21 August 2012

Market Summary

That comes at a surprise... the bulls are losing their steam faster than expected and taking their profits before the FOMC minutes come out... signs of weakness! I'm bear now!!!

Market Internals

Volume increased significantly from the recent days of stalled pattern. A noted divergence here is that New Highs outpaced New Lows, And TRIN appeared in the bullish region, while DECN outpaced ADVN marginally. I believe this is some signs of bulls showing weakness.

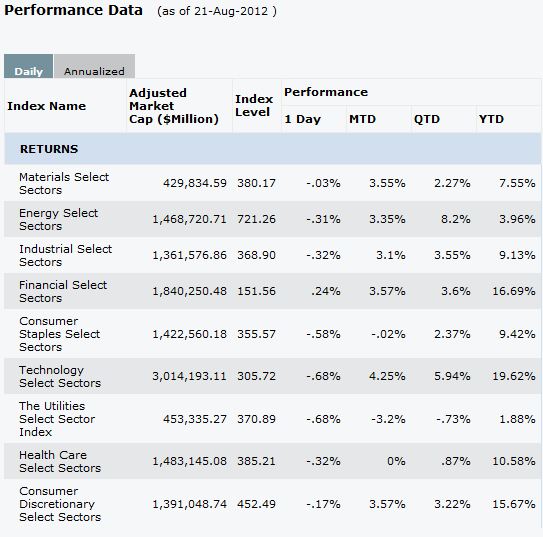

Leaders and laggards

Tech was the biggest loser yesterday as AAPL shredded some gains after becoming the biggest cap stock in the US.

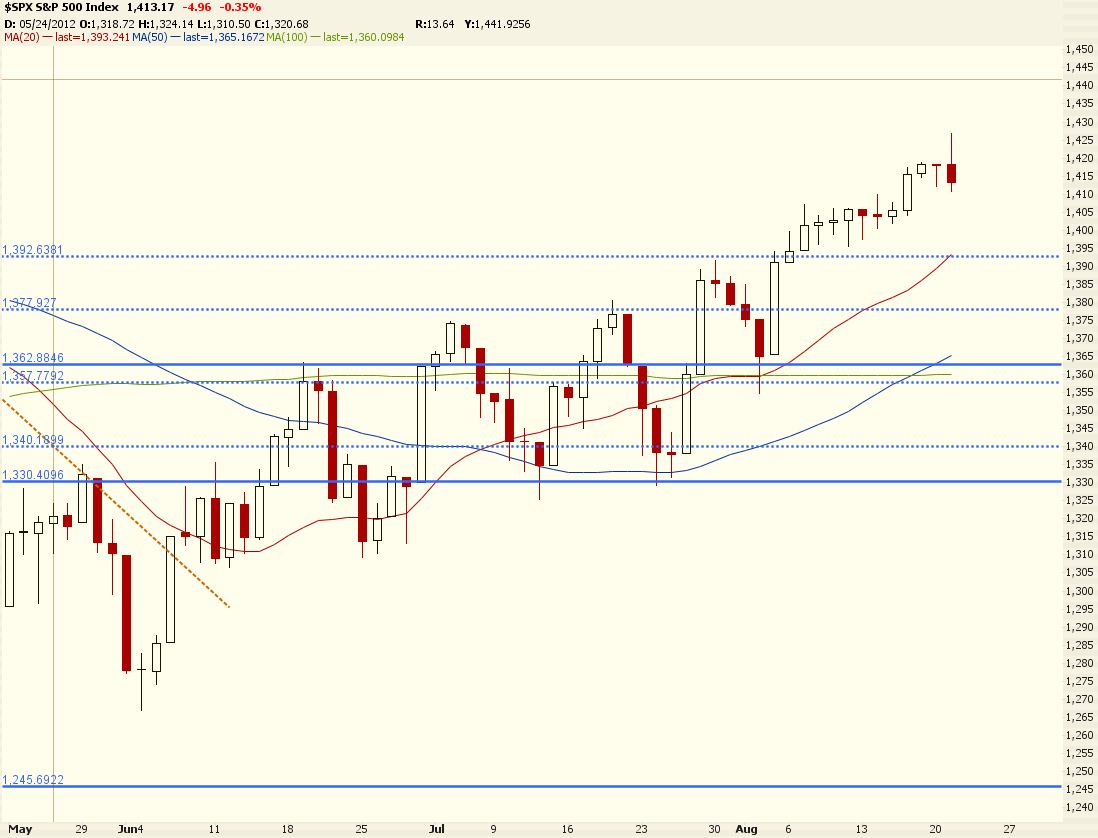

Technical Updates

Quite a bearish candle with long upper shadow... Bulls are unable to hold the highs and got trashed down across all 3 main indices. Let's see whether the minutes are able to crash it...

Commentaries

|

|

| Stock Market Update |

16:20 ET Dow -68.06 at 13208.69, Nasdaq -8.95 at 3067.26, S&P -4.96 at 1413.17 :[BRIEFING.COM] Equities got off to a strong start today but could not hold their gains into the afternoon. The S&P 500 briefly touched a 4-year high before retreating to session lows. Total volume was better than what has been seen in recent days, but remained well below average. The Dow underperformed and finished lower by 0.5% while the S&P 500 shed 0.4%.

Financial stocks outperformed the broader market as the components appeared to be benefit from the rotation out of traditionally safer stocks found in the utility and telecom sectors. Major names showed considerable intraday strength, but final gains were a bit slimmer due to the afternoon sell-off. JPMorgan Chase (JPM 38.04, +0.67) andCitigroup (C 30.73, +0.75) added 1.8% and 2.5%, respectively. Today's strength has Citigroup up nearly 16.0% since its earnings report in mid-July. European financials were even more exuberant as Deutsche Bank (DB 34.07, +1.38) and Credit Suisse (CS 18.68, +0.59) gained 4.2% and 3.3%, respectively.

The materials sector also showed strength. Within the group, A.M. Castle & Co (CAS 11.69, +2.47) surged 26.8% after Platinum Equity bought a 6.0% stake through metal processor Ryerson. The private equity firm also said it might try to buy the rest of the company. Meanwhile, Freeport-McMoRan (FCX 36.49, +1.13) advanced 3.2%.

The Dow Jones Transportation Average outperformed the market. After yesterday's rally in airline stocks was brought on by a fare hike, Delta Airlines (DAL 9.71, +0.25) enjoyed its second day of gains. Shares of the carrier ended higher by 2.6%. Trucking stocks were also stronger with Con-Way (CNW 31.24, +0.46) up 1.5%.

Coal stocks rallied after the U.S. Court of Appeals in Washington threw out an Environmental Protection Agency rule over limits on sulfur dioxide and nitrogen oxide emissions. Alpha Natural Resources (ANR 6.90, +0.40) jumped 6.2% on the news. Other coal names have faded some of the post-ruling gains, but they remained bid.Westmoreland Coal (WLB 7.94, +0.45) and Peabody Energy (BTU 23.79, +0.85) advanced by 6.0% and 3.7%, respectively.

Earlier today, tech giant Apple (AAPL 656.06, -9.08) marked an all-time high at $674.88, but some late morning selling dropped it into negative territory. The stock remained there for the remainder of the session and finished with a loss of 1.4%. Elsewhere, Daktronics(DAKT 9.43, +1.37) soared 17.0% after beating on earnings and revenues.

Shares within the telecommunications space weighed on the major averages. Neutral Tandem (IQNT 10.99, -0.56) slid 4.9% as selling pressure pushed the stock down to levels last seen in mid-March. Meanwhile, Verizon (VZ 42.89, -0.81) and AT&T (T 36.59, -0.30) ended lower by 1.9% and 0.8%, respectively.

There are a few names of interest remaining on the tail end of the earnings calendar. Dell(DELL 12.34, -0.22) will report earnings after today's close. The personal computer retailer is expected to earn $0.45 on $14.66 billion revenues. Meanwhile, Williams-Sonoma (WSM 38.23, +0.90) will also report after the bell. The culinary retailer is expected to report earnings of $0.41 on $863.84 million revenues.

Tomorrow morning, two apparel companies will report their quarterly results. Analysts expect American Eagle Outfitters (AEO 20.83, +0.38) to earn $0.21 on revenues of $738.72 million. Elsewhere, expectations call for Express (EXPR 16.90, -0.03) to earn $0.17 on $467.42 million revenues.

Tomorrow's economic calendar includes three releases. The MBA Mortgage Index will be announced at 7 AM ET, and existing home sales will be reported at 10 AM ET. Finally, the FOMC minutes will be released at 2 PM ET. ..NYSE Adv/Dec 1309/1648. ..NASDAQ Adv/Dec 1065/1385. |

|

After Hours

16:44 ET KTCC +15.1%, WSM +9.4%, UCTT -7.5%, DELL -3.6% following earnings/guidance :

Equities got off to a strong start today but could not hold their gains into the afternoon. The S&P 500 briefly touched a 4-year high before retreating to session lows. Total volume was better than what has been seen in recent days, but remained well below average. The Dow under-performed and finished lower by 0.5% while the S&P 500 shed 0.4%.

Today after the close the following companies reported earnings: ADI, AZPN, DELL, INTU, LZB, QIHU, WTSLA, WSM

Futures are higher after hours: S&P 500 futures are +1.31 from fair value of 1410.89 and Nasdaq100 futures are +2.32 from fair value of 2771.43.

Tomorrow morning before the open one economic reports is scheduled to be released: 1) MBA Mortgage Index.

Tomorrow before the open look for the following companies to report: AEO, CHS, EV, EXPR, TOL

Commodities

Sugar is dropping again........ Time to look at the SGG!

Treasuries

Not much changes to the T bonds as well.. I usually don't make market calls when big data comes out...but for the heck of it...

Date: DOWN

Accuracy: 8/16

No comments:

Post a Comment