7 August 2012

Market Summary

Damn.... Totally wrong... was expecting the market to pull back yesterday after such a massive run...

But no doubt.... after the spike at the early part of the session, profit taking started after lunch... you can expect quite a bit of weakness for these few days...

Market Internals

A bull day??? I think bulls are flat on the ground right now... looking at sudden spike in volume after lunch.... massive profit taking... on top of that...

Advance/Decn issues are flat as wel... just that the new Highs outpaced the new Lows...

TRIN remains pretty weak as well...

Advance/Decn issues are flat as wel... just that the new Highs outpaced the new Lows...

TRIN remains pretty weak as well...

Leaders and laggards

Technical Updates

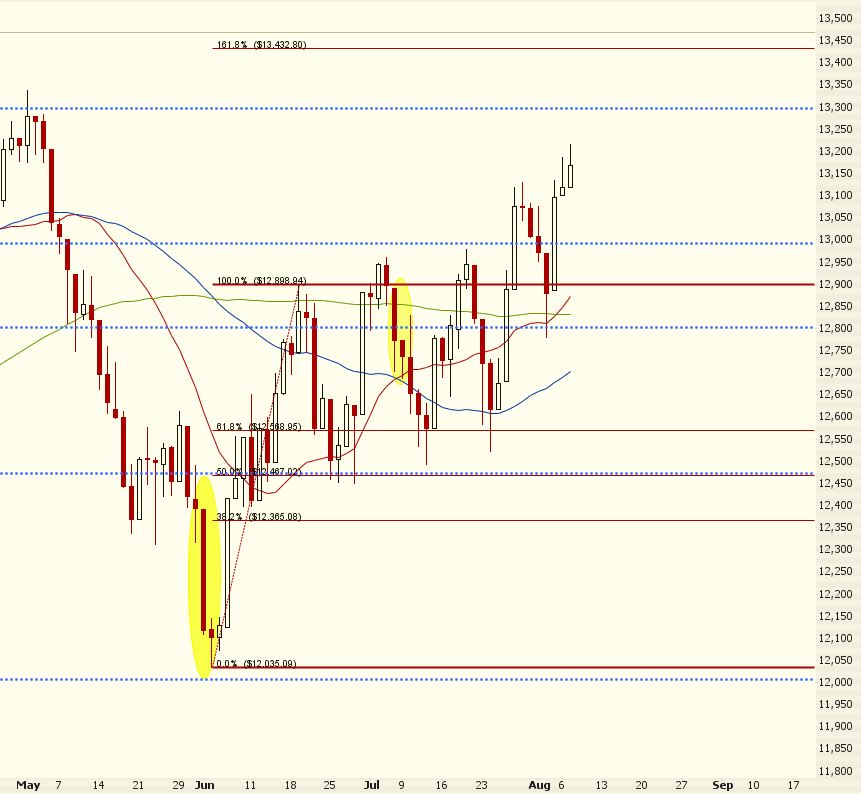

Now the major indices all faces their major resistance! time for PULLBACK!

Commentaries

| Stock Market Update |

| 16:20 ET Dow +51.09 at 13173.71, Nasdaq +25.95 at 3015.86, S&P +7.12 at 1401.35 :[BRIEFING.COM] After opening higher by 0.5%, stocks maintained their gains throughout the session. Similar to yesterday, low volume kept the markets relatively flat following the opening thrust higher. With no economic data of note being released, stocks maintained their gains and came off their highs towards the end of the session. As the day ended, the S&P 500 faded towards its opening level and the index ended up 0.5%. Fossil (FOSL 91.77, +21.98) surged by 31.5% after the company increased full-year guidance following an earnings and revenue beat. Today's buying lifted the stock out of a range which has held for three months. Competitor Movado (MOV 25.78, +3.06) benefited from Fossil's strength as investors expect Movado to also surprise to the upside. Shares of the luxury goods producer ended higher by 13.5%. US Home Systems (USHS 12.53, +3.47) gained 38.3% after Home Depot (HD 52.40, +0.40) agreed to buy the company for $12.50 per share. Energy was today's strongest performer. Within the group, Overseas Shipholding Group (OSG 6.66, +0.62) leaped 10.3% after a company director purchased 100,000 shares at $5.82. Chesapeake (CHK 19.37, +1.67) jumped 9.4% following a positive earnings report. Financials showed considerable strength. The SPDR Financial Select Sector ETF (XLF 14.94, +0.06) advanced 0.4%. Within the sector, JPMorgan Chase (JPM 37.01, +0.71) and Citigroup (C 28.89, +0.33) rose by 2.0% and 1.2% respectively. In addition, Morgan Stanley (MS 14.50, +0.36) gained 2.6%. Telecommunications was one of the weakest sectors. Inteliquent (IQNT 12.14, -1.78) weighed down the group after posting earnings and revenues below-expectations. The company also lowered their full-year forecast. Today's 12.8% decline puts the stock back at its mid-May levels. Shares of major pharmaceutical producers did not participate in today's advance. Elan(ELN 11.15, -0.10), Pfizer (PFE 23.74, -0.52), and Johnson & Johnson (JNJ 68.29, -0.55) announced that they will stop developing a treatment for Alzheimer's disease because of disappointing clinical results. All three stocks posted losses with Elan and Pfizer losing 0.9% and 2.1% respectively while Johnson & Johnson was off by 0.8%. The dollar index was virtually unchanged as the dollar's performance against the major currencies was mixed. The reserve currency gained 0.5% against the Japanese yen, and currently trades near 78.60. The British pound advanced 0.2% against the greenback to near 1.5630. The euro came off session highs and ended unchanged versus the dollar. The single currency trades around 1.2400. Also of note, the Australian dollar crossed 1.0600 which was a level not seen in five months. The Aussie has pulled back slightly since, to 1.0555. As earnings season winds down, a few notable companies have yet to report their quarterly results. Express Scripts (ESRX 56.02, +0.04), Priceline.com (PCLN 679.80, +14.68), and Walt Disney (DIS 49.81, +0.16) will release their earnings following today's close. In addition, Dean Foods (DF 12.42, +0.20), Dish Network (DISH 30.67, +0.16), andPolo Ralph Lauren (RL 153.03, +2.97) will report tomorrow morning. Tomorrow's economic data includes the MBA Mortgage Index due out at 7 AM ET. In addition, preliminary nonfarm productivity and unit labor costs will be released at 8:30 AM ET. Treasury will auction off 10-yr notes. ..NYSE Adv/Dec 1949/1065. ..NASDAQ Adv/Dec 1599/880. |

After Hours

17:10 ET DF +20.4%, RAX +8.5%, PCLN -16.3%, Z -9.0% following earnings/guidance:

After opening higher by 0.5%, stocks maintained their gains throughout the session. Similar to yesterday, low volume kept the markets relatively flat following the opening thrust higher. With no economic data of note being released, stocks maintained their gains and came off their highs towards the end of the session. As the day ended, the S&P 500 faded towards its opening level and the index ended up 0.5%.

Today after the close the following companies reported earnings: CREE, BKI, SMCI, SONS, ARRY, ENPH, ATLS, BIO, CSGS, GEVO, HUSA, KNXA, ONE, PHH, PRI, PSEM, CRL, DK, IO, NVTL, OSUR, XNPT, Z, BLKB, ENOC, SAPE, SEM, TRGT, ANV, DPM, GEO, RAX, VVUS, ARC, CQB, DIS, DMD, EGY, ETE, ETP, GCA, GIVN, GPOR, JAZZ, JIVE, KERX, LTRE, MODL, PL, POWL, PRMW, PRTS, PULS, BWC, CODI, DF, ELON, LYV, MALL, MYRG, PCLN, QUAD, SNTS, STEC, TRAK, TTGT, URS, WFR, WR, WRI, XL, BID, ESRX, RLJ, OPNT, PLAB, HRZN, MRC, MCEP, SZYM, REXX

Futures are lower after hours: S&P 500 futures are -0.31 from fair value of 1397.21 and Nasdaq100 futures are -2.35 from fair value of 2712.35.

Tomorrow morning before the open three economic reports are scheduled to be released: 1) MBA Mortgage Index, 2) Productivity-Prel (Consensus 1.5%), and 3) Unit Labor Costs-Prel (Consensus 0.4%).

Tomorrow before the open look for the following companies to report: MOLX, AVT, SWC, ALR, CCC, FSTR, VQ, AFAM, CLH, SKYW, ANR, BCE, CBB, CWH, FSYS, LAMR, NRG, OWW, PPL, DISH, HFC, LMIA, SATS, AAON, CORE, GLP, GTXI, IFF, LIOX, NXTM, AH, CGX, ES, EZCH, HII, INXN, KELYA, LSE, M, MFB, PRIM, SODA, SUSS, SVNT, THS, TTI, VPG, APEI, AONE, CSC, TDW, RL, AINV, RAH, RRMS, CG, ATRS

Commodities

Another weak day for the commodities as well.......

Treasuries

Some movement in the 10yr and 30yr T-bond... Something fishy going on???

Not a very heavy data day... I suspect the today is likely to be the day for pullback! I'm still bear........

Market Call: 8 Aug

Date: DOWN

Accuracy: 4/6

No comments:

Post a Comment