7 Aug 2013 AMC

Market Summary

Market Internals

Leaders and Laggards

Technical Updates

Briefing's Commentaries

Major Averages Register Modest

Losses

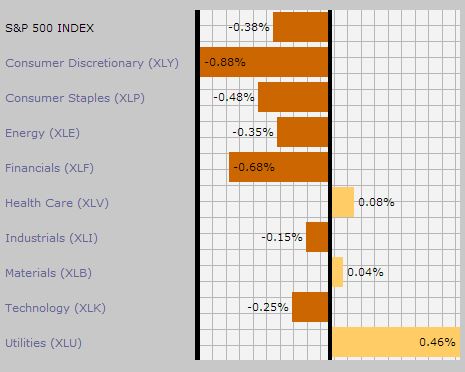

Sector Performance (%

change of the day): Utilities (+0.45%),

Health Care (+0.04%), Materials (+0.00%), Telecom

(-0.03%), Industrials (-0.21%), Tech (-0.28%), Energy

(-0.35%), Consumer Staples (-0.52%), Financials (-0.80%), Consumer

Discretionary (-0.83%).

Dow -0.3%, S&P 500

-0.4%, Nasdaq -0.3%, Nasdaq 100 -0.1%, S&P 400 -0.7%, Russell 2000 -0.7%

The S&P 500 settled

lower by 0.4% to register its third consecutive decline. The benchmark index

fell to its lows during the first hour of action before spending the remainder

of the session in a slow climb.

Stocks sold off at the

open after Asian indices endured a downbeat session with Japan's Nikkei falling

4.0% as dollar/yen continued its recent weakness. The pair fell below 97.00

into the Asian close and additional selling during the U.S. session pressured

it into the 96.50 area.

The relative strength of

most countercyclical sectors helped the benchmark index erase about half of its

losses during the afternoon. Health care and telecom services ended little

changed while utilities registered a modest gain of 0.5%. For its part, the

consumer staples sector (-0.5%) lagged.

Although the S&P was

able to trim its losses, the index could not regain its flat line as the

underperformance of influential cyclical sectors weighed. Financials and

discretionary shares both lost near 0.8%. In addition, the industrial sector

outperformed with a loss of 0.2%, but transportation companies lagged notably.

The Dow Jones

Transportation Average fell 0.7% as trucking companies led to the downside. CH

Robinson (CHRW 56.31, -3.27) tumbled 5.5% after missing on earnings

and revenue. Peer YRC Worldwide (YRCW 23.52, -5.06) also

endured a rough session after it too reported disappointing results.

Elsewhere, most major

bank shares registered losses and Bank of America (BAC 14.53,

-0.11) slid 0.8% after the Department of Justice filed a pair of lawsuits

alleging the bank has engaged in investor fraud when selling $850 million in

residential mortgage-backed securities.

Also of note, the

discretionary sector displayed broad weakness with notable losses among home

builders and retailers. The iShares Dow Jones US Home Construction ETF (ITB

21.41, -0.49) slumped 2.2% and the SPDR S&P Retail ETF (XRT

80.78, -1.19) lost 1.5%.

Treasuries registered

modest gains and the benchmark 10-yr yield fell five basis points to 2.60%.

So far, this week has

featured two light-volume sessions and today was not much different. With 629

million shares traded on the floor of the New York Stock Exchange, today's

final tally came up short of the 50-day average, which sits near 763 million.

Today's economic news

was limited to just two data points. The weekly MBA Mortgage Index ticked up

0.2% to follow seven consecutive contractionary readings, including last week's

decline of 3.7%.

Separately, June

consumer credit increased by $13.8 billion, which follows the prior month's

increase of $17.5 billion, and is higher than the $16.0 billion that had been

broadly expected among economists polled by Briefing.com.

Tomorrow, weekly initial

claims will be reported at 8:30 ET.

The U.S. Treasury will

auction $16 billion in 30-yr bonds.

|

After-Hours Report

|

|

|

|

|

|

A recap of the day’s

market activity in addition to an overview of key news stories released

after the close and key events that are scheduled for the next trading day. |

|

|

Updated: 07-Aug-13

17:38 ET

|

|

GRPN +16.6%, TSLA

+13.7%, TUMI -18.6%, FIO -16.4% following earnings/guidance

The S&P 500

settled lower by 0.4% to register its third consecutive decline. The

benchmark index fell to its lows during the first hour of action before

spending the remainder of the session in a slow climb.

Today after the close the following companies were scheduled to reported earnings: MG, ARRS, FIO, SYMM, GCAP, ASIA, IO, MKL, PRXL, SGI, BKD, CXO, DVR, DXCM, EDMC, ENSG, PRU, STRI, TTEK, WGL, GTY, IMPV, NAVG, PKT, RWT, ARRY, CECO, FTR, IILG, NRP, PODD, TWTC, AWK, BIOL, BWC, CODI, DMD, FTEK, MDLZ, NVTL, RBCN, SN, WTI, ADES, BIOS, CENT, CLR, CTL, CXW, DEPO, DK, DTSI, ENS, ETE, ETP, FLTX, GMCR, GNMK, GRPN, HALO, HNSN, IPAR, JCOM, LHCG, MHLD, MNTX, MRIN, MWE, MYRG, OFIX, OILT, OSUR, POWR, PPO, PRSC, PVA, RGP, RIG, RST, SSTK, STEC, SXL, SZYM, TCAP, TSLA, TUMI, TWGP, WR, AGU, BPZ, DIOD, FTK, LLNW, MBI, NGVC, SSRI, TNGO, WAGE, SCTY, EXP, EGLE, JACK, DRYS, MEAS, UHAL, RLD, RENT, ECOM, TXTR Other notable movers on earnings/guidance: GRPN +16.6%, TSLA +13.7%, CECO +12.3%, DXCM +9.2%, FLTX +7.2%, FTEK +6.4%, OSUR +6.1%, PKT +5.8%, STEM +5.8%, DEPO +4.8%, ARRS +4.0%, IDSY +4.0%, IPAS +4.0%, TROX +3.2%, MRIN +3.1%, JCOM +3.1%, IMUC +2.7%, JOE +2.7%, MDLZ +2.7%, DRYS +2.0%, SBY +2.0%, DMD +1.9%, EIG +1.6%, PRU +1.4%, NVTL +1.4%, OILT +1.3%, HALO +1.3%, HNSN +1.2%, UHAL +1.1%, TCAP +1.1%, TUMI -18.6%, MELA -17.6%, FIO -16.4%, SGI -14.6%, SCTY -10.9%, RBCN -10.7%, ACFN -10.5%, LLNW -8.2%, IO -8.0%, PPO -7.3%, ARRY -7.2%, GMCR -5.9%, IMPV -5.8%, VRNM -4.9%, PVA -4.0%, TTEK -3.4%, RLD -3.2%, SSTK -3.1%, CTL -3.1%, PCOM -2.7%, MBI -1.7%, JACK -1.7%, CVO -1.5%, CXW -1.3%, NGVC -1.3%, EGLE -1.2%, FTK -1.1%, CENT -0.5%, FSC -0.2%, NLY -0.2%

Futures are higher

after hours: S&P 500 futures are +1.93 from fair value of 1686.97 and

Nasdaq100 futures are +4.91 from fair value of 3113.59.

Tomorrow morning before the open two economic reports are scheduled to be released: 1) Initial Claims (Consensus 340k), and 2) Continuing Claims (Consensus 2975k) Tomorrow before the open the following companies are scheduled to report earnings: PMT, TMUS, LINE, MPW, SWC, NVO, IQNT, ACIW, BDC, BEAM, CNQ, FNP, FWLT, GTN, HSH, ICGE, MFC, OGE, RDEN, RGLD, SNI, GBDC, APO, SJI, BCRX, BR, CCOI, CQB, GLDD, NVAX, ONE, SGMS, FSYS, FUN, LAMR, THI, XTEX, AAON, AES, AMCX, AMRC, APEI, BCE, CBB, CDE, CNSL, CTB, DF, DNDN, FCN, GLP, HSC, IPCC, IRC, KIOR, MMS, OWW, SPH, SRPT, THS, TK, USPH, VC, WAC, WIN, AWR, HL, LMIA, SSYS, CAE, AAP, AINV, CSIQ, THR, FWM, NGPC, MZOR, WLH |

Commodities

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Treasuries

10-Yr:+12/32..2.602%.. USD/JPY:96.42.. EUR/USD:1.3339

{kind=link}

Treasuries Close Near Highs: Treasuries ended just off their best levels as buyers were in control over the course of the session. The complex saw an overnight bid as Asian equity markets dropped on Fed tapering concerns, and held their early gains throughout the European session. Maturities held in a tight range ahead of this afternoon's $24 bln 10-yr note auction before climbing to new highs as the results were digested. The auction drew 2.620% and a light 2.45x bid/cover. A slow week of data continues on Thursday with initial and continuing claims (8:30). Treasury will auction $16 bln 30-yr bonds. A solid 46.3% takedown by indirect bidders helped offset the slightly less than average direct bid (15.2%). Primary dealers were left with just 38.5% of the supply. The afternoon bid briefly pressured the 10-yr yield below 2.590%, but some light selling into the close made for a settlement of 2.600%. The 12 bp drop over the past couple of sessions has put minor support in the 2.550% region back in the spotlight, while the more important level remains 2.450%. Elsewhere, a gain of 26/32 for the long bond pushed its yield down more than 4.5 bps as it ended at 3.686%. Flattening continued along the knob of the curve as the 10-30-yr spread tightened to 108.5 bps. Meanwhile, precious metals climbed to their best levels into the close with gold adding $4 to $1286 and silver climbing $0.05 to near $19.60. A slow week of data continues on Thursday with initial and continuing claims (8:30). Treasury will auction $16 bln 30-yr bonds.

Next Day In View

On other news....

BoJ releases statement; reaffirms it will conduct money market operations so that the monetary base will increase at an annual pace of about 60-70 trillion yen.

Read more: http://www.briefing.com/Platinum/InDepth/InPlayFull.htm#ixzz2bMyEwBrW

Under Creative Commons License: Attribution

Currencies

Dollar Breaks Below 200-Day Moving

Average: The Dollar Index has been

offered throughout U.S. trade, and has pushed below key support in the 81.60

area aided by the 200-day moving average. Today's weakness has the

greenback on track to close at its lowest level in seven weeks.

·

EURUSD is +30 pips at 1.3335 as trade has finally

broken through 1.300 resistance. The bid has the single currency higher for the

third time in four sessions as action now looks to test the June highs near

1.3400. The ECB Monthly Bulletin and German trade balance will cross the wires

tomorrow.

·

GBPUSD is +140 pips at 1.5490 following today's

Bank of England Inflation Letter which indicated the central bank would keep

rates at current record lows so long as the unemployment rate holds above 7%. Sterling

plunged to 1.5200 in an initial response to the announcement, but saw a sharp

reversal as too many were caught leaning on the short side. The pair rallied to

test the 200-day moving average neat 1.5540 before sellers stepped in. Look for

prior resistance at the 1.5400 level to serve as near-term support.

·

USDCHF is -45 pips at .9210 as trade breaks

down to a seven-week low. Bears are looking to break .9200 support,

which dates back to February.

·

USDJPY is -125 pips at 96.50 as action flushes to

its lowest levels since the middle of June. Today's selling has the pair under

pressure for a fourth consecutive session ahead of tonight's Bank of

Japan rate decision. Japanese data out this evening is limited to the

current account balance.

·

AUDUSD is +20 pips at .9000 as trade ticks higher for a

third straight session. Hard currency bulls are hoping for a squeeze in

response to tonight's employment data. China's trade balance will be released

this evening.

·

USDCAD is +45 pips at 1.0420 as trade looks to close at

its best level in more than three weeks following the disappointing

Canadian building permits (-10.3% MoM actual v. -2.5% MoM expected) and Ivey

PMI (48.4 actual v. 56.3 expected) data. A move through the 1.0430

level likely sets up a test of the July highs near 1.0575. Canada's New Home

Price Index is due out tomorrow morning.

Jason's Commentaries

Was right that market started to retrace a little. Market was being dragged down by poor Asia performance yesterday which caused the day to start with a bearish bias. However, that bearish bias did not last long and started reversing at 12pm ET which subsequently regained half of it's initial losses. Consumer discretionary was the biggest laggard followed by Financials. Discretionary were being dragged down by Disney, Amazon, Home Depot which went down 1.7%, 1.28% and 1.52% respectively. Financials were being dragged down by companies like WFC and GS which lost 1.73% and 0.81% respectively. The only leader last night was Utilities. It seems that market might be turning its gearing into defensive stock which we will know in a few more days to come. Volumes is still weak at 628.8m shares traded on the NYSE. It was a moderate bearish day, which is not really support by the volume. As we're approaching the support level on the major indices, I reckon that the support will be held, especially Dow holding up above 15,400. Since we do not have much news coming out, I believe that the technicals should be able to do its magic.

Happy Hari Raya my Muslim friends!

Market Call:FLAT to upside

Date: 8 Aug 2013

No comments:

Post a Comment