market Call: FLAT(to upside)

Date: 10 Oct 2012

.

.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

No comments:

Post a Comment