9 Aug 2013 AMC

Market Summary

Market Internals

The Dow closed down 73 (-0.47%) at 15426, the S&P 500 closed down 6 (-0.36%) at 1691, and the Nasdaq closed down 9 (-0.25%) at 3660. Action came on below average volume (NYSE 637 mln vs. avg. of 765; NASDAQ 1502 mln vs. avg. of 1642), with decliners outpacing advancers (NYSE 1488/1559, NASDAQ 995/1510) and new highs outpacing new lows (NYSE 131/109, NASDAQ 124/23).

Relative Strength:

Silver Miners-SIL +4.50%, Copper Miners-COPX +3.89%, Steel-SLX +3.36%, Peru-EPU +3.29%, Coal-KOL +3.24%, Metals and Mining-XME +2.88%, Chile-ECH +1.49%, Greece-GREK +1.16%, BRICs-EEB +1.02%, Australian Dollar-FXA +0.88%.

Relative Weakness:

Natural Gas-UNG -2.51%, Corn-CORN -1.63%, Rare Earths-REMX -0.94%, India-INP -0.86%, Grains-JJG -0.80%, Poland-EPOL -0.73%, Utilities-XLU -0.69%, Taiwan-EWT -0.68%, Thailand-THD -0.66%, South Korea-EWY -0.56%.

Leaders and Laggards

Technical Updates

Commentaries

Stocks End Down Week on Lower Note

Sector Performance (%

change of the day): Financials (-0.28%),

Tech (-0.44%), Health Care (-0.34%), Consumer Staples (-0.44%), Consumer

Discretionary (-0.28%), Industrials (-0.29%), Energy (-0.49%), Telecom

(-1.00%), Materials (+0.57%), Utilities (-0.68%).

Dow -0.5%, S&P 500

-0.4%, Nasdaq -0.3%, Nasdaq 100 -0.4%, S&P 400 +0.1%, Russell 2000 -0.1%

The major averages ended

a down week on a lower note as the S&P 500 shed 0.4% to widen this week's

loss to 1.1%. Shortly after opening in the red, the benchmark index briefly

turned positive, but just like yesterday, it was unable to make a sustained

move above the 1,700 level. The S&P notched its low as the European session

ended before erasing about half of its losses over the course of the afternoon.

Nine of ten sectors

ended in the red while materials outperformed with a gain of 0.6% after China's

industrial production report surpassed estimates (9.7% actual, 9.0% forecast).

Steelmakers and miners rallied broadly, but Molycorp (MCP

6.69, -0.72) headed in the opposite direction after missing on earnings and

revenue. The materials sector was the only group that registered a gain this

week, rising 0.8%.

Other commodity-linked

sectors did not fare as well. Energy underperformed with a loss of 0.5% even as

crude oil advanced 2.5% to $106.02 per barrel. Meanwhile, the industrial sector

(-0.3%) ended slightly ahead of the S&P, but transportation companies

underperformed as the Dow Jones Transportation Average shed 0.6%.

Meanwhile, the remaining

cyclical groups ended in mixed fashion. Technology (-0.4%) underperformed while

financials (-0.3%) and discretionary shares (-0.3%) settled ahead of the

broader market. The discretionary sector received some support from Priceline.com (PCLN

969.89, +36.14) after the company beat on earnings and revenue.

With regard to

countercyclical groups, health care (-0.4%) and consumer staples (-0.4%) did

not deviate from the S&P while rate sensitive utilities (-0.7%) and telecom

services (-1.0%) lagged.

Treasuries were very

quiet today and the benchmark 10-yr yield slipped one basis point to 2.58%

after spending the day in a three point range.

Light volume persisted

throughout the week and today was no different as less than 650 million shares

changed hands on the floor of the New York Stock Exchange.

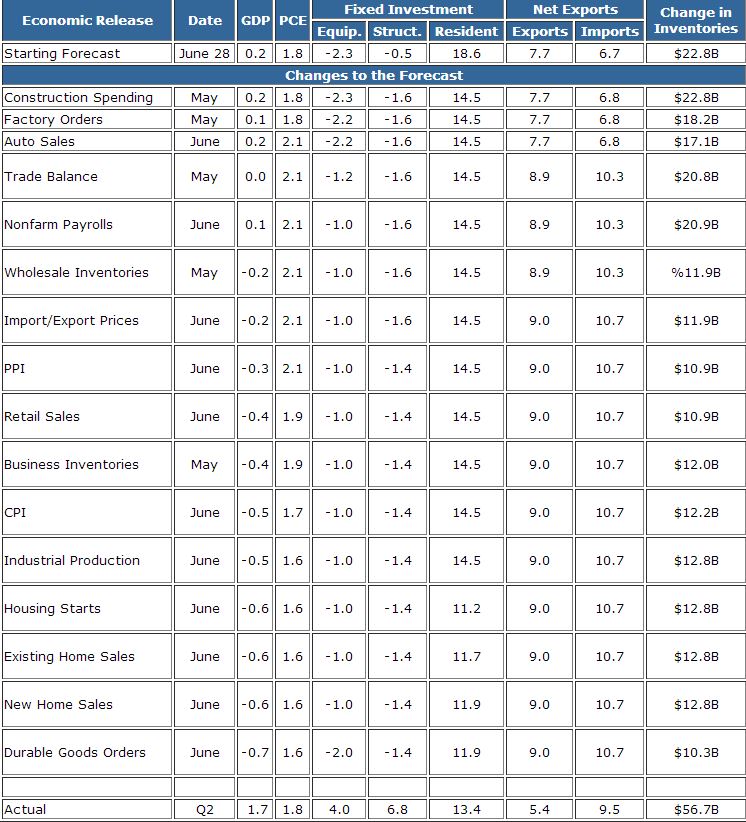

Today's economic data

was limited to wholesale inventories, which fell 0.2% in June after declining a

downwardly revised 0.6% (from -0.5%) in May. That was the third consecutive

monthly decline and the fourth monthly drop so far in 2013. The Briefing.com consensus

expected wholesale inventories to increase 0.4%.

The Bureau of Economic

Analysis assumed that wholesale inventories were flat in June in the advance

estimate for second quarter GDP growth. The downward surprise will add a minor

negative contribution to the revisions in the second estimate.

On Monday, the July

Treasury budget will be released at 14:00 ET.

Commodities

Dec corn fell 7 cents to

$4.53/bushel

Sep wheat fell 7 cents

to $6.34/bushel

Nov soybeans fell 1 cent

to $11.83/bushel

Sep ethanol settled fell

$0.04 to $2.14/gallon

Dec gold rose $2.10 to

$1312.00/ounce

Sep silver rose $0.21 to

$20.41/ounce

Sep copper rose 4 cents

to $3.31/lb

Treasuries

Treasuries See Mixed Week: Treasuries saw a mixed week as better than expected data and Fed chatter of potential tapering as early as the September meeting moved markets. ISM Services (56.0 actual v. 53.2 expected), the trade balance (-$34.2 bln actual v. -$43.4 bln expected), and initial claims (333K actual v. 340K expected) all exceeded estimates. The run of better than expected data produced more Fed chatter that a tapering of its bond buying program may begin as soon as the September meeting. Chicago Fed President Charlie Evans and Cleveland Fed President Sandra Pianalto were the latest to join the chorus of Fed Presidents who have begun discussing the possibility the Fed will begin tapering its asset purchase program later this year. However, St. Louis Fed chief James Bullard as a little more dovish, suggesting the central bank should take a wait and see approach as more data is needed before a decision is made.

Light selling upfront caused the 2- and 3-yr yields to rise while the back half of the curve posted modest gains, pushing those yields lower. The 3-yr was the loser for the week as selling ran its yield up 4 bps to 0.614% by Friday's cash close. Meanwhile, a modest bid in the belly pushed those yields down close to 3 bps apiece as settled the week at 2.580%, near a two-week low. Traders continue to watch this area closely as minor support rests in the vicinity. The long bond was the winner as a solid bid dropped its yield 5 bps to 3.639%, pushing action back below the 200-week moving average. This week's action flattened the yield curve as the 2-10-yr spread narrowed to 226.5 bps. Elsewhere, precious metals saw a mixed week as gold was flat at $1315 and silver rallied $0.55 to $20.50. Monday's data is limited to the Treasury budget (14).

On other news....

Reviewing

overnight developments:

·

Asian markets ended mostly higher. Japan's Nikkei +0.1%, China's

Shanghai Composite +0.4%, Hong Kong's Hang Seng +0.7%.

o In

regional economic data:

§ China's

CPI rose 2.7% year-over-year (2.8% expected, 2.7% prior) while the

month-over-month reading ticked up 0.1%, as expected. In addition, PPI

decreased 2.3% year-over-year (-2.2% expected, -2.7% prior). Separately, retail

sales increased 13.2% year-over-year (13.5% consensus, 13.3% previous),

industrial production rose 9.7% year-over-year (9.0% forecast, 8.9% prior), and

fixed asset investment jumped 20.1% year-over-year (20.0% expected, 20.1%

previous).

§ Japan's

Household Confidence slipped to 43.6 from 44.3 (45.3 expected) while the

Tertiary Industry Activity Index came in at -0.3% (-0.2% expected, 1.3%

previous). In addition, the M2 money stock increased 3.7% year-over-year (3.8%

consensus, 3.8% prior).

o In

news:

§ The

Reserve Bank of Australia lowered its 2013 GDP growth target by 25 basis points

to 2.25%. The central bank expects GDP growth to reach 3.5% as early as

2015.

·

Major European indices trade in mixed fashion. Great Britain's

FTSE +0.3%, Germany's DAX -0.1%, and France's CAC -0.2%.

o Notable

economic data was limited:

§ Great

Britain's trade deficit narrowed to GBP8.08 billion from GBP8.67 billion

(-GBP8.50 billion expected). In addition, the CB Leading Index slipped 0.2%

month-over-month (0.4% previous).

§ France

reported a government budget deficit of EUR59.3 billion (-EUR72.6 billion

prior) and its industrial production declined 1.4% month-over-month.

§ Italian

trade surplus narrowed to EUR3.62 billion from EUR3.93 billion (EUR4.22 billion

consensus).

o Looking

at news:

§ Italy's

Prime Minister Enrico Letta warned that the lack of a rebound in jobs poses the

biggest risk to economic recovery.

In U.S.

corporate news:

·

Molycorp (MCP 6.60, -0.81) is -10.9%

after missing on earnings and revenue.

·

NVIDIA (NVDA 14.25, -0.45) is

-3.1% after the company's cautious guidance overshadowed its earnings beat on

in-line revenue.

·

Priceline.com (PCLN 991.63, +57.88)

is +6.2% after reporting a bottom-line beat.

S&P

futures point to a modest decline at the open, trimming some of their earlier

losses. Bulls will have their sights set on retaking the 1700 level ahead of

the week as the ability to do so would mark a second consecutive weekly close

above the psychologically important mark.

The major averages in Asia were firm after Chinese data mostly outpaced estimates. While pricing pressures were a bit cooler than anticipated (CPI 2.7%, PPI -2.3%), fixed asset investment (20.1%), industrial production (9.7%), and new loans (CNY700 bln) all posted better than anticipated results, helping China's Shanghai Composite to a gain of 0.4%. Even Japan's Nikkei (+0.1%) ended in the green, but still saw its sharpest weekly decline in two months. Something to keep an eye on is the continued strength in the Australia dollar as trade tests minor resistance in the .9150 region. A move through that level sets up a test of the key .9300 area. Markets across much of the region were shuttered for holiday as India, Indonesia, Malaysia, the Philippines, and Singapore enjoy a long weekend.

Moving to Europe, most of the major averages hold little changed. Britain's FTSE (+0.4%) is outperforming after the run of better than expected data continued following the release of the country's trade balance (-GBP8.1 bln actual v. --GBP8.4 bln expected). While the rest of the region is flat, Italy's MIB (-0.3%) is lagging behind. The quiet trade has carried into both sovereign debt markets and the foreign exchange complex as both are seeing little deviation from their respective flat lines.

Shifting focus back to the U.S., a flat trade across most of the Treasury complex has yields hovering little changed with the 10-yr near 2.585%. The long bond is outperforming with a modest bid pushing its yield down 3 bps to 3.642%. Meanwhile, the Dollar Index is unchanged at 81.00. Notable is the greenback's weakness against the Australian dollar (AUDUSD +65 pips @ .9165) and Japanese yen (USDJPY -40 pips @ 96.20). MCP, NVDP, PCLN are among the names in focus following the release of their quarterly results...The following are the most important factors influencing the market this morning:

The major averages in Asia were firm after Chinese data mostly outpaced estimates. While pricing pressures were a bit cooler than anticipated (CPI 2.7%, PPI -2.3%), fixed asset investment (20.1%), industrial production (9.7%), and new loans (CNY700 bln) all posted better than anticipated results, helping China's Shanghai Composite to a gain of 0.4%. Even Japan's Nikkei (+0.1%) ended in the green, but still saw its sharpest weekly decline in two months. Something to keep an eye on is the continued strength in the Australia dollar as trade tests minor resistance in the .9150 region. A move through that level sets up a test of the key .9300 area. Markets across much of the region were shuttered for holiday as India, Indonesia, Malaysia, the Philippines, and Singapore enjoy a long weekend.

Moving to Europe, most of the major averages hold little changed. Britain's FTSE (+0.4%) is outperforming after the run of better than expected data continued following the release of the country's trade balance (-GBP8.1 bln actual v. --GBP8.4 bln expected). While the rest of the region is flat, Italy's MIB (-0.3%) is lagging behind. The quiet trade has carried into both sovereign debt markets and the foreign exchange complex as both are seeing little deviation from their respective flat lines.

Shifting focus back to the U.S., a flat trade across most of the Treasury complex has yields hovering little changed with the 10-yr near 2.585%. The long bond is outperforming with a modest bid pushing its yield down 3 bps to 3.642%. Meanwhile, the Dollar Index is unchanged at 81.00. Notable is the greenback's weakness against the Australian dollar (AUDUSD +65 pips @ .9165) and Japanese yen (USDJPY -40 pips @ 96.20). MCP, NVDP, PCLN are among the names in focus following the release of their quarterly results...The following are the most important factors influencing the market this morning:

·

·

Europe: FTSE +0.4%, CAC -0.1%, DAX -0.1%, MIB -0.2%, IBEX +0.3%

Europe: FTSE +0.4%, CAC -0.1%, DAX -0.1%, MIB -0.2%, IBEX +0.3%

o Notable

economic data was limited:

§ Great

Britain's trade deficit narrowed to GBP8.08 billion from GBP8.67 billion

(-GBP8.50 billion expected). In addition, the CB Leading Index slipped 0.2%

month-over-month (0.4% previous).

§ France

reported a government budget deficit of EUR59.3 billion (-EUR72.6 billion

prior) and its industrial production declined 1.4% month-over-month.

§ Italian

trade surplus narrowed to EUR3.62 billion from EUR3.93 billion (EUR4.22 billion

consensus).

Looking at news:

§ Italy's

Prime Minister Enrico Letta warned that the lack of a rebound in jobs poses the

biggest risk to economic recovery.

·

India revokes patents on AGN eye drugs Ganfort

and Combigan, according to reports

·

JCP Chairman Thomas Engibous

issues statement: CEO search process began three weeks ago; will be careful and

deliberate

·

JPM may face an increased

investigation of Bear Sterns MBS, according to reports

·

PCLN second quarter gross

travel bookings for the Group were $10.1 billion, an increase of 38.0% over a

year ago

·

ITC is set to rule if SSNLF has infringed

on AAPL's patents, according to reports

·

VZ gains FDA clearance

for remote health monitoring solution

·

Borrowers will be allowed to sue WFC over

mortgages, according to report

Earnings/guidance of interest:

·

MCP is -10.9% after missing on

earnings and revenue.

·

NVDA is -3.1% after the

company's cautious guidance overshadowed its earnings beat on in-line

revenue.

·

PCLN is +6.2% after

reporting a bottom-line beat.

Select analyst actions

of interest:

·

Upgrades: CSCO upgraded

to Neutral from Underweight at JPMorgan

·

Downgrades: LINE downgraded

to Underperform from Perform at Oppenheimer, FL downgraded to

Neutral from Buy at Goldman, DE Deere downgraded to Sell from

Neutral at UBS

Technical factors: At least some corrective trade was due

for the S&P in the wake of the three day slide and the ability to recoup

all of the first hour pullback was favorable. For the short term as long as it

is able to maintain a posture above the 1693/1692 support and the early low

(1688) it will remain in a constructive position. Resistance is at 1701/1703

prior to the 1708/1709 zone.

Looking ahead: Wholesale inventories will cross the wires at 10am ET. CDXS, OMER, ZOLT will report after the close while CRNT, GSS, PERI, SPR, SRT, SYY are scheduled to release their quarterly results ahead of Monday's open.

Looking ahead: Wholesale inventories will cross the wires at 10am ET. CDXS, OMER, ZOLT will report after the close while CRNT, GSS, PERI, SPR, SRT, SYY are scheduled to release their quarterly results ahead of Monday's open.

Currencies

Dollar Looks to Break

Losing Streak: The

Dollar Index is on track for its first gain in six sessions as trade holds near 81.10. Light buying over the

course of the morning lifted the dollar back above the 81.00 level before

chopping around in a tight range between 81.10/81.15 all afternoon.

·

EURUSD is -35 pips at 1.3345 as trade pulls back from

yesterday's seven-week high. The single currency stalled at the June highs near

1.3400, and now looks to be slipping back towards minor support in the 1.3300

area.

·

GBPUSD is -25 pips at 1.5510 as sellers hold

strong in their defense of the 200-day moving average. Today's weakness comes

despite Britain's trade deficit narrowing to GBP8.1 bln

(GBP8.7 bln previous). Near-term support rests near 1.5400.

·

USDCHF is +25 pips at .9225 as trade has so far

been able to hold key support in in the .9200 area. Today's bid has the pair on

track to post its first gain in six days, but the bulls are not out of the

woods just yet. Minor resistance will pose some problems in the .9250 region

while the real victory for the bulls comes on a move through the 50- and

200-day moving averages (.9355). Swiss data is limited to retail sales.

·

USDJPY is -30 pips at 96.30 as trade checks up

after its recent slide. Data flow was absent in Japan, but one news story that

has made headlines is that Japanese debt climbed above the one

quadrillion yen mark for the first time ever. Japan's preliminary GDP

will cross the wires Sunday evening.

·

AUDUSD is +100 pips at .9200 as trade climbs for

a fifth session. The hard currency has rallied on the heels of mostly better

than expected Chinese data, and is nearing a test of the key .9300 level.

·

USDCAD is -45 pips at 1.0280 with action on track

to close near a two-week low. Today's selling has pushed action onto the

100-day moving average, and has come despite the disappointing Canadian

jobs report (-39.4K actual v +10.0K expected).

Weekly Analysis

Week 38

Technical Updates

Briefing's Commentaries

Week in Review: S&P

500 Finds Resistance

On Monday, the S&P

500 shed 0.2% as eight of ten sectors settled in the red. Stocks slipped out of

the gate after better-than-expected economic data from China and Great Britain

was unable to spark an early bid. Equities climbed off their early lows before

receiving an additional push following the release of the ISM Non-Manufacturing

Index, which posted its best reading since February 2011. Although the data

provided stocks with a boost, the S&P never made it into the green as

comments from Dallas Fed President Richard Fisher knocked the key indices off

their highs. Mr. Fisher said the Fed's bond buying program may lay the

groundwork for misallocation of resources and fuel future inflation. In

addition, he said the market could expect a slowdown in asset purchases later in

the year if the economy continues to "improve along the lines envisioned

by the Committee."

Tuesday's session saw

the S&P settle lower by 0.6%. Stocks spent the first 90 minutes of the

session in a steady decline as cyclical sectors pressured the index below the

1,700 level with financials, materials, and industrials leading to the

downside. All top-weighted banks ended in the red with Citigroup (C

51.32 -0.46) posting the largest loss among the majors. Meanwhile, the broader

sector slid 0.9%.

On Wednesday, the

S&P shed 0.4% to register its third consecutive decline. The benchmark

index fell to its lows during the first hour of action before spending the

remainder of the session in a slow climb. Stocks sold off at the open after

Asian indices endured a downbeat session with Japan's Nikkei falling 4.0% as

dollar/yen continued its recent weakness. The pair fell below 97.00 into the

Asian close and additional selling during the U.S. session pressured it into

the 96.50 area. The relative strength of most countercyclical sectors helped

the benchmark index erase about half of its losses during the afternoon. Health

care and telecom services ended little changed while utilities registered a

modest gain of 0.5%. For its part, the consumer staples sector (-0.5%) lagged.

Thursday's session began

with modest gains after upbeat data from China helped ease some concerns

regarding the pace of global growth. The Middle Kingdom reported an increase in

exports (+5.1% actual, +3.0% expected) and imports (+10.9% actual, +2.1% forecast)

while its trade surplus narrowed to $17.82 billion from $27.10 billion. Shortly

after the start of the session, the S&P notched a high of 1,700.20 before

aggressive selling pressured the benchmark index back to its flat line. The

slide coincided with notable dollar/yen weakness that sent the pair below 96.00

for the first time since June 19. The slide in equities and dollar/yen was

halted shortly after the first hour of action. Stocks then returned to their

highs but the S&P was unable to reclaim the 1,700 level. The rebound took

place as most cyclical sectors outperformed with materials in the lead. The

sector advanced 1.5% as the Chinese data underpinned steelmakers and miners.

Next Week In View

Jason's Commentaries

Friday started with a bearish bias which sells off till 11am out of no reason and started reversing at 11am ET again.That reversal wiped off half of its losses and stayed sidelined for the rest of the day. On the Dow, almost every component was red and the biggest laggard being Disney which fell 1.55% followed by AT&T which fell 1.39%. Amongst the Tech, Apple was also another heavy laggard which dragged down the entire tech sector. With leaders like Exxon Mobil lagging the Energy sector, Apple and AT&T lagging the Tech sector, BfA and Citi lagging the Financial Sector, it's without a doubt that the market was down broadly. The materials sector was the only sector that was up, held by names like Dow Chemicals, Alcoa, and Catepillar. However, the volumes on the down days are approx 650m shares on the NYSE and it was 635m shares traded on the NYSE. With the rest of the internals pointing at a mixed day, we might be looking at a weak retracement.On the Technical side, we're looking at Dow holding up at 15,400 points again and with that shadow on the candlesticks that long, I reckon that the support level will take some serious news to break it.

On the weekly perspective, it's pretty apparent that at a 61.8% retracement and we're unlikely to go down any further. So we're likely to head up or consolidate for a while before breaking up higher assuming there's no other bearish news to gyrate the market. For the coming week, we do not have much heavy economic news coming out therefore we're likely to head up higher to test the previous high made.

Market Call: FLAT to upside

Date:12 Aug 2013

No comments:

Post a Comment