23 Aug 2013 AMC

Market Summary

Market Internals

Market Internals -Technical-

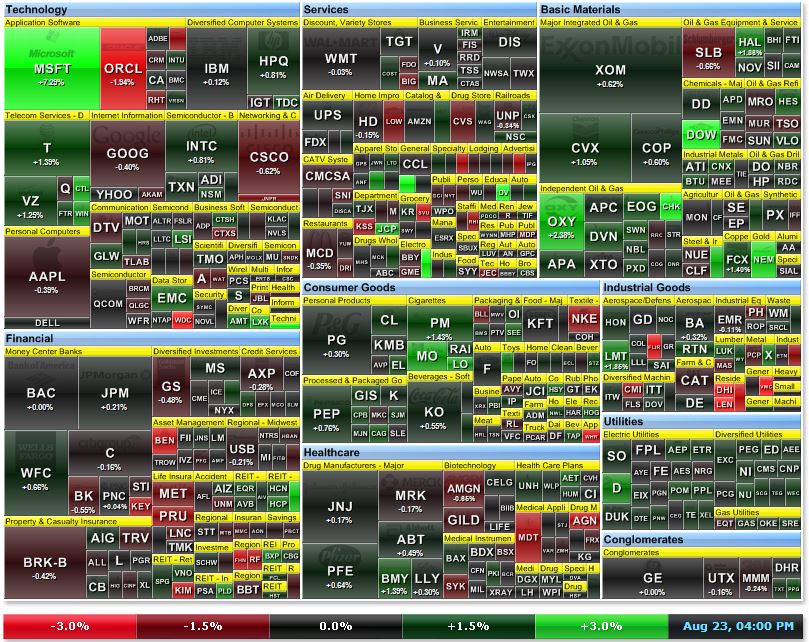

The Nasdaq closed up 19 (+0.52%) at 3658, the S&P 500 closed up 7 (+0.39%) at 1663, and the Dow closed up 47 (+0.31%) at 15010. Action came on below average volume (NYSE 572 mln vs. avg. of 738; NASDAQ 1460 mln vs. avg. of 1588), with advancers outpacing decliners (NYSE 2100/985, NASDAQ 1344/1156) and new highs outpacing new lows (NYSE 65/36, NASDAQ 91/17).

Relative Strength:

Junior Gold Miners-GDXJ +5.43%, Silver-SLV +3.95%, Brazilian Real-BZF +3.28%, Greece-GREK +2.66%, Latin America 40-ILF +2.66%, India-INP +1.97%, BRICs-EEB +1.95%, Rare Earths-REMX +1.64%, Grains-JJG +1.49%, Metals and Mining-XME +1.43%.

Relative Weakness:

U.S. Home Construction-ITB -2.54%, Volatility-VXX -2.12%, Homebuilders-XHB -1.39%, Natural Gas-UNG -1.07%, Vietnam-VNM -1.06%, New Zealand-ENZL -0.63%, Banks-KBE -0.54%, China 25 Index-FXI -0.36%, Thailand-THD -0.32%, Columbia Index-GXG -0.25%.

Leaders and Laggards

Technical Updates

Commentaries

Closing Market Summary: Stocks End Week on Upbeat Note

The major averages registered modest gains and the S&P 500 retook its 50-day moving average. All ten sectors ended in positive territory after a final-hour surge pulled today's underperformers into the green. For the week, the S&P added 0.3%, Nasdaq rose 1.4%, and the Dow shed 0.6%.

Stocks spiked at the open with the technology sector leading the way after Microsoft (MSFT 34.75, +2.36) announced Chief Executive Officer Steve Ballmer will retire from the company within a year. Shares of the software company surged 7.3%, contributing to the outperformance of the Nasdaq, which gained 0.5%.

The S&P followed the opening surge with a brief slip into the red after it was reported that new home sales collapsed in July, falling 13.4% to 394,000 from a downwardly revised 455,000 (from 497,000) in June. The Briefing.com consensus pegged new home sales at 485,000. In terms of percentage, the drop in sales was the largest since May 2010 and brought levels down to their lowest point since October 2012.

Home builders tumbled in reaction to the data and the iShares Dow Jones US Home Construction ETF (ITB 21.07, -0.55) lost 2.5%. This weighed on the discretionary sector, which ended with a razor-thin gain of 0.02%.

Discretionary shares were also pressured by retailers. The SPDR S&P Retail ETF (XRT 78.89, -0.25) lost 0.3% after Aeropostale's (ARO 8.76, -2.22) earnings report continued the recent trend of disappointing results from teen apparel retailers.

Recent weeks have entertained much discussion over when the Federal Reserve will begin cutting back the pace of its asset purchases. While comments from many Fed speakers have suggested the first taper may occur as early as September, their remarks have often included reminders that the Fed intends to remain data-dependent. To that end, today's new home sales report revealed a notable drop-off in sales, which speaks against tapering in the immediate term.

Treasuries, foreign exchange, and precious metals appeared to agree with this assessment as the benchmark 10-yr yield fell seven basis points to 2.82%. The dollar weakened in the wake of the report while gold futures surged 1.9% to $1396.70 per troy ounce. Meanwhile, silver futures spiked 4.3% to $24.04 per troy ounce.

Today's sector leadership was a bit scattered. Three cyclical groups--energy (+0.7%), materials (+0.9%), and technology (+0.6%)--outperformed throughout the day while the remaining three--consumer discretionary (+0.02%), financials (+0.1%), and industrials (+0.1%)--traded in the red until the closing surge.

With regard to countercyclical sectors, rate-sensitive consumer staples (+0.6%), telecom services (+1.4%), and utilities (+0.8%) rallied in reaction to the retreat in yields while health care (+0.2%) lagged.

Today's trading volume was well below average, and with 572 million shares traded at the NYSE, today's total was one million below the tally from yesterday's session that included a three-hour halt of all Nasdaq-listed issues.

On Monday, July durable orders will be reported at 8:30 ET.

Treasuries End Week on Upbeat Note

Leave it to a downbeat piece of economic data to help the Treasury market close the week on an upbeat note. That is what transpired today as the Treasury market was catapulted by a decidedly weak New Home Sales report for July.

Prior to the release of the new home sales data at 10:00 a.m. ET, the Treasury market saw small losses with most of the selling interest persisting in the intermediate to long end of the curve. After the report, though, the trading dynamic changed as selling interest gave way to renewed buying interest.

In terms of the said report, it showed that new home sales declined 13.4% from a downwardly revised annual rate of 455,000 (from 497,000) in June to just 394,000 in July. That was well below the Briefing.com consensus estimate of 485,000, and it marked the largest decline since May 2010. The big, downside surprise was enough to make market participants think a tapering announcement at the September 17-18 FOMC meeting may not be a foregone conclusion. That mentality also manifested itself in the US Dollar Index (81.37, -0.12), which rolled over after the report, as well as in gold futures ($1396.40, +25.60), which spiked in the wake of the weak data.

By and large, the Jackson Hole Symposium didn't create a lot fanfare even if it did provide its share of headlines. Atlanta Fed President Lockhart (non-voter), St. Louis Fed President Bullard (voter), and San Francisco Fed President Williams (non-voter) all did interviews with CNBC this morning. None of them committed to a tapering announcement in September, yet all of them reiterated that incoming data will determine the policy path. Separately, IMF head Christine Lagarde spoke about the risk an exit from unconventional policy poses, yet that was view was presented in a stating-the-obvious kind of way that didn't unnerve the market.

Yields came down across the curve, but longer-dated instruments saw the biggest adjustment with yields dropping four to seven basis points from the 5-year note to the 30-yr bond. The benchmark 10-yr note settled the week at 2.83%, which is exactly where it began the week.

Pre-Market News

Asian markets ended on a mixed note with Japan's Nikkei outperforming (+2.2%) as USDJPY climbed to test the 99.00 level. Elsewhere, China's Shanghai Composite (-0.5%) and Hong Kong's Hang Seng (-0.2%) underperformed. News flow from the region was relatively light, but a researcher from the China Academy of Social Sciences warned the country may once again face liquidity issues during the second half of the year. Economic data was limited to China's foreign direct investment, which increased to 7.1% year-to-date (4.9% prior). Looking at the currencies: USCNY held steady at 6.1210; USDINR is lower near 63.95; USDJPY climbed to 99.08; AUDUSD is lower near .8984.

Asian markets ended on a mixed note with Japan's Nikkei outperforming (+2.2%) as USDJPY climbed to test the 99.00 level. Elsewhere, China's Shanghai Composite (-0.5%) and Hong Kong's Hang Seng (-0.2%) underperformed. News flow from the region was relatively light, but a researcher from the China Academy of Social Sciences warned the country may once again face liquidity issues during the second half of the year. Economic data was limited to China's foreign direct investment, which increased to 7.1% year-to-date (4.9% prior). Looking at the currencies: USCNY held steady at 6.1210; USDINR is lower near 63.95; USDJPY climbed to 99.08; AUDUSD is lower near .8984.

·

In

Japan, the Nikkei advanced

2.2% as discretionary names paced the advance. Isetan Mitsukoshi Holdings, J

Front Retailing, and JTEKT all gained between 5.0% and 6.1%. On the downside,

Tokyo Electric Power Co tumbled 4.9%.

·

Hong

Kong's Hang Seng slipped 0.2%

with retailers leading to the downside. Belle International and Li & Fung

lost 3.5% and 1.5%, respectively. Casino and gaming names outperformed as

Galaxy Entertainment rose 1.8% and Sands China added 0.9%.

·

In

China, the Shanghai Composite

settled lower by 0.5% as financials lagged. China Vanke shed 0.2%.

Major

European indices trade in mixed fashion as the quiet session enters the home

stretch. Economic data was limited as Germany's second quarter GDP increased

0.7% quarter-over-quarter, as expected. In addition, Great Britain's second

quarter GDP was revised up to reflect growth of 0.7% quarter-over-quarter (0.6%

expected, 0.6% previous). Separately, BBA Mortgage Approvals came in at 37.2K

(39.2K expected, 37.3K previous), business investment rose 0.9%

quarter-over-quarter (0.6% forecast, -1.9% prior), and the Index of Services

climbed 0.6% (0.7% consensus, 0.7% previous). Among headlines of note, German

Finance Minister Wolfgang Schaeuble said the Greek economy may enter expansion

next year, but is still likely to need a new aid package that would be much

lower than previous bailouts.

·

Great

Britain's FTSE is higher by 0.5%

as miners contribute to the advance. Antofagasta, Rio Tinto, and Vedanta

Resources are all up between 1.2% and 1.5%. Financials are among the laggards

with HSBC and Standard Life lower by 0.1% and 0.6%, respectively.

·

In

Germany, the DAX is up 0.2% as

Commerzbank leads with a gain of 2.0%. Software company SAP (+1.6%) is also

among the outperformers. Apparel manufacturer Adidas is the weakest performer,

down 1.6%.

·

France's CAC is unchanged. Steelmakers ArcelorMittal and

Vallourec are higher by 1.3% and 1.7%, respectively. Consumer names lag as

L'Oreal and drugmaker Sanofi both sport losses near 1.4%.

Commodities

Closing Commodities: Crude Ends The

Week 0.09% Lower

·

Oct crude oil extended

yesterday's gains as the dollar index weakened. The energy component recovered

into positive territory after trading as low as $104.30 per barrel in morning

pit action. It rose to a session high of $106.94 per barrel and settled with a

1.4% gain at $106.43 per ounce. Despite today's climb, crude oil booked a 0.9%

loss for the week

·

Sep natural gas, on the

other hand, trended lower in negative territory. It pulled back from its

session high of $3.52 per MMBtu and settled with a 1.9% loss at $3.49 per

MMBtu. Still, natural gas gained 3.6% for the week. Precious metals rose

sharply today as economic data showed that July new home sales slid 13.4% to

394,000, thus awakening hope that the Federal Reserve will keep its stimulus in

place

·

Dec gold touched a

session high of $1398.70 per ounce after trading as low as $1367.80 per ounce

earlier in the session. It settled 1.8% higher at $1395.80 per ounce, booking a

1.8% gain for the week

·

Sep silver came off its

low of $23.00 per ounce and settled 3.1% higher at $23.74 per ounce. Today's

rise brought gains for the week to 1.8%

NYMEX Energy Closing Prices

·

Oct

crude oil rose $1.44 to

$106.43/barrel

o Crude oil extended yesterday's gains as the

dollar index weakened. The energy component recovered into positive territory

after touching a session low of $104.30 in morning floor trade. It brushed a

session high of $106.94 and settled with a 1.4% gain. Despite today's rise,

crude oil lost 0.9% over the week.

·

Sep

natural gas fell 6 cents to

$3.49/MMBtu

o Natural gas, on the other hand, trended lower in

negative territory. It pulled back from its session high of $3.52 and settled

slightly above its session low of $3.47, booking a 1.9% loss. Still, natural

gas booked a 3.6% gain for the week.

·

Oct

heating oil rose 3 cents to

$3.10/gallon

·

Oct

RBOB gasoline rose 3 cents to

$2.87/gallon

CBOT Agriculture and Ethanol/ICE

Sugar Closing Prices

·

Dec

corn rose 6 cents to

$4.70/bushel

·

Sep

wheat rose 4 cents to

$6.34/bushel

·

Nov

soybeans rose 38 cents to

$13.26/bushel

·

Sep

ethanol rose 14 cents to

$2.44/gallon

·

Nov

sugar (#16 (U.S.)) rose

0.50 of a penny to 20.90 cents/lbs

Treasuries

On other news....

New Home Sales Collapse in July

New home sales collapsed in July, falling 13.4% to 394,000 from a downwardly revised 455,000 (from 497,000) in June. The Briefing.com consensus pegged new home sales at 485,000. In terms of percentage, the drop in sales was the largest since May 2010 and brought levels down to their lowest point since October 2012. This report is another knock against the NAHB home builders sentiment index, which rose to its highest point since 2006. It is clear that the index is not accurately representing conditions in the new home sector. Inventories rose 4.3% to 171,000 in July from 164,000 in June. With sales down, inventories are now at a 5.2 months' supply after languishing around 4.0 months' supply for most of the year. While we have been advocating for more inventories, we expected it to come from stronger construction numbers and not weakness in sales. Median home prices increased 8.3% to $257,200. Strong price growth will make it difficult to attract potential buyers as higher interest rates and lower employment growth keep affordability conditions down.

Currencies

Weekly Analysis

Week 34

Technical Updates

Briefing's Commentaries

Week in Review: Stocks Chop as Rates Climb

Monday marked the beginning of a new week for the stock market, yet the story played out much the same way it did during the prior week. Long-term rates continued to rise, the stock market continued to sink, and trading volume remained light. The major averages were mixed and little changed for much of the session, but they broke down in late trading as the technology sector gave up its leadership post and other sectors bowed to selling interest. There wasn't a specific news catalyst for the late-day breakdown, which led some to conclude it was a function of technical factors at work. Outside of some specific names, buyers didn't want much to do with the market. The stocks that benefited were familiar names like Boeing (BA 105.48, +0.34), Johnson & Johnson (JNJ 88.41, +0.81), Google (GOOG 870.21, -3.50), and Apple (AAPL 501.02, -1.94).

On Tuesday, the S&P 500 settled higher by 0.4% to snap its streak of four consecutive losses. Small caps outperformed as the Russell 2000 rose 1.5% after registering five declines in a row. Unaffected by another round of losses across emerging markets, stocks climbed at the open, but gains were limited as the S&P could not retake its 50-day moving average. The benchmark index made a brief midday appearance above the key level before spending the entire afternoon just below it. A retreat in Treasury yields contributed to the relative strength of equities as the benchmark 10-yr yield fell seven basis points to 2.82%. The pullback in yields helped rate-sensitive sectors such as telecom services (+0.5%), utilities (+0.8%), and home builders. The iShares Dow Jones US Home Construction ETF added 3.1% as most major builders gained between 2.0% and 4.0% apiece.

Wednesday's session saw the S&P 500 settle lower by 0.6% despite making a brief appearance in positive territory following the release of the FOMC minutes. Although the minutes from the July meeting offered few changes from prior statements, they did indicate broad support for Chairman Bernanke's timeline, which would likely call for tapering as early as September. However, this was coupled with cautious comments regarding the labor market as the minutes noted, "The June employment report showed continued solid gains in payrolls. Nonetheless, the unemployment rate remained elevated, and the continuing low readings on the participation rate and the employment-to-population ratio, together with a high incidence of workers being employed part time for economic reasons, were generally seen as indicating that overall labor market conditions remained weak." Overall, the minutes did not provide a clear-cut signal regarding the Fed's tapering schedule and the mixed reaction across markets suggests a certain level of uncertainty remains present. The reaction in Treasuries was consistent with expectations of tapering in the near-term as the benchmark 10-yr yield jumped four basis points to 2.86%. The selling had the biggest impact on the belly of the curve as the 5-yr yield jumped more than 6 bps to 1.606%. However, the yield still managed to close just below Monday's two-year high.

On Thursday, the major averages registered gains across the board, but a three-hour halt of all Nasdaq-listed issues prevented normal trading from taking place throughout the afternoon. Stocks climbed out of the gate after upbeat survey data from China and the eurozone reassured investors. China's HSBC Manufacturing PMI jumped to 50.1 from 47.7 (48.3 expected) while the eurozone Manufacturing PMI improved to 51.3 from 50.3 (50.8 forecast). In addition, the Services PMI reading rose to 51.0 from 49.8 (50.2 expected). The economic data provided a boost to growth-sensitive sectors as five of six cyclical groups registered gains larger than 1.0%. The technology sector lagged with an advance of 0.5%. The largest sector component, Apple, ended little changed and Dow member Hewlett-Packard (HPQ 22.40, +0.18) endured its worst session in two years, falling 12.5%, after reporting in-line results and saying it is unlikely to experience revenue growth in 2014.

Next Week In View

Jason's Commentaries

Had an awesome weekend with the Young Entrepreneurship Network and was totally burnt out. Ending the night with a horror flim The Conjuring. Finally got my ass back for work.

Got it right for Friday's call for the market. Market started with a bearish bias which reversed after the New Home Sales came in disappointing compared to Consensus. Market rallied after the report was released and stayed flat through the lunch time then finally breaking up higher during the final hour of trading. The main leader on the S&P500 board is Microsoft, gaining a 7.29% after its CEO, Steve Balmer announced his retirement in 12 months. What a mockery to the CEO, i bet he's gonna be real pissed with the market. The gain of Microsoft was able to offset the drop in Oracle which fell 54% on Friday. Other notable gainers are like Dow Chemical, Philip Morris, Altria and Lockheed Martin which gained more than 1.5%. The main leaders in the market were the Materials and the Utilities which gained 0.81% and 0.83% respectively.

Volumes came in pathetic at 544m shares traded on the NYSE. Bulls outpaced the bears slightly and VIX went down 5.28%. Not exactly a bull day actually. It seems that the market is waiting for shorts in the market, or possible sidelined as Sep is approaching, a possible time for Fed's tapering act. On the Technical side of the market, We have the Dow Jones bouncing off its supper with really pathetic NYSE volumes supporting it. This is really very likely to be a dead cat bounce. As for S&P500, it found a support at around the 1645 to 1640 region. However, we're poised for a third candle reversal today. And I'm definitely not gonna be very bullish about it. Furthermore, we do not have much bullishness in the market for a UFUM. S&P500 has closed above its 50MA and Dow Jones is still well below its 100MA. As for Nasdaq 100, it closed above its 20MA.

As for the Treasuries, the treasuries had a major sell off in the week due to the Fed Tapering. If there should be any tapering, the bonds will definitely be the first victim. Perhaps we can short the bonds already? As for the commodities, Crude Oil remained high at the $104 to $107 region.

As for the news coming ahead, we do not have much heavy news this week. We're gonna start the week with the Core Durable Goods Order, Consumer Confidences, Prelim GDP and the Unemployment Claims coming up. The only biggest movers for these reports will be the Prelim GDP report. I'll be expecting the market to consolidate for a while before breaking down strong. It's mixed signs all around the place. Perfect condition for consolidation. The breakdown may come in sudden so stay safe, and stay bear.

Market Call: FLAT to downside

Date:26 Aug 2013

No comments:

Post a Comment