15 August 2012

Market Summary

CPI came in under expectation... a sign of lower inflation... that probably held the market up... the market is still not convinced of the economic direction... Firstly, on lower volume, secondly having mixed results. Everything was flat yesterday.. I think today will be an important day as a number of data is coming out... but if... a report comes out red(likely the philly fed)... that's it...

Market Internals

Lower volumes, crazy intraday gyration, UVOL outpaced DVOL slightly, ADVN outpaced DECN slightly... New highs outpaced New lows significantly, TRIN at neutral, TICK was mostly positive through the day...

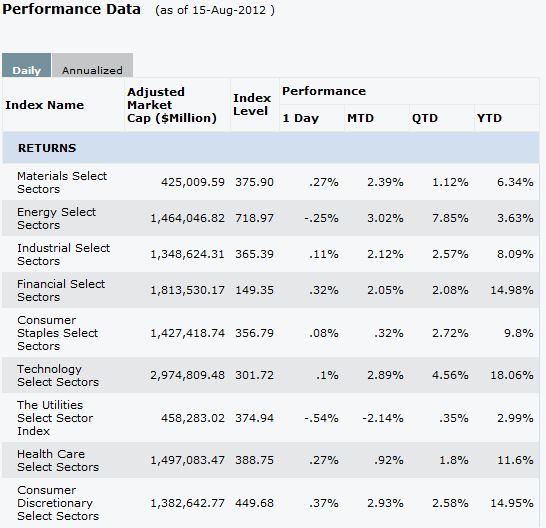

What a flat day.......

Leaders and laggards

what else to say... it's flat...

Technical Updates

Another small candle on the main indices... Noted that the DOW was the only component closes in the red.

Commentaries

| Stock Market Update |

| 16:20 ET Dow -7.36 at 13169.89, Nasdaq +13.95 at 3030.93, S&P +1.60 at 1405.53 :[BRIEFING.COM] Equities started the day on a down note before staging a slow climb towards session highs. With thin volume and economic data largely in-line, today's action occurred mostly around the unchanged line. An afternoon push attempted to lift stocks to a higher close but the move lacked conviction. As a result, the Nasdaq ended higher by 0.5% while the S&P 500 and Dow finished flat. Shares on the Nasdaq outperformed the broader market. Within the group, Akamai Tech(AKAM 36.80, +1.36) and Limelight (LLNW 2.60, +0.09) were up 3.8% and 3.6%, respectively. Both network companies rose on rumors which suggested AT&T (T 37.10, -0.15) will re-sell CDN services provided by either of the two companies. Both vendors are negotiating, with Akamai viewed as the favorite to win the contract. Abercrombie & Fitch (ANF 35.23, +2.90) was a session leader after beating on earnings and revenues. Shares of the apparel producer jumped 9.0% in reaction to the results. Competitors Aeropostale (ARO 13.63, +0.40) and American Eagle (AEO 21.13, +0.29) got a lift from the positive Abercrombie & Fitch results. The two stocks gained 3.0% and 1.4%, respectively. Two popular retailers saw contrasting performance following their earnings releases.Staples (SPLS 11.49, -1.96) plunged 14.6% after missing on earnings and revenues. Today's selling dropped the shares to levels not seen since October 2002. Meanwhile,Target (TGT 64.50, +1.12) advanced 1.8% after exceeding earnings estimates and reporting in-line revenues. Energy was one of today's main laggards despite crude oil climbing 1.2% to $94.50 and testing levels last seen in mid-May. The spike in crude comes on renewed tensions between Israel and Iran. Looking closer at the sector, Contango Oil & Gas (MCF 55.12, -4.76) slid 8.0% after announcing its Chairman and CEO, Kenneth Peak will be taking a medical leave of absence. Other energy names also showed significant losses despite the lack of news driving their declines. Alpha Natural Resources (ANR 6.61, -0.23) was down 3.4% whileWPX Energy (WPX 14.58, -0.37) slipped 2.5%. Gun makers Smith & Wesson (SWHC 8.60, -1.16) and Sturm Ruger (RGR 45.39, -2.69) were under pressure after receiving downgrades from KeyBanc Capital Markets. Smith & Wesson fell 11.9% after being downgraded from ‘buy' to ‘hold' while Sturm Ruger slumped 5.6% after being lowered from ‘hold' to ‘underweight.' The downgrades were handed down as analysts believe the industry is near its peak profitability. With the majority of second quarter results already delivered, a handful of names remain on the earnings calendar. Cisco Systems (CSCO 17.35, +0.18) and Applied Materials(AMAT 11.80, +0.09) will report after today's close. Cisco is expected to earn $0.45 on $11.61 billion revenues while the consensus calls for Applied Materials to deliver earnings of $0.22 on revenues of $2.32 billion. Retail names will headline tomorrow's reports before the bell. Analysts are expectingDollar Tree (DLTR 50.00, -0.62) to earn $0.47 on revenues of $1.71 billion while retail giant Wal-Mart (WMT 74.45, +0.44) is expected to report earnings of $1.17 on $114.80 billion revenues. The Housing Market Index for August registered a reading of 37. That was up from the prior month, and better than the reading of 35 that had been expected, on average, among economists polled by Briefing.com. Separately, industrial production increased during July by 0.6%, which was in-line with expectations. The reading follows the revised 0.1% increase experienced in the prior month. Capacity utilization hit 79.3%, which was also in-line with expectations, and up from the prior month reading of 78.9%. Consumer prices were unchanged during July, which was slightly cooler than the 0.2% increase that had been generally expected. Core prices increased by 0.1%, which fell short of the 0.2% increase expected by economists polled by Briefing.com. Tomorrow's economic data will be focused on jobs data and housing. Housing starts, building permits, and initial and continuing claims will be reported at 8:30 AM ET. The monthly Philadelphia Fed survey will be released at 10 AM ET. ..NYSE Adv/Dec 1899/1113. ..NASDAQ Adv/Dec 1719/768. |

After Hours

16:58 ET PETM +6.0%, NTAP +5.2%, CSCO +4.7%, A -8.5% following earnings/guidance :

Equities started the day on a down note before staging a slow climb towards session highs. With thin volume and economic data largely in-line, today's action occurred mostly around the unchanged line. An afternoon push attempted to lift stocks to a higher close but the move lacked conviction. As a result, the Nasdaq ended higher by 0.5% while the S&P 500 and Dow finished flat.

Today after the close the following companies reported earnings: A, MIPS, AVNW, CACI, CSCO, SINA, HOTT, LTD, NTES, AMAT, PETM, AFCE, NTAP, TAOM

Futures are higher after hours: S&P 500 futures are +1.48 from fair value of 1403.12 and Nasdaq100 futures are +6.43 from fair value of 2734.57.

Tomorrow morning before the open, three economic reports are scheduled to be released: 1) Initial Claims (Consensus 368k) and Continuing Claims (Consensus 3332k), 2) Housing Starts (760k), and 3) Building Permits (Consensus 755k).

Tomorrow before the open look for the following companies to report: LYTS, GKSR, PRGO, ARX, BKE, BONT, CATO, DANG, DLTR, GME, PERY, PLCE, ROST, SHLD, SMRT, SSI, WMT, EJ

Credits: Briefing.com

Commodities

Credits: http://www.cnbc.com/id/15839171/site/14081545/

Oil Spiked like crazy yesterday due to a lower in oil production. However, at 1.35AM ET, it closes in the red... Lean hogs dropped another 2%.. that looks bad...

Treasuries

Credits: http://www.forexfactory.com/calendar.php

The 10yr and 30 yr declined further... that doesn't look good.... DEJA VU!!!!

Yesterday i got the wrong call... however, it was a flat day nonethless.. Since the PMI has been dropping, i doubt the philly fed will be dovish anyway... the market is still looking for something to push it further...

https://www.facebook.com/photo.php?fbid=10151180102113665&set=a.10150362713198665.391889.144280373664&type=1&relevant_count=1

Another interesting data from my mentor's facebook...

Notice the relationship between the production numbers and the state of economy... what happened in 2001 and 2008???? correlate to the PMI numbers and you'll find we're not in a very good shape...

the rest of the world is already in recession... What makes you think that the US will be spared?

I'M STILL BEAR!!!

Market Call: 16 Aug

Date: DOWN

Accuracy: 7/12

No comments:

Post a Comment