16 Aug 2013 AMC

Market Summary

Market Internals

Market Internals -Technical-

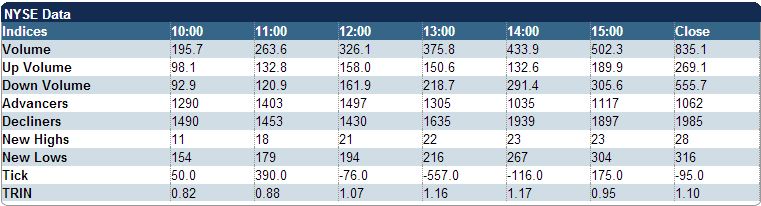

The S&P 500 closed down 5 (-0.33%) at 1656, the Nasdaq closed down 3 (-0.09%) at 3603, and the Dow closed down 31 (-0.20%) at 15081. Action came on mixed volume (NYSE 834 mln vs. avg. of 745; NASDAQ 1459 mln vs. avg. of 1615), with decliners outpacing advancers (NYSE 1072/2019, NASDAQ 1143/1353) and mixed new highs/lows (NYSE 29/341, NASDAQ 49/33).

Relative Strength:

Egypt-EGPT +3.18%, Greece-GREK +2.00%, Shipping-SEA +1.83%, Cotton-BAL +1.42%, Italy-EWI +1.38%, Base Metals-DBB +1.33%, Austria-EWO +1.24%, Spain-EWP +1.10%, Silver-SLV +0.86%, Timber-CUT +0.74%.

Relative Weakness:

India-INP -5.50%, Indonesia-IDX -3.48%, Indian Rupee-ICN -2.59%, Realty Majors-ICF -2.43%, Real Estate-IYR -2.31%, Brazilian Real-BZF -2.12%, Gold Miners-GDX -2.10%, Corn-CORN -1.92%, Volatility-VXX -1.91%, Columbia Index-GXG -1.62%.

Leaders and Laggards

Technical Updates

Commentaries

The stock market fluttered on Friday, trying to bounce back from Thursday's drubbing while at the same time contending with a further rise in the 10-yr note yield, which hit 2.86% at its highest level of the day. The latter got in the way of rebound efforts as the major indices ended this options expiration day modestly lower.

There was evidence in today's session of participants pressing the buy-the-dip trade that has worked so well for so long. That evidence was seen early on in the outperformance of the homebuilding stocks, which have been hit hard of late. Ultimately, though, the strength in homebuilding stocks faded as the yield on the 10-yr note, and concerns about rising mortgage rates, increased.

The on again-off again showing of the homebuilders was representative of the overall action. There just wasn't a lot of conviction on either the buy side or the sell side.

The S&P 500, for its part, danced above and below its 50-day simple moving average (1657/1656), but closed just below that notable support level due to some closing selling interest. Gains in individual stocks like Boeing (BA 103.47, +0.74), Apple (AAPL 502.33, +4.42), American Express (AXP 75.17, +0.29), and United Continental (UAL 30.86, +0.76) offered a measure of support, but clear-cut sector strength was lacking for the most part today.

The transports were about the only area where buying interest was broad-based and semiconductor stocks fared reasonably well after analysts defended Applied Materials (AMAT 15.62, +0.30) following an otherwise disappointing earnings report and fiscal fourth quarter outlook. The Dow Jones Transportation Average increased 0.6% while the Philadelphia Semiconductor Index rose 0.4%.

Retailers were once again on the soft side after Nordstrom (JWN 56.43, -2.90) and Jos. A. Bank (JOSB 41.00, -3.10) joined the roster of retail companies providing earnings warnings. Those warnings weighed most heavily on the apparel companies.

In terms of interest rates, they started out on a pretty subdued path, but selling picked up noticeably around 12:30 p.m. ET. Soon thereafter, CNBC reported that it had been told by a White House source that chances of Larry Summers being nominated for Fed chairman were two in three. That report presumably triggered increased selling interest with participants concerned that Mr. Summers might be more inclined than Janet Yellen (the current Vice Chairman and other leading candidate) to dial back the Fed's asset purchases more readily than Ms. Yellen would be. The selling pressure took the yield on the 10-yr note as high as 2.86% before it settled at 2.84%.

The continued rise in long-term rates continued to take a toll on the high-dividend yielding utilities (-1.1%) and telecom services (-1.0%) sectors, which were the only sectors to lose at least 1.0% today. For the week, the utilities sector dropped 4.4% while the telecom services sector fell 2.3%.

There was another batch of economic data today that included the Housing Starts and Building Permits report for July, the Productivity report for the second quarter, and the University of Michigan Consumer Sentiment report for August. True to recent form, the economic data was uneven.

Housing starts and building permits were basically in-line with expectations, rising 5.9% and 2.7%, respectively, to an annualized rate of 896,000 and 943,000, yet those increases were driven entirely by multi-family units. Starts and permits for single-family homes were down 2.2% and 1.9% from June.

Second quarter productivity increased 0.9% and unit labor costs rose 1.4%. Both numbers were better than expected and both were promptly ignored by the market given the dated nature of the report.

The University of Michigan Consumer Sentiment report, however, captured some of the market's attention with a disappointing headline print of 80.0. That was down from 85.1 in July which, to be fair, was a six-year high. Still, the pullback in the indexes for current conditions and expectations were downers in terms of the report's overall messaging.

With the options expiration today, volume was the heaviest it has been all week with 835 mln shares traded at the NYSE.

Commodities

Closing Commodities: Crude Oil Ends Above $107.50, Gold Closed Above $1350

Commodities continued to display some high volatility in today's session. Crude oil rallied above $108/barrel before dropping back near $106.50/barrel. Ultimately, Sept crude oil ended the day $0.21 higher at $107.55/barrel.

Sept natural gas ended $0.05 lower at $3.37/MMBtu.

Precious metals rallied today, which also included a swift decline in morning activity. Following the morning drop, gold and silver marched higher and ended the day near session highs. Dec gold closed $11.30 higher at $1371.00 and Sept silver closed $0.40 at $23.31/oz.

CBOT Agriculture and Ethanol/ICE

Sugar Closing Prices

·

Dec corn fell 10 cents

to $4.63/bushel

·

Sep wheat fell 6 cents

to $6.32/bushel

·

Nov soybeans fell 6

cents to $12.59/bushel

·

Sep ethanol fell 2 cents

to $2.23/gallon

·

Nov sugar (#16 (U.S.))

fell 0.11 of a penny to 20.33 cents/lbs.

COMEX

Metals Closing Prices

·

Dec gold rose $11.30 to

$1371.00/ounce

·

Sep silver rose $0.40 to

$23.31/ounce

·

Sep copper rose at

$3.36/lb

NYMEX Energy Closing Prices

·

Sep crude oil rose $0.21

to $107.55/barrel

·

Sep natural gas fell 5

cents to $3.37/MMBtu

·

Sep heating oil rose 1

cent to $3.08/gallon

·

Sep RBOB gasoline fell 2

cents to $2.96/gallon

Treasuries

Longer Dated Yields End at Two-Year Highs: 10-yr: -17/32..2.832%..USD/JPY: 1.3334

Treasuries endured heavy selling this week, with most yields marking two-year highs, as relatively in-line economic data continued to fuel the debate over whether or not the Fed will begin tapering its bond buying program as early as the September meeting. Retail sales, CPI, Empire Manufacturing, the Philly Fed, housing starts, and building permits all printed close to analyst expectations, allowing for the debate as to whether or not the economy can stand on its own if the Fed were to pull back its asset purchases. Traders also had to grapple with June TIC flow data that showed the largest outflows from the Treasury market since August 2007 as China and Japan dumped paper.

Selling was pretty well dispersed across the complex as yields in the back half of the curve tacked on at least 20 bps. The benchmark 10-yr yield led the move higher, climbing 25 bps to a fresh two-year high of 2.829%. Even the 5-yr saw an aggressive move higher, adding 20 bps to end Friday's session at 1.569%. Action up front was a little more muted as the 2-yr yield ticked up 4 bps to 0.351% and the 3-yr rallied 10 bps to 0.728%. Aggressive steepening took place along the yield curve as the 2-10-yr spread widened to 248 bps. Elsewhere, precious metals saw a solid weekly advance as gold jumped $41 to $1372 and silver rallied $2.20 to near $23.20. There is no data on Monday.

Treasuries catching a bid into the cash close

2-yr unch @ 99 25/32

3-yr -02/32 @ 99 22/32

5-yr -06/32 @ 99 02/32

7-yr -10/32 @ 98 18/32

10-yr -16/32 @ 97 05/32

30-yr -20/32 @ 96 00/32

On other news....

Slower Economic Growth Expected in

the Third Quarter

The big question is how consumers and businesses will react to an environment with rising interest rates. Most analysts believe that, since interest rates are low relative to historic norms, the increase in rates should not have much of an adverse effect on consumption and investment. Normally, we would disagree. Any type of tightening will cause lower spending, at least on the margins. The latest spending trends, however, suggest that those adverse effects are extremely small and do not impair economic growth.

The housing sector is where rate increases will matter the most. According to our model, a rise in interest rates has an immediate negative effect on sales. That means housing price growth will slow and its subsequent wealth effect on consumption will lessen. Builders also seem concerned about a drop in demand. Single-family construction levels declined in July even though historically low inventories are constraining sales.

Job security has improved notably over the past several months. The initial claims level dropped to its lowest point in nearly 6 years and implies payroll growth in the neighborhood of 200,000 new jobs.

Currencies

Euro Slips in Sleepy Trade: 10-yr:

-23/32..2.854%..USD/JPY: 97.64..EUR/USD: 1.3331

The Dollar Index holds small gains near 81.30 as traders ready for the week's final hour of trading. Current action has the Index sitting on its 100-week moving average, a level that has not seen two consecutive closes below it since February.

The Dollar Index holds small gains near 81.30 as traders ready for the week's final hour of trading. Current action has the Index sitting on its 100-week moving average, a level that has not seen two consecutive closes below it since February.

·

EURUSD is -25 pips at 1.3325 as trade has held

in a narrow 20 pip range throughout the course of U.S. trade. An early bid

failed just short of the important 1.3400 level that corresponds with the June

and August highs, and that has traders shifting their focus back towards minor

support in the 1.3250 area. However, the 1.3200 area remains far more important

as support there is helped by the 50-day moving average. Eurozone data is

limited to German PPI. Click here to see a daily EURUSD

chart.

·

GBPUSD is -20 pips at 1.5620 as trade looks to end two

days of gains. Resistance in the 1.5650 area has held up as sterling bears flex

their muscles in defense of the June highs near 1.5700/1.5750. Key near-term

support holds in the 1.5520 region, and is helped by the 200-day moving

average.

·

USDCHF is +5 pips at .9260 amid a rather sleepy

session, which has seen trade locked in a 20 pip range since this morning. A

breakdown of intraday support in the .9255 area will likely provoke a move back

towards .9230. However, it is the .9200 area that remains critical as help

there dates back to February.

·

USDJPY is +35 pips at 97.60 after early action was

unable to pierce support in the 97.00 area. Bulls are by no means out of the

woods just yet as resistance near 98.00 has help from the 50- and 100-day

moving average. Japan's trade balance will cross the wires Sunday

evening.

·

AUDUSD is +45 pips at .9185 as trade probes the 50-day

moving average. The ability to retake that level will sets up a test of the

important .9300 area. The minutes from the latest Reserve Bank of Australia

meeting will accompany new motor vehicle sales on Sunday evening.

·

USDCAD is +40 pips at 1.0340 as trade action remains

locked in a tight range. The pair has seen a rather choppy trade over the past

month with most of the action trapped between the 50- and 100-day moving

averages. Canada's wholesale sales are due out Monday morning.

Weekly Analysis

Week 33

Technical Updates

Briefing's Commentaries

Weekly Wrap

The week in review for the stock market begins with the week in review for the Treasury market. Specifically, it begins with the yield on the 10-yr note sitting at 2.58% when the week began and ending at 2.84% when the week ended. That move was at the root of why the major averages suffered another losing week, highlighted by the Dow, S&P 500, S&P 400 and Russell 2000 all declining in excess of 2.0%.

It wasn't all about interest rates, though. Increasing worries about the escalating violence in Egypt's political battle, uneven economic data, and disappointing earnings outlooks provided by Macy's (M), Cisco (CSCO), Wal-Mart (WMT) and Nordstrom (JWN) all factored into the broad-based weakness.

The basis for the jump in long-term rates was attributed to concerns that the Federal Reserve is going to announce at its September FOMC meeting a decision to taper its asset purchases. Those concerns were driven by stronger-than-expected reports for retail sales and weekly initial claims, the latter of which fell to its lowest level since October 2007.

Notwithstanding the encouraging signs in those reports, other pieces of data were less convincing as it relates to the prospect of the Fed tapering in September. To that end, it was indicated that industrial production was flat in July, led by a 0.1% decline in manufacturing output, that inflation at both the producer and consumer level remained below the Fed's target rate, that single-family housing starts declined 2.2% in July, and that consumer sentiment measured in the University of Michigan consumer sentiment survey slipped to 80.0 in August from 85.1 in July.

The fact that long-term rates continued to rise in the face of those reports, and declarations from Atlanta Fed President Lockhart and St. Louis Fed President Bullard that the Fed needs more data before making a tapering decision next month, proved to be an intriguing development.

To be sure, there were some irreconcilable messages in the similarly weak showings by the stock and bond markets this week. If there is a true tapering trade in Treasuries, that would be based on the recognition that the economy is strengthening -- something that should be viewed as a positive development by the stock market given the favorable implications for corporate profits. Cisco's and Wal-Mart's guidance in particular, though, undercut that macro view, which leads one to wonder if the weakness in Treasuries could also be a function of concerns that the Fed is losing its grip on things.

In the same vein, the stock market is no doubt grappling with the concern that a rise in long-term rates threatens to slow the economic recovery, and an even bigger concern today in thinking the Fed risks playing with economic fire by tapering in September given the inconclusive messages in the data about economic activity. So, one could argue that the stock market was buffeted by weak guidance at the micro level and concerns the macro picture isn't yet strong enough to handle higher interest rates that come either via the Fed's hand or the market's own hand.

Per usual, time will ultimately tell the tale, but insofar as the past week was concerned, the tale of the tape was one of a decidedly weak picture. Every sector lost ground, with the high dividend-yielding utilities sector taking honors as the biggest laggard with a 4.4% decline. The consumer discretionary, consumer staples, and health care sectors followed behind with losses of 3.3%, 3.2%, and 3.1%, respectively.

The technology sector was the relative strength leader, falling only 0.3%. It has Apple (AAPL) to thank for that. Shares of AAPL surged 10.7% on the news that activist investor Carl Icahn reported a large position in the company and recommended to Apple CEO Tim Cook that the company do a large share buyback.

Over the last two weeks, the S&P 500 has declined 3.2%. On the bright side, it still remains up 16.1% year-to-date.

Next Week In View

Events and conferences of interest:

FOMC Minutes, Jackson Hole Conference to highlight events next week

Events and conferences of interest for next week, Apr 19-24th are listed below. For a complete list of next week's events, please see the events calendar.

Monday

Events and conferences of interest for next week, Apr 19-24th are listed below. For a complete list of next week's events, please see the events calendar.

Monday

·

Chilean Investors Forum

o Scheduled to appear: OAK, APO, MSCI, CS, C

·

MSC2013 Cleveland: Adult

Stem Cell Therapy and Regenerative Medicine

o Scheduled to appear: NBS

·

Masters 2013

o Scheduled to appear: MCHP

Tuesday

·

14th Annual Santander

Conference 5th Palm Oil Summit

o Scheduled to appear: GOL

·

UK 10 Year Bond Auction

Wednesday

·

Morgan Stanley

Semiconductor Corporate Access Day

o Scheduled to appear: SLAB, PSMI, ADNC, IPHI, MTSI

·

2013 Citi One-on-One MLP /

Midstream Infrastructure Conference

o Scheduled to appear: MPC, ACMP, ARLP, ALDW, AMID, APL, ARP, BKEP, BWP, BBEP, BIP, BPL, CLMT, CPLP, CQP, CMLP, UAN, CVRR, DPM, EROC, EPB, EEP, ETP, EPD, EVEP, EXLP, FGP, GEL, HEP, NRGM, KMP, LGCY, LRE, MMP, MWE, MEMP, MCEP, MPLX, NRP, NGL, NKA, NTI, NS, OILT,OKS, PNG, PDH, PVR, PAA, QRE, RGP, RNF, RRMS, SXE, SEP, SMLP, SXCP, SXL, TEP, NGLS, TCP, TGP, TOO, TLLP, TLP, USAC, VNR, WGP, WES, WPZ, XTEX, SXC

·

FOMC

Minutes at 14:00

Thursday

·

Raymond James US Bank

Conference

o Scheduled to appear: SYBT, NPBC, FFIN, BXS, BBCN, HVB, FMBI, RNST, HOMB, TRMK, OZRK, ZION

·

Eurozone PMI Data

·

Jackson

Hole Fed Conference Begins (Thursday - Saturday)

Friday

·

Nothing of Interest

Jason's Commentaries

The market on Friday started with a bullish bias despite Building Permits came in under expectation. However, the market is unable to hold on the the positive side after 12pm ET and started into a sell off and hit a low of 15, 050. After testing the support near 15,000, market reversed in the afternoon and gain back some of the losses which ended the day which a flat to downside day. In the S&P500, we can see that Verizon, Citigroup, Pfzier, Philip Morris were the main laggard with -1.71%, -1%, -1.49% and -1.6% respectively. In the overall sector performance, Utilities once again became the biggest laggard with -1.16%. The Industrials were the only sector performing with a gain of 0.13%. As it's the expiration Friday, volume spiked to 835m shares traded. Which is much lower than the rest of the expiration Fridays. Internals were showing mild bearish sign through the trading session.

For the trading week, it's definitely a washout after breaking the support at 15,400. Moreover, the 50MA has been broken as well, which is likely to point towards a short-term bearishness. However, I do believe that the market is still bullish in the mid term. Right now, the market is heading towards the 61.8% retracement level and I do believe that the market is likely to head up for the next few days ahead of the FOMC Meeting Minutes on Wednesday. Whether the market is likely to hold that support will greatly depends on the FOMC minutes. However, the Jackson Hole Symposium is also happening From Thursday till Saturday which is likely to cause some gyration in the market. I do expect the volume to be hovering around 600m shares traded in the NYSE and the market is likely to remain uncommitted. While recovering from the drastic drop on Thursday, We're likely to see a mild bounce today.

Market Call:FLAT to upside

Date: 19 Aug 2013

No comments:

Post a Comment