12 Oct 2012 AMC

Market Summary

Time for the market analysis!! Was busy during the weekend but finally got the time to write my analysis..

Last friday, the 3 of the major DOW components held DOW up for the day, but the majority of the DOW components were down.. SPX and NASDAQ was down... so it's quite apparent it's a down day...

Market Internals

Looking at the internals... the DVOL immediately gave away that it was a down day except it ended flat... I won't be surprised if tomorrow is going to be a down monday as well...

Leaders and Laggards

Looking at the main sectors... the telco lead the decliners again... this time round... financials joined in the fun.. the financials were dragged down by the 2 biggest name in the financials, namely JP morgan and Wells Fargo.

Technical Updates

Now all the indices are holding still at the neckline...

Commentaries

|

Commodities

Copper, Silver and Platinum shed more than 1% for the precious metals... While the agriculture commodities were down a lot... with Wheat down 3%, soybean down 1.65% etc... that doesn't look good... There will be a agriculture and wheat report coming out on Monday, so I suppose the market is pricing in for these agriculture commodities...

Treasuries

Treasuries went up!

Weekly Analysis

Week 38

Technical Updates

On a weekly view, both DOW and SPX is holding at their support while NASDAQ is making some moves down...

Commentaries

Weekly Wrap

Dow +2.46 at 13328.85, Nasdaq -5.30 at 3044.11, S&P -4.25 at 1428.59

Today's session got off to a quiet start. The major averages held near their opening levels until the preliminary October University of Michigan Consumer Sentiment Survey registered a reading of 83.1. The survey's best level since September 2007 lifted the major averages to their session highs. However, the exuberance was short-lived as the key indices promptly fell through the unchanged line, to their session lows. The afternoon was generally quiet as the S&P 500 hovered within points of the 1,428 level before settling at 1,428.59, with a loss of 0.3%. Note that today's session punctuated a down week, during which the S&P 500 lost 2.2%.

The financial sector was the biggest laggard of the day. Despite record earnings from two major names, the SPDR Financial Select Sector ETF (XLF 15.81, -0.22) shed 1.4%. JPMorgan Chase (JPM 41.62, -0.48) reported earnings of $1.40 per share against expectations of $1.21. Meanwhile, its revenues were reported at $25.15 billion which was ahead of the expected $24.27 billion. The stock traded higher in initial response to the earnings report, but it settled lower by 1.1%.

Wells Fargo (WFC 34.25, -0.93) slid 2.6% after reporting mixed earnings. WFC exceeded earnings expectations by one cent, while its revenues fell $200 million short of analyst estimates.

Other major financials also showed weakness. Bank of America (BAC 9.12, -0.22) and Morgan Stanley (MS 17.31, -0.55) slipped 2.4% and 3.1%, respectively.

Consumer staple stocks were the top performers of the session. Within the space, Dean Foods (DF 14.94, +0.29) added 2.0% after Stifel Nicolaus upgraded the stock to ‘buy' from ‘hold' with an $18 price target.

Cigarette stocks also showing strength among defensive staple stocks. Philip Morris (PM 91.70, +0.86) and Altria (MO 33.12, +0.41) saw respective gains of 1.0% and 1.3%.

Elsewhere in the space, Monster Beverage (MNST 57.08, +2.64) advanced 4.9% in a rebound from recent weakness.

The Dow Jones Transportation Average outperformed the broader market and settled higher by 0.9%. JB Hunt (JBHT 58.37, +3.58) is the top performer within the space. The freight carrier settled higher by 6.5% after its mixed earnings report showed a top line beat and a slight bottom line miss. Meanwhile, peer CH Robinson (CHRW 59.94, +1.04) added 1.8%. With most transportation stocks on the rise, Overseas Shipholding Group (OSG 5.08, -0.80) was a notable laggard as the shipping stock tumbled 13.6%.

AMD (AMD 2.74, -0.46) slumped 14.4% after the company lowered its third quarter revenue guidance below consensus. Peer Intel (INTC 21.48, -0.20) settled lower by 0.9% while the Market Vectors Semiconductor ETF (SMH 30.50, -0.10) slipped 0.3%.

Overall producer prices rose during September by 1.1%, which was hotter than the 0.8% increase that had been widely forecast. Core producer prices were unchanged which was lower than the Briefing.com consensus call of a 0.2% increase.

The September Treasury Budget showed a $75 billion surplus, which was in-line with expectations.

Next week, the earnings season enters full force as more than 230 companies are scheduled to report their third quarter results.

On Monday, September retail sales, retail sales ex-auto, and the October Empire Manufacturing Index will all be reported at 8:30 ET. In addition, August business inventories will be released at 10:00 ET.

Weekly Review: Markets Cautious Ahead of Third Quarter Earnings

On Monday, equities began the day on a negative note after the World Bank cut its growth projections for the Asian region. Lacking an additional catalyst, the key indices spent the majority of the session trading near their opening levels. A late-day buying surge briefly lifted the S&P 500 and Dow to their session highs, but the bulk of the move was promptly retraced. As a result, the S&P 500 shed 0.3% and the Nasdaq ended with a loss of 0.8%. Marathon Petroleum (MPC 54.30, -0.36) advanced 5.4% after announcing the purchase of BP's Texas City Refinery, related logistics, and marketing assets.

Tuesday's session began on a mixed note before a broad sell-off sent the major averages to their session lows. The weakness started in the technology sector where a slew of companies lowered their third quarter guidance. After reaching their worst levels of the day, the key indices traded sideways until late-day selling coincided with reports the U.S. Attorney in Manhattan filed a civil mortgage fraud lawsuit against Wells Fargo (WFC 34.25, -0.93). The company has since come out and denied any wrongdoing. As a result, the S&P 500 fell 1.0% while the Nasdaq underperformed with a loss of 1.5%.

Wednesday's session got off to a mixed start as the key indices chopped around their respective unchanged lines during the first hour. Sellers took control after traders digested the wholesale inventories data, pushing the major averages to their worst levels. Afternoon trade was mostly quiet as the three averages hovered near session lows. As a result, the S&P 500 finished lower by 0.6%. Alcoa (AA 8.69, -0.08) dipped 4.6% after beating on earnings and revenues. However, the company's third quarter revenue of $5.833 billion represents a 9.1% year-over-year decrease.

On Thursday, equities began the session on a positive note after the weekly initial claims were reported at their lowest level since January 2008. However, the reading of 339,000 may not be entirely comparable to the prior period as one unidentified large state was not included in the total. The early bullish sentiment failed to hold as the major averages reversed during the first hour, and headed for the flat line. As a result, the S&P 500 ended flat. Alpha Natural Resources (ANR 7.88, -0.67) and Arch Coal (ACI 7.62, -0.32) both surged near 16.0%.

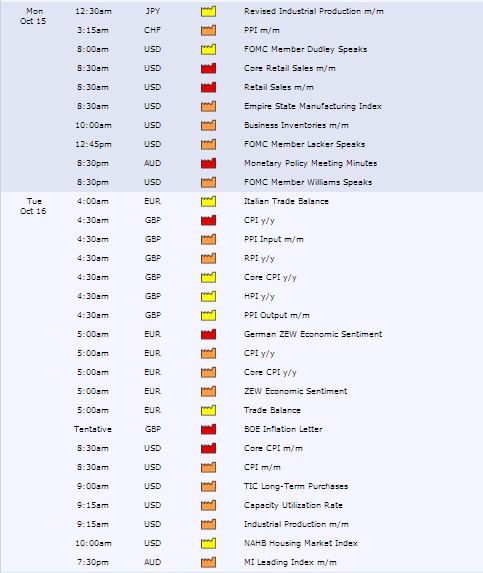

Next Week In View

There will be quite a bit of data coming out next week.. all we need is one bad report to sell the market off... but... it's gonna take a lot of good reports to hold the market above the support... Man... I'm waiting to short the market!

Market Call(Weekly): DOWN

Market Call(15 Oct 2012):Flat to upside

Market Call(15 Oct 2012):Flat to upside

Date: 15 Oct 2012

No comments:

Post a Comment