27 Aug 2013 AMC

Market Summary

·

UK's FTSE: -0.8%

·

Germany's DAX: -2.3%

·

France's CAC: -2.4%

·

Spain's IBEX: -3.0%

·

Portugal's PSI: -1.9%

·

Italy's MIB Index: -2.3%

·

Irish Ovrl Index: -2.0%

·

Greece ATHEX Composite: -4.1%

Before Market Opens

Markets

across Asia were broadly lower as fears of Fed tapering and a potential

conflict in Syria weighed. Emerging markets like Indonesia and the Philippines

saw the heaviest selling, closing down 3.7% and 4.0%, respectively. India's

Sensex (-3.2%) saw significant weakness as the rupee tumbled to yet another

record low against the greenback. While the remainder of the region was mostly

lower, China (+0.3%) and Australia (+0.1%) saw late day reversals into the

green following comments from China's vice finance minister suggesting the

Middle Kingdom remained on track for 7.5% growth and that there was no need for

more stimulus. Data out overnight saw Hong Kong's trade deficit narrow to

HKD37.2 billion (HKD45.0 billion expected, HKD49.7 billion previous), the

Philippines' trade deficit shrink to $0.37 billion ($0.46 billion expected,

$0.37 billion previous), and South Korea's consumer confidence hold at 105.

·

In

Japan, the Nikkei closed

lower by 0.7% as the stronger yen weighed. Heavyweight Fast Retailing lagged

the broader market, posting a loss of 1.4%. Elsewhere, Nissan Motor and Honda

Motor were also weak, falling 1.4% and 0.9%, respectively.

·

Hong

Kong's Hang Seng shed 0.6% as

trade settled on the 100-day moving average. Rail operator MTR outperformed

with a 1.1% gain after its earnings beat.

·

In

China, the Shanghai Composite

added 0.3% as shares climbed to their best level in two weeks. China Southern

Airlines rallied 3.0% despite posting disappointing results. Meanwhile, China

Eastern Airlines surged 10.0% in anticipation of Friday's earnings release.

Major

European indices hover near their lows as the cautious session continues.

Today's economic data was limited to Germany's Ifo Business Climate Index,

which ticked up to 107.5 from 106.2 (107.0 expected) as the Current Assessment

rose to 112.0 from 110.1 (110.9 forecast) while Business Expectations increased

to 103.3 from 102.4 (103.0 expected). Also of note, Italy and Spain conducted

solid short-term debt auctions despite the safety bid that was in place

overnight.

·

Great

Britain's FTSE is lower by 0.6% as

financials underperform. Lloyds Banking Group, Royal Bank of Scotland, and

Standard Chartered are all down between 2.3% and 3.6%. On the upside, oil

company Petrofac is higher by 9.1% after comments from the Chief Executive

Officer who said the company is on pace to meet its 2015 profit targets.

·

In

France, the CAC trades down

1.5% as nearly all components post losses. Exporter Renault leads to the

downside with a loss of 3.4%. Financials are also weak with BNP Paribas and

Credit Agricole down 2.1% and 3.1%, respectively.

·

Germany's DAX holds a loss of 1.6% as 29 of 30 index

members trade lower. Commerzbank and steelmaker ThyssenKrupp lead weigh with

respective losses of 3.1% and 3.0%. Chemical producer Lanxess is the lone

advancer as the stock sports a slim gain of less than 0.1%.

European Markets Closing Prices

European markets are now closed; stock markets across Europe performed as

follows:

Market Internals

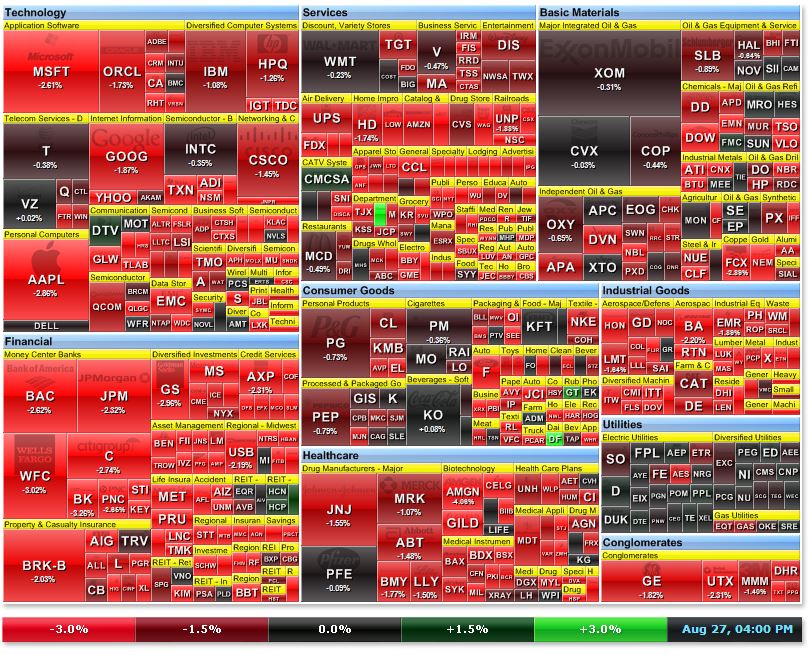

Market Internals -Technical-

The Nasdaq closed down 79 (-2.16%) at 3579, the S&P 500 closed down 26

(-1.59%) at 1630, and the Dow closed down 170 (-1.14%) at 14776. Action came on mixed volume (NYSE 683 mln vs. avg. of 736;

NASDAQ 1591 mln vs. avg. of 1588), with decliners

outpacing advancers (NYSE

620/2481, NASDAQ 322/2225) and new

lows outpacing new highs (NYSE

14/80, NASDAQ 29/31).

Relative Strength:

Volatility-VXX +8.11%, Gasoline-UGA +2.78%, Heating Oil-UHN +2.45%, Oil-USO

+2.40%, Japanese Yen-FXY +1.42%, Commodities-GSG +1.26%, Brazilian Real-BZF

+0.71%, Swiss Franc-FXF +0.49%, Canadian Dollar-FXC +0.29%.

Relative Weakness:

Indonesia-IDX -7.60%, India-INP -6.83%, Turkey-TUR -6.34%, Junior Gold

Miners-GDXJ -5.20%, Greece-GREK -4.99%, Thailand-THD -4.95%, Biotechnology-XBI

-3.83%, Silver Miners-SIL -3.73%, Clean Energy-PBW -3.68%, Regional Banks-KRE

-3.37%.

Leaders and Laggards

Technical Updates

{kind=link}

{kind=link}

{kind=link}

Briefing's Commentaries

Closing Market Summary: Stocks Slump as

Geopolitical Concerns Weigh

The major averages settled on their lows after broad-based selling persisted

throughout the session. Sellers were in control, reacting to the increased

likelihood of U.S. military involvement in Syria.

In addition, investors exhibited caution amid news indicating the debt ceiling

will be reached in mid-October and that Congress has yet to begin budget

negotiations ahead of the new fiscal year, which begins October 1.

The S&P 500 fell 1.6% to end below its 100-day moving average for just the

second time this year. Small caps endured even more selling as the Russell 2000

lost 2.4%.

Global equities sold off ahead of the U.S. open while commodities received an

overnight bid that held throughout the session. Concerns over possible supply

interruptions helped crude oil end at its highest level in more than a year,

climbing 2.8% to $108.84 per barrel. Elsewhere, gold futures rose 1.6% and

silver advanced 2.0% to $1415.50 and $24.50 per troy ounce, respectively.

Similar to oil and precious metals, Treasuries were on the receiving end of

safe-haven flows with the benchmark 10-yr yield sliding eight basis points to

2.72%.

The retreat in yields helped rate-sensitive telecom services and utilities end

little changed. However, other sectors were not as fortunate as six groups lost

more than 1.0%, and two of those six fell more than 2.0% apiece.

Intraday rebound attempts never gathered steam as two top-weighted sectors,

financials and technology, led to the downside with respective losses of 2.4%

and 2.0%. The weakness in technology was notable as the sector had provided

notable leadership in recent days.

Elsewhere, industrials also finished among the laggards as

transportation-related companies underperformed. The Dow Jones Transportation

Average fell 2.6% as airlines displayed significant weakness. Delta Air Lines (DAL 19.11, -1.16) and United Continental (UAL 27.71, -2.15) tumbled 5.7% and

7.2%, respectively.

While most cyclical sectors ended behind the broader market, the energy space

outperformed with a loss of 0.6% as the surge in crude contributed to the

sector's strength.

Broad losses across the major averages sent the CBOE Volatility Index (VIX 16.76, +1.77) to its highest

level since early July as investors scrambled to buy protection.

Today's session was the most active since August 16, and fifth most active this

month, as 683 million shares changed hands on the floor of the New York Stock

Exchange.

Looking back at the day's economic data, consumer confidence improved in August

as the Conference Board's Consumer Confidence Index increased to 81.5 from an

upwardly revised 81.0 (from 80.3) in July. The Briefing.com consensus expected

the index to fall to 77.0.

A sharp drop in equity prices along with weak payroll growth were expected to

weigh on the Consumer Confidence Index. Instead, confidence strengthened on the

back of better layoff numbers and generally positive economic media reports. It

is unlikely that confidence will improve again in September. Heated budget and

debt ceiling negotiations took their toll on sentiment indicators in 2011. As

the media once again highlights the negative effects of a potential default or

government shut down, sentiment will probably decline.

Separately, the June Case-Shiller 20-city Home Price Index rose 12.1% while a

12.0% increase had been expected by the Briefing.com consensus. This follows

the previous month's increase of 12.2%.

Tomorrow, the weekly MBA Mortgage Index will be reported at 7:00 ET and July

pending home sales will cross the wires at 10:00 ET.

Commodities

Closing Commodities: Crude Oil, Precious Metals Gain on

Syria Concerns, Weaker Dollar Index

A weaker dollar index and increased concerns over possible military action

against Syria gave crude oil and precious metals a boost today.

·

The biggest gain came

from Oct crude oil as the energy component climbed to a new high of the year of

$109.32 per barrel, extending gains for a fourth consecutive session. It

chopped around near the $109.00 per barrel level for most of today's floor

trade and settled there with a solid 3.0% gain.

·

Dec gold traded as high

as $1424.00 per ounce, its highest level since June. It booked a 2.0% gain as

it closed at $1420.20 per ounce. Sep silver also advanced today and touched a

session high of $24.70 per ounce. It eventually settled 2.8% higher at $24.66

per ounce.

·

Oct natural gas began

floor trade in negative territory, trading as low as $3.48 per MMBtu. However,

it climbed higher and erased earlier losses, closing with a 0.3% gain at $3.57

per MMBtu.

NYMEX Energy Closing Prices

·

Oct

crude oil rose $3.21 to

$109.00/barrel

o Crude oil climbed to a new high this year of

$109.32, extending gains for a fourth consecutive session. The rise came on a

weaker dollar index and increased supply concerns due to possible U.S. military

action against Syria. Crude oil chopped around near the $109.00 level for most

of today's floor trade and eventually settled with a 3.0% gain.

·

Sep

natural gas rose 1 cent to

$3.57/MMBtu

o Natural gas came off its session low of $3.48

set at pit trade open and climbed higher as the session progressed. It managed

to erase earlier losses and settled 0.3% higher.

·

Oct

heating oil rose 9 cents to

$3.17/gallon

·

Oct

RBOB gasoline rose 9 cents to

$2.92/gallon

CBOT Agriculture and Ethanol/ICE

Sugar Closing Prices

·

Dec

corn fell 15 cents to

$4.86/bushel

·

Sep

wheat fell 4 cents to

$6.51/bushel

·

Nov

soybeans fell 17 cents to

$13.73/bushel

·

Sep

ethanol fell 3 cents to

$2.47/gallon

·

Nov

sugar (#16 (U.S.)) fell

0.18 of a penny to 20.62 cents/lbs

COMEX Metals Closing Prices

·

Dec

gold rose $27.20 to

$1420.20/ounce

o Gold rose to its highest level since June on

increased tension over Syria and the increased likelihood of U.S. military

action in the region. The yellow metal booked a 2.0% gain as it settled

slightly below its session high of $1424.00.

·

Sep

silver rose $0.66 to

$24.66/ounce

o Silver also traded higher today, climbing as

high as $24.70. It eventually settled with a solid 2.8% gain.

·

Sep

copper rose 1 cent to $3.33/lbs

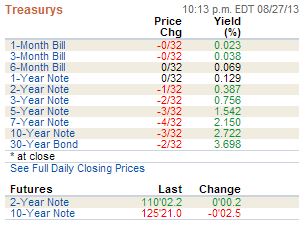

Treasuries

Treasuries See Safety Bid as Potential Conflict

with Syria Looms: 10-yr: +20/32..2.721%..USD/JPY: 97.00..EUR/USD: 1.3388

Treasuries booked solid gains as overnight buying that developed on worries of

a conflict in Syria persisted throughout the session, leading to a third

straight day of gains. The complex climbed in the face of better than expected

economic data as both the Case-Shiller 20-city Index (12.1% actual v. 12.0%

expected) and consumer confidence (81.5 actual v. 77.0 expected, 81.0 previous)

posted better than expected results, providing more fuel to the argument the

Fed will begin tapering its asset purchase program later this year. Maturities

remained near their best levels of the session ahead of this average

afternoon's $34 bln 2-yr note auction, and climbed to fresh highs as its

results were digested. The auction drew 0.386% and a weak 3.21x bid/cover

(12-auction average 3.53x) that still managed to be the best since April

(3.63x). Light indirect bidder participation (19.3%) was countered with an

average direct takedown (26.1%), leaving primary dealers with 54.6% of the

supply. Yields at the long end of the curve ended the day down more than 8 bps

apiece as the 10-yr slipped below 2.735% support, closing at 2.721%. The

inability to regain the support in a timely matter will have Treasury bulls

trying to press the 50-day moving average near 2.605%. The benchmark yield last

closed below the 50-day in early May, just as the sell off was beginning to

take hold. Today's bid

produced aggressive flattening along the yield curve as the 2-10-yr spread

narrowed to 235.5 bps. Elsewhere,

a solid bid across the metals complex saw gold rally $24 to $1417 and silver

climb $0.55 to near $24.55. Wednesday's

data is limited to the weekly MBA Mortgage Index (7) and pending home sales

(10). Treasury will hold

a $35 bln 5-yr note auction

Yields slip to fresh lows

2-yr -1.6 bps @ 0.360%

3-yr -5.1 bps @ 0.729%

5-yr -7.7 bps @ 1.515%

7-yr -8.6 bps @ 2.124%

10-yr -7.8 bps @ 2.713%

30-yr -7.9 bps @ 3.688%

{kind=link}

Next Day In View

Economic Commentary

On other news....

Currencies

Dollar Nears Test of Key Support:

10-yr: +23/32..2.725%..USD/JPY: 97.05..EUR/USD: 1.3390

The Dollar Index holds on session lows near 81.15 after sellers took control

following this morning's better than expected data. Today's weakness has the

Index on track to close at its worst level in a week, with action once again

nearing a test of key support in the 80.80/81.00 area. Click here to see a daily Dollar

Index chart.

·

EURUSD is +25 pips at 1.3395 as trade holds just below

session highs. The single currency has tested the 1.3400 level

throughout much of August, but has only registered one close above the mark. Early

selling was unable to pierce minor support in the 1.3325 area. Eurozone data

out tomorrow includes GfK German Consumer Climate and M3 money supply.

·

GBPUSD is -40 pips at 1.5535 as trade pushes lower for

the fourth time in five days. Sterling saw an early test of the 200-day moving

average, but was able to hold that level as buyers emerged near 1.5500. Both

the 50- and 100-day moving averages should provide some help on a move into the

1.5350 region. British data is limited to CBI Realized Sales. Bank of

England Governor Mark Carney will speak tomorrow in Nottingham.

·

USDCHF is -50 pips at .8975 as trade probes key support

in the area. Traders are watching today's action closely as a finish below

.9170 would mark the worst for the pair since February.

·

USDJPY is -145 pips at 97.00 as trade tests support at

the level. Today's weakness comes as sellers defend trendline resistance off

the May highs that is helped by the 50- and 100-day moving averages. A test of

the 200-day moving average (94.45) cannot be ruled out if current levels are

broken.

·

AUDUSD is -50 pips at .8975 as action has rallied off

session lows. The hard currency dipped below the .8935 level earlier this

morning, but has since managed to retake minor support at the level. A close

below .8900 marks the worst in over three years. Australia's construction work

done is due out this evening.

·

USDCAD is -10 pips at 1.0490 has action has seen a significant

reversal off session highs. A slip below the 1.0475 level will surely

provoke the bulls to come out in defense of the 50-day moving average near

1.0400.

Jason's Commentaries

It was definitely way past my expectation. Was only expecting the market to go down slightly, but it came down more than 170 points on the Dow last night. What a total washout. The market started with a very bearish sentiment with more than a drop of 0.8% on the futures before the market open. Despite good economic results, the market did not manage to regain any ground. Once again, it's a sea of red in the market last night. Notable events would be the debt ceiling issue and US's possible military involvement in Syria. US always want to have some war to bail them out from their debts. let's see the US military will start a war in Syria. Financials and the Industrials were the worst laggard in the market last night with more than 1.7% drop. Volumes were 682m shares traded on the NYSE, which is significantly higher and the rest of the trading sessions in the past 2 weeks. All internals were pointing to the downside. However, it was definitely oversold and i'm expecting some slight bounce in the market soon. However we do not have any significant support level to provide the bounce yet.

Market Call: Flat to downside

Date: 28 Aug 2013

No comments:

Post a Comment